1

Origins of the Crisis

Overview

The U.S. financial crisis of 2008 followed a boom and bust cycle in the housing market

that originated several years earlier and exposed vulnerabilities in the financial system. As

is typical of boom and bust cycles, this boom was characterized by loose credit, rampant

speculation, and general exuberance in the outlook for the market—in this instance, the

housing market. The subsequent downturn began as a housing crisis that initially seemed

to be concentrated in certain states and in the subprime mortgage market. Eventually,

however, the seemingly circumscribed housing collapse spread to the entire U.S. housing

market, as house prices declined nationwide. And because the financial system had

been integral to the housing boom, it was highly exposed to the housing market, whose

downturn would prove to be so severe that it threatened to drag down the financial

system with it in the absence of significant government intervention. Inexorably, the

collapse of the U.S. housing market in 2007 became the most severe financial crisis since

the Great Depression, and the financial crisis, in turn, resulted in a protracted economic

contraction—the Great Recession—whose effects spread throughout the global economy.

The nationwide housing expansion of the early 2000s was rooted in a combination

of factors, including a prolonged period of low interest rates. By mid-2003, both long-

term mortgage rates and the federal funds rate had declined to levels not seen in at least

a generation. One response to low interest rates was an acceleration in U.S. home price

appreciation to double-digit rates for the first time since 1980. Another response was a

series of mortgage market developments that dramatically weakened credit standards

in mortgage lending. These market developments were associated with a glut of savings

held by global institutional investors seeking high-quality and high-yield assets; loose

underwriting standards; a complex and opaque securitization process; the use of poorly

understood derivative products; and speculation based on the presumption that housing

prices would continue to increase.

Other factors were in play as well in the years leading up to and during the housing

market expansion. Financial innovation and deregulation contributed to an environment

in which the U.S. and global financial systems became far more concentrated, more

interconnected, and, in retrospect, far less stable than in previous decades. These factors

4 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

and the ones mentioned in the preceding paragraph helped fuel a housing boom while also

making the U.S. financial system more vulnerable to collapse in times of stress.

One set of key players in fueling the boom was real estate investors. Attracted by the

expectation of future house price appreciation and the availability of cheap credit, many real

estate investors entered the housing market,

1

motivated to buy and re-sell homes to make

short-term gains. Investors’ speculative behavior contributed to the striking house price

appreciation, which in turn spurred potential homebuyers to act before prices increased

further. In the end, when house prices collapsed, many of these real estate investors realized

losses and many homeowners lost their homes.

Also fueling the boom was the role mortgage companies played in the steady rise of house

prices. Mortgage credit was cheap, so when high house prices limited the pool of low-risk

borrowers who could qualify for conventional mortgages, mortgage lenders expanded the

group of potential borrowers by offering new and innovative mortgage products designed

to reach less-creditworthy borrowers. However, many of these borrowers became the

targets of predatory lending practices that placed borrowers into mortgage products that

would eventually create financial hardship for them, as they ended up building debt rather

than wealth, either through repeat refinancings that took equity from homes or through

adjustable rate features that challenged their repayment abilities.

The housing boom was fueled, as well, by the financialization of housing assets: illiquid

real estate (housing) was turned into a financial asset that could be traded more easily and

therefore made it possible for investors to participate in new and innovative ways. One form

of financialization was securitization, or packaging of securities backed by mortgages

2

—a

process that allowed investors to invest in the U.S. housing market and that therefore

linked individual homeowners to the global financial system of large banks, shadow

banks (explained below in the section “Financial Market Disruptions”), and institutional

investors. Participants in the securitization process had short-term incentives to profit

without accounting for the risk; they largely passed the inherent risk of the underlying

mortgage to the next participant in the securitization chain. While the securitization

process had been around for decades before the housing boom, its scope expanded as new

types of securities were generated.

A number of the new types of securities were liquid and were assigned a high credit

rating, despite being backed by pools of risky mortgages. As the housing boom progressed,

the financial system continued creating various mortgage securities that were aimed at

transforming the risk and meeting investor demand. For example, financial institutions

transformed lower-rated tranches of mortgage-backed securities (explained below in

the section “Mortgage Securitization”) into collateralized debt obligations that were

1

Karl E. Case and Robert J. Shiller, “Is There a Bubble in the Housing Market?,” Brookings Papers on

Economic Activity 2 (2003): 321, https://www.brookings.edu/wp-content/uploads/2003/06/2003b_bpea_

caseshiller.pdf.

2

A detailed explanation of securitization is given in footnote 8.

5 CHAPTER 1: Origins of the Crisis

often AAA-rated. It was thought that by generating securities with different risk profiles,

financial engineering of this kind could diversify and transform the risk associated with

the underlying mortgages. Furthermore, derivatives that referenced these mortgage

securities were created, spreading and amplifying the risk further into the system. These

derivatives did not have cash flows based on actual mortgages but tracked the performance

of mortgage securities, enabling investors to speculate on mortgage security performance.

Financial institutions also began to issue credit default swaps to insure investors against

losses on these securities. The risk of these securities, however, was not well understood.

Nevertheless, the securities were held throughout the financial system, and because

the financial system was highly interconnected, even institutions that were not directly

involved with mortgage securitizations had some exposure to the mortgage market. As

risk spread throughout the financial system, therefore, the entire system ultimately became

exposed to the housing market.

Another source of risk, besides exposure to risky mortgages, was high leverage.

Financial institutions increased leverage by relying more on debt to finance their balance

sheets. Although higher leverage enabled institutions to earn a higher return on equity, it

also made them more vulnerable to greater losses if mortgage defaults should increase—

as they ultimately did.

Initial signs of the housing collapse to come emerged in 2006, as the housing market

expansion slowed. In the middle of 2005, mortgage rates began to rise and, by the middle

of 2006, had increased more than 100 basis points. Higher mortgage rates reduced housing

market activity, causing home price growth to slow. After rising at double-digit annual

rates for 27 consecutive months through early 2006, home prices peaked in mid-2006. The

housing market slowdown eliminated the expectation of future investment gains and,

along with it, the ability of borrowers to refinance (for without the expectation of rising

prices, lenders would be unwilling to provide new funds); housing activity slowed even

further. As interest rates rose and house prices began to fall, many homeowners became

unable to meet mortgage payments on their existing loans or refinance into a new loan,

and mortgage defaults rose rapidly.

Yet, through the end of 2006, most macroeconomic indicators continued to suggest that

the U.S. economy would proceed uninterrupted on its path of moderate growth. Indeed,

aside from some concerns about an overheated housing market,

3

there was little in the

way of financial data to suggest that the U.S. and global economies were on the verge of

a financial system meltdown. In hindsight, however, we know that by the mid-2000s the

United States was experiencing a housing price bubble of historic proportions and that

already in 2006 the first signs of trouble were apparent. In 2007, when the bubble burst, the

financial systems of the world’s most advanced economies were brought relatively quickly

to the brink of collapse.

Throughout 2006 and even into 2007, there was considerable and ongoing debate as to whether a housing

price bubble actually existed. A consensus would not be reached until the collapse was well underway.

3

6 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

How did this happen? Ultimately, as house prices declined nationwide and

mortgage defaults began rising, the value of all the mortgage-backed securities

deteriorated. The rise in defaults, by undermining the value of trillions of dollars of

mortgage-backed securities, severely disrupted the securitization funding mechanism

itself. That mechanism—the securitization system that generated mortgage-backed

securities (MBS) from mortgages—had become opaque and very complex, and the

financial institutions involved were highly leveraged. The lack of transparency and the

complexity of the securities masked the risk, and the high leverage left investors with

little capital to cushion loss. Moreover, the financial institutions had underpriced risk,

having been lulled into complacency by the prolonged period of economic stability that

preceded the onset of problems. When mortgage defaults began to rise, the system’s

interconnectedness, complexity, lack of transparency, and leverage exacerbated the

effects of the crisis. Eventually, many of the largest financial institutions suffered

catastrophic losses on their portfolios of mortgage-related assets, resulting in severe

liquidity shortages. As noted above, even financial institutions without large MBS

holdings were affected because they were deeply interconnected with the financial

system in which MBS played so significant a role.

Observing the devastating cascade of falling house prices, subprime mortgage

defaults, bankruptcies, and write-downs (or reductions in the value of mortgage

assets), investors and creditors lost confidence in the financial markets. The credit

markets froze, and at the same time many overleveraged financial institutions were

forced to sell assets at fire-sale prices, further reducing liquidity. Under mark-to-

market accounting rules,

4

these asset sales only precipitated further rounds of asset

write-downs. The mounting losses strained financial institutions, causing many of

them to fail. Eventually the situation became so dire that government interventions on

an unprecedented scale were undertaken to break the downward spiral of defaults and

to restore confidence in, and functionality to, the financial marketplace.

As noted in Financial Crisis Inquiry Commission (FCIC), The Financial Crisis Inquiry Report: Final Report of

the National Commission on the Causes of the Financial and Economic Crisis in the United States (2011), 226–

27, http://fcic-static.law.stanford.edu/cdn_media/fcic-reports/fcic_final_report_full.pdf, mark-to-market is

the process by which the reported value of an asset is adjusted to reflect the market value. The process had a

detrimental effect during the crisis, as mark-to-market accounting rules required firms to write down their

holdings to reflect the lower market prices. Firms claimed that the lower market prices did not reflect market

values but, rather, reflected fire-sale prices driven by forced sales.

4

7 CHAPTER 1: Origins of the Crisis

Housing Market Bubble and Mortgage Crisis (2006–2007)

By the end of the 2000–2006 period, the rapid rise in U.S. house prices had transformed

from a boom to a nationwide housing market bubble. Like all bubbles, this one could

not be sustained forever, and the bursting of the bubble was devastating to many recent

homebuyers, who (like many other people) had expected home prices to continue rising.

In that expectation, many borrowers had taken out mortgages on which they were

unable to continue making payments when the terms of their mortgages changed and

housing prices fell (as noted above, falling prices meant lenders would not refinance).

The bubble was fed not only by people taking out mortgages for homes, however.

Also feeding the bubble was a system, created by financial institutions, that linked

homebuyers’ demand for housing with investors’ demand for highly rated assets with

high yields. Financial institutions purchased mortgages from mortgage originators,

packaged the mortgages into securities, and sold the securities—whose credit quality,

in retrospect, was inaccurately assessed by the rating agencies—to investors needing a

safe place for their funds. These transactions, in turn, then provided the liquidity and

short-term funding from the capital markets that mortgage lenders depended on to

continue to originate loans.

The chain linking homebuyers who were taking out mortgages with investors who

were buying securities that were backed by pools of such mortgages was only as strong

as its weakest link. When mortgage defaults rose, all the other links in the chain were

irreparably weakened.

e Rapid Rise in House Prices

Coming out of the bank and thrift crisis of the late 1980s and early 1990s, the United

States experienced an expansion of housing construction, a rise in home prices, and

an increase in housing credit, all of which persisted through the 2001 recession and

accelerated in the early 2000s. By the time national house prices peaked (in the middle

of 2006), they had increased at double-digit annual rates for 27 consecutive months—

from early 2004 through the first three months of 2006—culminating in a 14.2 percent

annual gain in 2005 (see Figure 1.1). Reinhart and Rogoff observe that “between 1996

and 2006, the cumulative real price increase was about 92 percent—more than three

times the 27 percent cumulative increase from 1890 to 1996.”

5

Their research found no

housing price boom during that 106-year period comparable in sheer magnitude and

duration to the one that ended in the subprime mortgage crash that began in 2007.

Indeed, the extremes of housing value during the housing boom and bust of the mid-

2000s stand out starkly, as Figure 1.2 illustrates.

Carmen Reinhart and Kenneth Rogoff, This Time Is Different: Eight Centuries of Financial Folly (2009), 207.

5

8 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

Figure 1.1. S&P/Case-Shiller Home Price Index, 1987–2013

Year-Over-Year Percent Change National Index Value 2000 = 100, NSA

20

15

10

5

0

-5

-10

-15

Change in Home Price, Year-Over-Year (L)

Home Price Index (R)

Peak: July 2006

200

175

150

125

100

75

50

25

0

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Source:

S&P/Case-Shiller (Haver Analytics).

Figure 1.2. Real Home Price Index, 1890–2013

Index (1890 = 100)

200

180

160

140

120

100

80

60

Great Depression 2000s

and World War II

Boom

1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Source:

Robert J. Shiller, http://robertshiller.com.

Note:

Index is based on ination-adjusted sale prices of standard existing homes, not new construction, to track the

v

alue of housing as an investment over time.

9 CHAPTER 1: Origins of the Crisis

Several factors contributed to the run-up in housing prices. One was low interest rates: in

July 2003, the federal funds rate declined to 1.01 percent, its lowest level in 45 years, while

in June 2003, the Freddie Mac 30-year conventional mortgage rate fell to 5.21 percent, the

lowest level in the 32-year history of the Primary Mortgage Market Survey. This prolonged

period of low rates after the 1991–1992 recession made mortgages less expensive, thus

increasing demand, and, with increased demand, house prices began rising. Another factor

in the price run-up was the origination of mortgage products that increased demand by

enabling less-creditworthy borrowers to qualify for mortgages (see the box titled “Types of

Mortgage Products”). Financial institutions, including a number of large thrifts, investment

banks, and commercial banking organizations, acted as originators of subprime and Alt-A

mortgages and also as underwriters and issuers of securitizations backed by these loans.

6

A third factor in driving up prices was the influx of investors into the housing market:

drawn by the expectation of future house price appreciation, investors bought homes for

investment gain, not residence. All of this was consistent with Case and Shiller’s description

of a housing bubble. “The notion of a bubble,” they write, “is really defined in terms of

people’s thinking: their expectations about future price increases, their theories about the

risk of falling prices, and their worries about being priced out of the housing market in the

future if they do not buy.”

7

As interest costs fell and, in response, the demand for mortgages increased, the funding

for mortgages increased significantly, allowing lenders to offer credit to more borrowers.

Behind this increase in funding were (1) a heavy demand of investors worldwide for highly

rated assets with high yields, and (2) the satisfaction of that demand through the mortgage

securitization process, which allowed the financialization of mortgage assets.

8

The heavy worldwide demand for safe assets was brought about by an increase in global

savings. This glut of global savings reflected many factors, including the buildup of foreign

exchange reserves in emerging market economies and the aging populations in industrial

economies (retirees have higher savings).

9

The securitization process that served to satisfy

the worldwide demand involved the packaging of pools of mortgages into securities that

6

Inside Mortgage Finance Publications, The 2010 Mortgage Market Statistical Annual, vol. 2, 2010.

7

Case and Shiller, “Bubble in the Housing Market?,” 301.

8

As explained in the overview section, financialization of housing assets means that “illiquid real estate was

turned into a financial asset that could be traded more easily and therefore made it possible for investors

to participate in new and innovative ways.” Securitization is the process by which assets with generally

predictable cash flows and similar features are packaged into interest-bearing securities with marketable

investment characteristics. Investors buy the right to future cash flow, thus providing increased liquidity back

to the seller, who then has additional monies to lend. Over time, securitized assets have been created using

diverse types of collateral, including home mortgages, commercial mortgages, mobile home loans, leases,

and installment contracts on personal property. The most common securitized product is the mortgage-

backed security (MBS).

9

Ben Bernanke, “The Global Saving Glut and the U.S. Current Account Deficit,” remarks at the Sandridge

Lecture, Virginia Association of Economists, Richmond, VA, March 10, 2005, https://www.federalreserve.

gov/boarddocs/speeches/2005/200503102/.

10

CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

could be sold to institutional and individual investors as a way to transfer risk among

investors; the investors received rights to cash flows of the underlying mortgage pools.

The relatively illiquid mortgage asset could be quickly bought or sold in the market

without the asset’s price being affected, and innovations in finance supplied different types

of assets with different risk profiles to suit different investor requirements, not only the

need for safety. Securitization, which came to dominate mortgage funding, was the vehicle

by which global savings contributed to the decline in longer-term interest rates and, in

addition, helped finance the U.S. residential market (investment in MBS increased the

liquidity available for financing additional mortgages, as explained in the next section).

e Foundations of the Mortgage Crisis

Just when the increased liquidity provided by securitization allowed lenders to offer credit

to more borrowers, the rapid increase in home prices reduced affordability—but also

fed buyer interest in purchasing a home (either to own or to turn a profit) before prices

rose further. Lenders, competing to attract customers and to meet the financing needs of

prospective homebuyers, diversified their mortgage offerings and eased lending standards.

Both of these practices—offering nontraditional mortgages and the relaxation of lending

standards (see the box titled “Types of Mortgage Products”)—helped homebuyers bridge

the affordability gap and facilitated lending to less-creditworthy borrowers.

Accommodating borrowers was made easier by the mortgage securitization system.

Banks and other mortgage originators originated loans, then distributed them by

selling them in the secondary loan market; the purchasers of the loans were mortgage

securitizers, who paid the originators, or lenders, high fees for mortgages; and the high

fees created incentives for lenders to fill the securitization pipeline by relaxing lending

standards and in some cases by aggressively marketing mortgages. The securitization

process is described in more detail below, in the section “Mortgage Securitization.” This

“originate to distribute” model led to a rise in predatory lending that targeted a wide

spectrum of consumers who might not have understood the embedded risks but used

the loans to close the affordability gap. In the end (see the next section, “The Housing

Market Collapse”), the originate-to-distribute model, with the misaligned interests of

all parties, undermined responsibility and accountability for the long-term viability

of mortgages and mortgage-related securities and contributed to the poor quality of

mortgage loans and, ultimately, to the riskiness of the securities backed by the loans.

11 CHAPTER 1: Origins of the Crisis

Types of Mortgage Products

Mortgages fall into two broad categories: prime and nonprime. Prime loans are

issued to borrowers whose more pristine credit is considered most creditworthy.

Such borrowers receive the best rate. Nonprime is the generic term for loans whose

mortgage interest rates are substantially higher than the prevailing prime rate. The

two types of nonprime loans are subprime and Alternative-A, or Alt-A.

Subprime loans are higher-interest loans that involve elevated credit risk and

are generally viewed as higher risk. Alt-A mortgages are made to borrowers with

credit ranging from very good to marginal, but they are made under expanded

underwriting guidelines that make these loans higher risk and also higher interest.

When strong home price appreciation and declining affordability helped drive up

the demand of borrowers for mortgage products that would allow them to stretch

their home-buying dollars, lenders—flush with mortgage credit—accommodated

by offering nontraditional (alternative) mortgage products. Nontraditional

mortgage loans have some features that differ from a plain-vanilla prime loan.

Among the nontraditional mortgages originated during the boom were interest-

only mortgages (IOs), adjustable rate mortgages (ARMs) with flexible payment

options (option ARMs, or payment-option mortgages), simultaneous second-

lien or piggyback mortgages, and no-documentation or low-documentation

loans. IO and payment-option loans were specifically designed to minimize

initial mortgage payments by eliminating or relaxing the requirement to repay

principal during the early years of the loan. Piggyback mortgages were a lending

arrangement in which either a closed-end second lien or a home equity line of

credit was originated at the same time as the first-lien mortgage loan to take the

place of a larger down payment. In no-documentation or low-documentation

loans, the documentation standards for verifying a borrower’s income sources or

financial assets were reduced or minimal.

Any of these loans—prime, subprime, nontraditional—could be structured as

an adjustable rate mortgage. ARMs have an interest rate and payment that change

periodically over the life of the loan, the changes being based on changes in a specific

index. In addition, there are hybrid ARMs and option ARMs. The former, also

known as short-term hybrids, have an initial fixed rate for two or three years and

then turn into an adjustable rate loan with an annual adjustment in rate or payment

or both. The option ARMs allow borrowers to set their own payment terms on a

monthly basis. The borrower could, for example, make a minimum payment lower

than the amount needed to cover interest; or pay only interest, deferring payment

of principal; or make payments calculated to have the loan amortize in 15 or 30

years. Interest typically was reset every month, and interest payments that were

deferred were added to principal through negative amortization.

continued

12 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

Problems escalated when risk layering occurred—that is, when a loan combined

several risky features. An example of such a loan was a subprime hybrid ARM:

a variable-rate loan offered to a subprime borrower, with an initial rate that was

probably quite low (to tease the borrower in) but that after a short period increased

to monthly payments that were often unaffordable. Another example was a non-

amortizing interest-only mortgage made to a borrower on the basis of little or no

documentation to validate the borrower’s income or assets. When risk layering

occurred, products grew in complexity, and the total risk was heightened.

Among the new, nontraditional mortgage offerings, many were structured as

adjustable rate loans, not fixed rate. More than three-fourths of the subprime mortgages

that were originated during the period 2003 through 2007 were short-term hybrids

(the interest rate is fixed for the first couple of years and then becomes adjustable and

benchmarked to short-term rates).

10

Most Alt-A loans were also adjustable rate loans, as

were most option adjustable rate mortgages. Option ARMs, as noted, offered borrowers

the choice of making full payments, interest-only payments, or minimum payments that

were less than the interest due. About 94 percent of option ARM borrowers made only

the minimum monthly payment, creating negative amortization.

11

Like the subprime

short-term hybrid mortgages, ARM loans had interest rates that were fixed for the

first couple of years but then were benchmarked to the LIBOR rate.

12

Under the more

relaxed underwriting standards at the time, many borrowers qualified for adjustable

rate mortgages based only on their ability to pay the low initial monthly payments as

determined under the introductory teaser rate. Hence, their ability to afford the mortgage

after the teaser rate expired was predicated on their ability to refinance the mortgage

before the higher payments became effective.

The ability to refinance—counted on by many investors, homebuyers, and originators—

depended critically on house prices. As long as house prices were rising, lenders were

generally willing to supply new funds with new terms. And even after house prices at the

national level peaked, in mid-2006, housing market participants generally did not expect

house prices to crash. After all, the United States had not experienced large nationwide

declines in house prices since the Great Depression. In mid-2006, some observers saw the

10

Christopher J. Mayer, Karen M. Pence, and Shane M. Sherlund, “The Rise in Mortgage Defaults,” Federal

Reserve Board Finance and Economics Discussion Series 59 (2008): 5, https://www.federalreserve.gov/pubs/

feds/2008/200859/200859pap.pdf.

11

Austin Kilgore, “Subprime Problems Persist, as Alt-A, Option ARM Crisis Brews,” HousingWire, January 11,

2010, https://www.housingwire.com/articles/6208-subprime-problems-persist-alt-option-arm-crisis-brews.

12

LIBOR stands for the London interbank offered rate; this rate is set daily and is the interest rate at which

banks offer to lend funds to one another in the international interbank market.

13 CHAPTER 1: Origins of the Crisis

turning point (identified as such only in retrospect) as nothing more than a correction,

not the presage of a precipitous decline:

With interest rates rising and speculative demand cooling,

the housing boom is coming under pressure … As long as the

economy continues to create jobs and builders trim production

to match slowing demand, house prices will keep climbing and

the housing sector will likely achieve a soft landing. Although

house price growth will likely moderate in many areas, sharp

drops in house prices are unlikely anytime soon. Major house

price declines seldom occur in the absence of severe overbuilding,

major job loss, or a combination of heavy overbuilding and

modest job loss. Fortunately, these preconditions are nowhere in

evidence across the nation’s metropolitan areas.

13

In hindsight, optimism in the housing market outlook in mid-2006 was based on a

major misreading of the market. Pressures had already been building against further

house price appreciation. In 2004, the Federal Reserve had started to tighten monetary

policy by raising the target federal funds rate in response to the increasing pace of

economic activity. Nevertheless, through 2005 and into 2006, despite the rise in interest

rates, a continuing flow of funds into the mortgage market maintained the easy credit

conditions and, even as the housing market expansion began to slow, homeowners

remained able to refinance. However, in 2006, with interest rates rising and (as shown in

Figure 1.3) house prices beginning to decline, homeowners whose mortgage payments

were indexed to interest rates were unable to refinance. Many homeowners and housing

investors were stuck with homes they could neither afford nor sell. Thus, the stage was

set for increasing numbers of delinquencies, defaults, and foreclosures.

e Housing Market Collapse

According to the Financial Crisis Inquiry Commission (FCIC), one of the first signs of the

impending collapse was an increase in the number of early payment defaults—defined as

occurring when a borrower becomes more than 60 days delinquent within the first year

of a mortgage. Defaults on subprime and Alt-A mortgages began to rise in late 2005. As

house prices declined further, default rates on higher-quality mortgages also rose, as shown

in Figure 1.4. By mid-2010, almost one out of every ten mortgage loans was past due, with

almost 30 percent of subprime ARM borrowers and almost 14 percent of prime ARM

borrowers in delinquency.

14

In addition, the decline in house prices resulted in negative

13

Joint Center for Housing Studies, “Affordability Problems Escalating Even as Housing Market Cools. 2006

State of the Nation’s Housing Report Is Released,” Press Release, Harvard University, John F. Kennedy School

of Government, June 13, 2006.

14

Mortgage Bankers Association, “Delinquencies and Foreclosure Starts Decrease in Latest MBA National

14 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

equity for many homeowners who had bought homes with little or no down payment.

These homeowners were underwater on their mortgages (i.e., the value of the outstanding

mortgage exceeded the value of the home). The share of underwater homeowners out of

all homeowners with a mortgage rose drastically as, eventually, house prices at the national

level declined more than 30 percent from their peak—and in some areas of the country,

they fell more than 50 percent. By 2010, more than 12 million homeowners—about 1 in 4

with a mortgage—owed more than their homes were worth.

15

Figure 1.3. Home Sales and Home Price Index, 2000–2013

Existing Home Sales S&P/Case-Shiller Home Price Index

Thousands of units National Index Value 2000 = 100, NSA

50

75

100

125

150

175

200

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Existing Home Sales (L)

Home Price Index (R)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Sources: S&P/Case-Shiller and National Association of Realtors (Haver Analytics).

Of the players linked in the securitization chain, one of the earliest to feel the effects

of the downturn in housing prices was mortgage originators, for which subprime loans

represented a significant portion of revenue and assets. As subprime loan originations

plummeted from 20 percent of total mortgage production in 2006 to 8 percent in 2007,

16

subprime originators faltered. By the spring of 2008, with the failure of many subprime

originators (including top lenders Countrywide Financial Corporation and Ameriquest

Mortgage Company), the U.S. subprime mortgage industry had essentially collapsed.

Delinquency Survey,” August 26, 2010, https://www.mba.org/x73818.

15

CoreLogic, CoreLogic® Equity Report, 4Q 2013 (2014), 8.

16

Inside Mortgage Finance Publications, The 2010 Mortgage Market Statistical Annual (2010), vol. 1, 2010.

15

35

CHAPTER 1: Origins of the Crisis

Figure 1.4. Mortgage Loans Past Due, by Type of Loan, 2000–2013

Percent

5

10

15

20

25

30

All Loans

Conventional Prime ARM

Conventional Subprime

Conventional Subprime ARM

0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Source:

Mortgage Bankers Association (Haver Analytics).

From the Mortgage Crisis to a Financial Crisis (2008)

The ramifications of the mortgage crisis went far beyond mortgage originators, as the

securitization chain also involved (among others) mortgage servicers, underwriters,

guarantors, and securitizers. The chain stretched across many players from depository

institutions to investment firms, with interconnections that were extensive and opaque,

and risks that were magnified by the increased use of financial leverage in a generally

deregulatory climate. Because of the high interconnectedness within the financial

system, the collapse of the subprime mortgage industry undermined the securitization

system itself and the financial markets.

The central element of the securitization chain, as has been noted, was pools of

mortgage-backed securities. But the pivotal role played by these securities depended on

the assurance investors received from rating agencies that these securities were priced

appropriately for the risk they contained—and as mortgages defaulted, the MBS and

securities derived from them had to be downgraded. Firms that were heavily invested in

such securities and at the same time highly leveraged were caught in a vise, and even the

reputations of the rating agencies themselves were tarnished.

16 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

Mortgage Securitization

The securitization process was a way to pool individual mortgages into a bond, that

is, a security, to be sold to investors. The resulting mortgage-backed security was often

carved into different pieces, or tranches, with a range of risk and return to appeal to

investors’ differing appetites. Investors bought the tranche(s) that served their needs.

The senior tranches were the highest rated and were considered to have the lowest risk

and the highest priority for payment. The equity tranches were the lowest tranches; they

had the highest return but also the highest risk because they would be the first to lose

money if mortgage loan borrowers defaulted.

Historically, securitization for the mortgage market was provided primarily by Fannie

Mae and Freddie Mac, which are Government-Sponsored Enterprises (GSEs) created by

Congress to provide the U.S. housing market with liquidity, stability, and affordability.

17

Fannie and Freddie, private companies at the time of the boom,

18

purchase and securitize

mortgages, selling the securitized mortgages to outside investors and holding some

mortgages and MBS as investments. With the housing market heating up, however, non-

agency (or private label) securitization activity—until then a relatively small share of

the market—ramped up to exceed the securitization activity of the GSEs. Figure 1.5,

showing MBS issuance from 1990 to 2013, displays the striking rise in the volume of

private label MBS issued beginning in 2002. Private label MBS doubled in dollar volume

from 2003 to 2005, increasing to over half of total MBS issuance in 2005 and 2006.

The increase in private label securitization activity, which involved many different types

of firms within the financial system, created tremendous capacity for new mortgages. To

fill the pipeline, as noted above, mortgage originators began to lower credit standards or

ease documentation requirements or both. One result was that mortgage pools became

more risky. In an attempt to generate securities that were low risk, financial institutions

turned to creative re-securitizations by securitizing the tranches of risky mortgage

securities into higher-rated securities. (The fundamental assumption was that although

all the tranches were backed by risky mortgages, some of the mortgages would pay out,

and as long as they did, they would satisfy the payments needed to pass through to the

newly securitized higher-rated security.) Ultimately, however, despite the higher ratings,

the securities proved very risky—and at the end, defaults were so large and so numerous

that the payment stream to these securities dried up.

The basic security—the mortgage-backed security—became the building block of

more-complex products, as MBS themselves were re-securitized into securities and sold

to investors as well as traded among the financial institutions that created them.

19

For

17

Fannie’s formal name is Federal National Mortgage Association (FNMA). Freddie’s is Federal Home Loan

Mortgage Corporation (FHLMC).

18

Fannie Mae and Freddie Mac were put into government conservatorship in September 2008. This is covered

in more detail below, in the section “Institutions in Crisis in 2008.”

19

A financial “product” is an instrument that involves moving money from one party to another. Thus, the

17 CHAPTER 1: Origins of the Crisis

example, lower-rated MBS were repackaged into collateralized debt obligations (CDOs).

Like MBS, CDOs were issued in tranches that varied in risk and had ratings that ranged

from high to low,

20

with investors in the lowest rated of these securities being exposed to

the highest risk. In this manner, mortgage risk appeared to be further diversified. Adding

to the perceived reduction of risk were credit default swaps (CDS), which provided

investors with insurance against losses on MBS, as explained in the next section.

Figure 1.5. Issuance of Mortgage-Backed Securities, 1990–2013

Billions of Dollars

3,000

2,500

2,000

1,500

1,000

500

0

Source:

Inside MBS & ABS, Inside Mortgage Finance.

Reprinted with permission. Inside Mortgage Finance Publications, Inc. www.insidemortgagefinance.com.

Private-Label

Fannie Mae

Freddie Mac

Ginnie Mae

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Another source of risk was a technique, also involving MBS, that banking companies

often used to increase their leverage without running afoul of regulatory requirements.

They would retain MBS in structured investment vehicles (SIVs), which were highly

leveraged entities held by banking companies but which, as separate legal entities,

were off the banks’ balance sheets and were therefore not subject to regulatory capital

requirements, even if a SIV’s parent holding company was under federal supervision.

SIVs were designed to generate cash flows by issuing short- to medium-term debt—

including asset-backed commercial paper

21

—at a low interest rate to raise funds that the

term can refer equally to a simple loan or a complex security. A home equity line of credit is a financial

product, and so are collateralized debt obligations, which are securities made up of repackaged MBS.

20

FCIC, Final Report, 127–29, http://fcic-static.law.stanford.edu/cdn_media/fcic-reports/fcic_final_report_full.

pdf.

21

Asset-backed commercial paper is a short-term promissory note whose repayment is backed by cash flows

18 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

institution could invest in longer-term assets, such as MBS. SIVs were first established in

1988 and remained relatively unscathed during pre-2007 periods of financial distress. By

2007, there were 36 SIVs and, between 2004 and 2007, the total assets held in SIVs had

tripled to $400 billion,

22

meaning that SIVs had come to have substantial exposure to the

mortgage market. The exposure would lead to their demise.

In sum, by generating a variety of complex financial products based on pools of

mortgages, private label securitizers created within the financial system an additional

level of complexity, opacity, and interconnectedness. Investment entities and financial

institutions were heavily involved in securitizing and underwriting MBS, investing in

derivatives, and generally creating and investing in new financial products.

23

But the

opacity of these instruments and activities masked the underlying systemic risk, which

derived both from the riskiness of the mortgages backing the securities and from the

highly leveraged nature of many of the institutions involved. Investment banks (part of the

shadow banking system) were not subject to the types of restrictions on the use of financial

leverage that banks were subject to, and were therefore able to expand their balance sheets

by increasing leverage to a greater extent than federally supervised banks were allowed

to.

24

Finally, although the deep interconnectedness among investment entities and financial

institutions spread risks across the securitization chain, it also created conflicts of interest

within the chain: originators and underwriters (at the front of the chain) were not acting in

the best interest of the investors and bondholders (at the end of the chain).

25

e Role of Rating Agencies and the Devastating Eect of Downgrades

During the years when subprime losses were materializing, one group critical to the entire

mortgage-based investment process was credit rating agencies. Credit rating agencies

assign credit ratings to a variety of financial institutions and financial assets, and during

the period in question, the agencies were rating MBS. The reason these ratings were critical

is that both investors and insurers of investment contracts relied on them. Investors relied

(and still rely) on credit ratings—particularly on those issued by one of the Nationally

from specific pools of assets such as trade receivables or mortgages. This commercial paper plays a prominent

role in the section below titled “Financial Market Disruptions.”

22

FCIC, Final Report, 252.

23

According to the FCIC, derivatives are financial contracts whose prices are derived from the performance

of an underlying asset, rate, index, or event. The use of derivatives grew significantly during the 2000s as a

way to ensure payment (losses due to price movement could be recouped through gains on the derivatives

contract). The resulting growth in leverage made financial institutions “vulnerable to financial distress or

ruin if the value of their investments declined even modestly” (ibid., xix, 45–51).

24

For a more detailed discussion of the shadow banking system and financial interconnections, see Zoltan

Pozsar et al., “Shadow Banking,” Federal Reserve Bank of New York Staff Report 458 (2010), https://www.

newyorkfed.org/medialibrary/media/research/staff_reports/sr458.pdf.

25

International Monetary Fund, “Navigating the Financial Challenges Ahead,” Global Financial Stability

Report (2009), 77–115.

19 CHAPTER 1: Origins of the Crisis

Recognized Statistical Rating Organizations (NRSROs)

26

—to assess the credit quality of

their investments. Many investors (for example, pension funds) are required to adhere

to mandates on the quality distribution of assets they hold, and the quality distribution

is typically determined by the credit ratings from an NRSRO. In addition, credit rating

agency ratings are often used in investment contracts to protect investors against a

possible credit downgrade. For example, if investors bought AAA-rated securities (such

as mortgage derivatives) because they believed—on the basis of the rating—that the

securities were risk free, but the securities were subsequently downgraded, the contract

might have entitled the creditor to demand collateral from the debtor. Insurers, too,

relied on credit ratings when they started guaranteeing the AAA ratings of MBS, putting

their own reputation and financial strength on the line because of confidence in the

credit ratings issued by the agencies.

In 2007, subprime defaults were increasing, and the performance of MBS and other

structured financial products started deteriorating. According to Benmelech and

Dlugosz, deterioration in the credit ratings of such products began likewise in 2007.

In

that year, there were more than 8,000 downgrades, eight times the number in 2006.

27

In the first three quarters of 2008, there were almost 40,000 downgrades, far exceeding

the cumulative number of downgrades for the period 2000 through 2007. Moreover,

the magnitude of the downgrades—the number of levels, or “notches,” by which

each rating was lowered—became much more severe in 2007. In 2005 and 2006, the

average downgrade each year was 2.5 notches, but in 2007 the average downgrade was

4.7 notches, and in 2008 it was 5.6 notches.

28

The sharp increase in the number and

severity of downgrades was devastating for the holders of the securities affected, for the

reputation of the rating agencies themselves, and for insurers.

The holders of the securities found that their previously AAA-rated investments—the

highest rated, considered the safest of investments—had become unmarketable.

29

Under

mark-to-market accounting rules, institutions that held these now-unmarketable mortgage-

backed bonds had to write them down.

30

Investor demand plummeted and securitization

activity dropped precipitously. Private label securitization—which, as noted, had provided

much of the funding for new mortgages—continued dropping until, in 2008, it virtually

disappeared. As a result, many underwriters were stuck holding large portfolios of mortgages

and MBS that could not be sold and were quickly losing value. This downturn would have

significant implications for the financial markets, as discussed in the next two sections.

26

NRSROs are credit rating agencies registered as such with the Securities and Exchange Commission.

27

Efraim Benmelech and Jennifer Dlugosz, “The Credit Rating Crisis,” NBER Macroeconomics Annual 2009 24

(2010): 172.

28

Ibid., 170.

29

Carl Levin, Hearing of the U.S. Senate Permanent Subcommittee on Investigations, “Wall Street and the

Financial Crisis: The Role of Credit Rating Agencies,” Opening Statement, April 23, 2010, 4.

30

FCIC, Final Report, 227–30.

20 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

Among the many reasons mentioned above for the puncturing of the housing

bubble was new pricing information that contributed to the decline in MBS values.

Gorton makes an important point about the role that information about the MBS

market played in puncturing the housing and mortgage-backed securities bubble. He

observes that information about the pricing of residential mortgage-backed securities

was not commonly available in real time until the ABX index was introduced, at the

start of 2006.

31

The ABX index measures the value of subprime mortgages. He states,

“The introduction of these indices is important for two reasons. First, they provided

a transparent price of subprime risk, albeit with liquidity problems. Second, [the

transparent price of subprime risk] allowed for [the efficient] shorting of the subprime

market,”

32

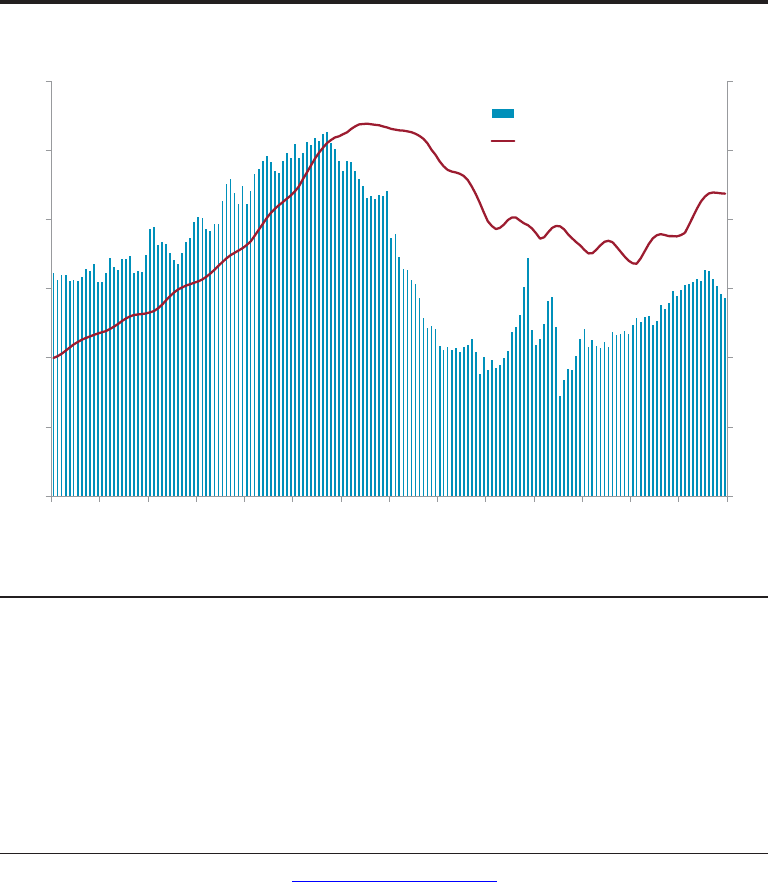

enabling investors to hedge their positions.As seen in Figure 1.6, new vintages

in 2007 declined sharply upon issuance. Gorton states that “it is not clear whether the

housing price bubble was burst by the ability to short the subprime housing market or

whether house prices were going down and the implications of this were aggregated

and revealed by the ABX indices.”

33

Regardless, he makes a compelling case that the

ABX index provided transparency for the pricing information on subprime MBS,

revealing deterioration and playing an important role in the decline of house prices, as

investors pulled out of the housing market.

As financial stress continued and investors increasingly questioned the credibility of

the credit ratings, the reputation of rating agencies declined. As they kept downgrading

MBS and CDOs, it became apparent that the high ratings previously assigned to these

securities had been overstated and were overly optimistic. Part of the problem was that

the models used by credit rating agencies were based on more traditional mortgage

products than the ones in the market at the time and on historic data that did not cover

an episode of a nationwide downturn. The data covered the recent period characterized

by low delinquency and default rates, and housing downturns that were concentrated

in just some states. The models did not account for the risk scenario of a massive,

nationwide decline in home prices.

34

Another part of the problem was that financial

institutions that issue securities paid rating agencies to rate their products, and the

institutions typically shopped around for favorable ratings. Many observers have noted

that the desire to retain business encouraged credit rating agencies to provide securities

ratings that were agreeable to the issuing institutions.

35

31

The ABX index is a financial benchmark that references 20 equally weighted residential mortgage-backed

security tranches. There are also sub-indexes for bonds based on their rating level: AAA, AA, A, BBB, and

BBB–. The “vintage” of an ABX index refers to the date it was introduced.

32

Gary Gorton, “The Subprime Panic,” European Financial Management 15, no. 1 (January 2009): 32.

33

Ibid., 34.

34

Markus K. Brunnermeier, “Deciphering the Liquidity and Credit Crunch 2007–2008,” Journal of Economic

Perspectives 23, no. 1 (Winter 2009): 81, http://pubs.aeaweb.org/doi/pdfplus/10.1257/jep.23.1.77.

35

See, for example, Simon Johnson and James Kwak, Thirteen Bankers (2010), 139.

21 CHAPTER 1: Origins of the Crisis

The rating downgrades also affected monoline insurers, companies whose single line

of business was to guarantee financial products and whose role in the mortgage market

had increased during the years leading up to the financial crisis. Monoline insurers

traditionally insured municipal bonds against default, but during the years preceding

the financial crisis, they started to insure mortgage securities, issuing CDS that insured

against declines in the price of CDOs and MBS. As noted above, this insurance

guaranteed the AAA ratings on these securities. The value of the guarantee was based

on the AAA status of the insurer.

Figure 1.6. Mortgage Credit Default Swap ABX Indexes

ABX Index 7-1 Series Price

100

80

60

40

20

0

1/19/2007

5/19/2007 9/19/2007 1/19/2008 5/19/2008 9/19/2008

AAA

AA

A

BBB

BBB-

Source:

Bloomberg.

Note: The 7-1 series started January 1, 2007.

As mortgage CDO and CDS issuances grew, investment banks created synthetic

CDOs. These synthetic CDOs referenced mortgage securities but were not actually

backed by them or by mortgage assets. Instead, they were backed by credit default swaps.

In essence they reflected bets on the mortgage market—bets that increased leverage in

the system without actually financing mortgages (see the box titled “CDOs and CDS”).

Weakness in the mortgage markets challenged the profitability of monoline insurers,

and the challenge to the insurers’ profitability worried holders of CDS guarantees.

Because many insurers did not expect to incur losses, they were thinly capitalized. In

late 2007, one of the smaller insurers, ACA, reported a net loss of $1.7 billion due to

22 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

losses on CDS contracts.

36

In January 2008, Fitch Ratings downgraded monoline insurer

Ambac, and rating agencies then began downgrading other monoline insurers; the

downgrades continued through the end of the summer. In June of that year, Standard

and Poor’s downgraded monoline bond insurer MBIA, which at that time was liable for

$2.9 billion to satisfy potential termination payments and for approximately $4.5 billion

in underlying collateral.

37

Markets reacted by selling MBS, CDOs, and related securities,

and the stock prices of monoline insurers (as well as of other financial institutions that

were exposed to mortgage securities) continued to decline.

CDOs and CDS

Collateralized Debt Obligations (CDOs) and Credit Default Swaps (CDS) played

integral roles in spreading and amplifying the risk of the mortgage market

throughout the financial system.

CDOs were a type of mortgage asset structured from lower-rated tranches of

MBS tranches that were individually difficult to sell to investors, who demanded

highly rated securities. CDOs were structured to further diversify the risk of a given

pool of lower-rated tranches of MBS, on the assumption that payments would flow

from some of the MBS tranches, even if other tranches were to bear losses. CDOs

were structured like MBS, with a waterfall of payments going first to the AAA-

rated tranche. About 80 percent of the tranches of these CDOs were highly rated,

despite the fact that their value was based on lower-rated tranches of MBS. Lower-

rated tranches of CDOs were further bundled and packaged into new CDOs, called

CDO squared. The CDO process exposed risk not only to CDO investors but to the

securities firms that issued CDOs, as they held the lower-rated MBS tranches until

the CDO was issued. The risk was further spread throughout the financial system

as these securities were used as collateral in short-term funding markets.

In addition, key financial institutions issued CDS to insure against losses on

MBS, CDOs, and other mortgage securities. CDS were a type of financial contract

in which the issuer retained the risk of default and paid the CDS purchaser in the

event of default. The CDS served as insurance to the purchaser, who did not need

to own the security. CDS issuance ramped up along with the rise of CDOs and

other mortgage securities. CDS issuance was profitable as long as the mortgage

market remained strong and the insured mortgage securities were considered low

risk. By providing insurance against losses on mortgage securities, CDS furthered

continued

36

FCIC, Final Report, 276.

37

FCIC, “Credit Ratings and the Financial Crisis,” Preliminary Staff Report, (2010) 8, http://fcic-static.law.

stanford.edu/cdn_media/fcic-reports/2010-0602-Credit-Ratings.pdf.

23 CHAPTER 1: Origins of the Crisis

the perception of the safety of the system and perpetuated investor demand for

what were, in fact, precarious mortgage securities.

Synthetic CDOs consisted of CDS that referenced MBS and CDOs without

containing cash flows from these mortgage securities. Since they only referenced

mortgage securities, synthetic CDOs did not directly finance mortgage issuance,

but enabled investors to speculate on the mortgage market. For example, "short"

synthetic CDO investors who bought a CDS agreement on a referenced CDO paid

premiums to the CDO and received payment from the CDO if the referenced

CDO did not perform. "Unfunded long" synthetic CDO investors who bought a

CDS agreement on a referenced CDO received premiums if the referenced CDO

performed, but had to pay out if it did not perform.

The financial system aimed to diversify mortgage risk by creating new highly

rated mortgage securities to meet investor demand. The demand for highly

rated mortgage securities further supported mortgage issuance. Ultimately, the

performance of the different tranches of the MBS securities upon which CDOs and

CDS were based, were highly correlated. When MBS losses mounted, the losses

were amplified throughout the financial system.

Source: FCIC, Final Report, Chapter 8.

Financial Market Disruptions: Illiquidity and Fire Sales

As financial distress spread across the securitization chain, the ripple effects from the

troubles in the housing market began to reach deeper into the financial system. Uncertainty

over collateral value, asset quality and asset liquidity, and counterparty creditworthiness

caused a rapid withdrawal of short-term liquidity, especially in the shadow banking

system (see second paragraph below). Illiquidity, on top of high leverage, forced firms to

engage in asset fire sales, which depressed asset prices even further.

38

With so much of short-term lending based on collateral composed of now-discredited

structured products, the market completely shut down. Some nonbank entities were able

to obtain liquidity support for their mortgage-related assets from their banking affiliates,

which had access to Federal Reserve liquidity facilities.

39

For financial institutions with

38

Brunnermeier, “Deciphering Liquidity,” 77–100.

39

When market liquidity dried up during the crisis, concerns about financial stability prompted the Federal

Reserve to grant exemptions to Sections 23A and 23B of the Federal Reserve Act, which limit transactions

between banks and their nonbank affiliates such as broker-dealers and insurance companies. The 23A

and 23B restrictions are intended to limit the exposure of a bank to its nonbank affiliates (a bank is

regulated, protected by FDIC deposit insurance, and allowed access to Federal Reserve liquidity facilities;

a nonbank affiliate is not). The exemptions allowed bank holding companies to obtain liquidity for their

nonbank subsidiaries from bank subsidiaries that could access the Federal Reserve’s liquidity facilities. See

24 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

limited access to funding markets, the only way to raise collateral was by selling assets

at steep discounts, but these fire-sale prices were then used to mark-to-market similar

assets, beginning another round of fire sales. These market disruptions caused distress in

the financial system, particularly in the shadow banking system.

The shadow banking system consists of broker-dealers, money market mutual funds

(MMFs), hedge funds, insurance companies, and other nondepository financial institutions

(including investment banks) that match short-term investor cash with longer-term assets.

The complex web of financial linkages among these entities was an important channel

for propagating the mortgage crisis. These entities, as well as banks, relied heavily on

short-term funding, which they accessed through a variety of instruments that were based

in some way on MBS or the underlying mortgages.

40

Two examples of such short-term

funding vehicles are repurchase agreements (repos) and commercial paper.

Repos are contracts under which the repo holder (a hedge fund, for example) sells

securities to another financial firm (an MMF, for example) with the agreement to buy

back the securities at a later date (usually overnight), typically at a higher price. In effect,

repos are short-term, collateralized loans. Commercial paper is a short-term, unsecured

promissory note. Asset-backed commercial paper (ABCP) is a short-term promissory

note for which payment is based on cash flows from securitizations or the underlying

assets. Institutions that rely on repos and commercial paper can continue to roll over

both of these short-term instruments as long as the demand for them is strong, but cash

providers can withdraw funding very quickly by refusing to roll over the agreements.

41

In the period leading up to the financial crisis, broker-dealers and hedge funds relied

heavily on repos for funding, and many more financial institutions relied on the issuance

of commercial paper.

42

On the demand side were MMFs, which invest in short-term debt

securities with funding from investors seeking a safe, deposit-like asset. MMFs were a

large and, before the crisis, steady source of demand for the repos and commercial paper

that other types of financial firms were issuing in their need for short-term funding.

Since MMFs offer their investors a stable net asset value of one dollar per share regardless

of the value of the underlying assets, they seek to invest in safe assets. Short-term debt

securities issued by investment banks were considered safe, and MMFs held them.

In the summer of 2007, as mortgage defaults rose and the value of MBS fell, demand

for the short-term instruments rapidly declined. Cash providers no longer wanted to

U.S. Government Accountability Office, Government Support for Bank Holding Companies, GAO-14-18,

November 2013, https://www.gao.gov/assets/660/659004.pdf.

40

Martin Baily, Robert Litan, and Matthew Johnson, “The Origins of the Financial Crisis,” Initiative on Business

and Public Policy at Brookings (2008), 27–31, https://www.brookings.edu/wp-content/uploads/2016/06/11_

origins_crisis_baily_litan.pdf.

41

Gary Gorton, “Slapped in the Face by the Invisible Hand: Banking and the Panic of 2007,” Federal Reserve

Bank of Atlanta 2009 Financial Markets Conference: Financial Innovation and Crisis, 30, http://citeseerx.ist.

psu.edu/viewdoc/download?doi=10.1.1.189.1320&rep=rep1&type=pdf.

42

Pozsar et al., “Shadow Banking,” 35.

25 CHAPTER 1: Origins of the Crisis

enter into repos collateralized by MBS, fearing that if the other party to the contract (the

counterparty) defaulted, they would be left holding an asset with a declining value. As for

ABCP, since it was based on the cash flow from underlying mortgages and MBS, it was

suddenly seen as more risky than before. Eventually, many banking companies with off-

balance-sheet SIVs—which financed MBS and mortgage purchases by issuing ABCP—

were forced to bring these entities onto their own balance sheets to prevent the entities’

insolvency and the legal and reputational damage that could result from default.

43

In late 2007 the ABCP market collapsed, and in 2008 a number of hedge funds and SIVs

were forced to liquidate their portfolios, having become unable to roll over short-term

debt. In the course of 2007 and into 2008, SIV balance sheets had continued to weaken,

and liquidity had become a major issue. For highly leveraged institutions like SIVs and

hedge funds, steep markdowns of assets under mark-to-market rules initiated increased

margin and collateral calls. Because of the general opacity of SIVs, the increased calls on

some SIVs prompted investor withdrawal from other, potentially safer SIVs.

During the crisis, with illiquidity crippling the financial system, distress was

exacerbated by the high level of leverage present in many financial institutions. Higher

leverage amplifies gains when the assets bought with the borrowed money increase in

value, but it also magnifies losses when the value of the assets declines.

44

Leveraged investors are required to hold some minimum level of cash or collateral

with a broker institution to guard against losses. Financial institutions purchased assets

on margin, holding the minimum level of cash or collateral that was required and

borrowing most of the funds needed to purchase assets. As noted, the higher the margin,

the higher the profits from a rise in the asset price—but the larger the losses from a price

decline. For example, a financial institution that purchases $100 in assets with $10 of its

own capital and $90 of borrowed funds has a leverage ratio of 10 and has purchased the

asset at a 10 percent margin. If the value of the asset falls to $90, the firm realizes a $10

loss and has no capital remaining. If the price falls below $90, the firm needs to sell assets

to meet its margin requirement of 10 percent.

As securities fall in value and losses mount, the leveraged investor is required to

provide more cash or sell a portion of the securities. Highly leveraged firms may have

less access to cash and be more likely to experience collateral calls or funding outflows.

If many leveraged firms must meet these calls all at the same time and are forced to

raise capital by selling assets whose prices are declining, the supply of assets for sale may

increase enough to drive the price down even further. This additional drop may trigger

additional margin and collateral calls.

In 2007, the markdowns of assets by highly leveraged institutions caused increased

43

Baily, Litan, and Johnson, “Origins,” 29. For a table describing the outcomes for the major structured

investment vehicles, see Gary Gorton, “The Panic of 2007,” NBER Working Paper 14358 (2008), appendix B,

http://www.nber.org/papers/w14358.pdf

.

44

FCIC, Final Report, xix.

26 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

margin and collateral calls, which started a vicious cycle of falling prices and fire sales.

According to the FCIC, in that year the major investment banks—Bear Stearns, Goldman

Sachs, Lehman Brothers, Merrill Lynch, and Morgan Stanley—were operating with a

leverage ratio as high as 40.

45

This ratio indicates the magnitude of the effect that asset

price declines had on the balance sheets of major financial institutions precisely when

short-term funding dried up.

Institutions in Crisis in 2008

As described above, concerns over the exposure of financial institutions to MBS grew

during 2007 and into 2008, and large banks reported write-downs on mortgage products.

Starting third quarter 2007, major financial institutions—including two commercial

banks (Bank of America and Citigroup) and four investment banks (Bear Stearns,

Lehman Brothers, Merrill Lynch, and Morgan Stanley)—began to report declines in net

earnings. Bear Stearns had substantial exposure to mortgages and mortgage products

beyond the two Bear Stearns-managed hedge funds that declared bankruptcy in 2007,

and investors grew increasingly concerned about the firm’s solvency. On March 12, 2008,

these concerns precipitated a run on the investment bank by its hedge fund clients and

other counterparties. The next day, the bank lost its ability to borrow in the repo market.

To avert panic among investors, the Federal Reserve coordinated the acquisition of Bear

Stearns by JPMorgan Chase—granting a $30 billion loan to JPMorgan to cover potential

losses on Bear’s asset portfolio.

In the ensuing months, a general lack of transparency in exposures to risky assets

greatly increased uncertainty over counterparty credit risk, and fears mounted over the

solvency of other major financial institutions.

46

Throughout the summer of 2008, persistent declines in asset values continued

to weigh on financial institution balance sheets. Eventually, several major financial

institutions neared insolvency. Among them were the two giant GSEs, Fannie Mae and

Freddie Mac, which together held about $1.5 trillion in bonds outstanding. Finally, on

September 7, 2008, growing losses and ongoing deterioration in MBS prices prompted

Treasury Secretary Henry Paulson to put these two GSEs into federal conservatorship,

while explicitly guaranteeing all outstanding GSE securities.

47

Within days, Lehman Brothers, another investment bank heavily exposed to MBS,

experienced funding problems similar to those Bear Stearns had experienced. Like Bear

Stearns, Lehman Brothers was not exceedingly large but was deeply interconnected with

other financial institutions. Concerned about Lehman’s solvency, investors withdrew

45

Ibid. Here the leverage ratio is expressed as a 40 to 1 multiple, meaning that for every $40 in assets, there was

only $1 in capital to cover losses. In discussions of bank regulation, the leverage ratio is generally calculated

as a ratio of equity to assets.

46

Brunnermeier, “Deciphering Liquidity,” 96–98.

47

Ibid., 89.

27 CHAPTER 1: Origins of the Crisis

their funds, refused repo funding, and demanded more collateral on outstanding

commitments. On September 15, 2008, unable to meet investor demand—and without

government assistance or the presence of an acquiring institution—Lehman Brothers

declared bankruptcy. Lehman’s failure triggered panic throughout the U.S. and global

financial systems. Coming on the heels of the previous stages of financial market

turbulence, the panic resulted in one of the most severe financial crises in U.S. history.

The ensuing panic was similar to previous financial panics in the sense that investors lost

confidence in the financial system. Unlike the previous ones, however, this one involved

a run on financial firms not by individual depositors but by other financial firms.

48

When exposure to mortgage-backed securities and derivatives was spread throughout

the financial system, counterparties did not know where the risk was concentrated and

which institution would be next to fail. Widespread uncertainty over the solvency of

major financial institutions led investors to quickly withdraw their exposures to the

financial sector and to hoard cash. In turn, the withdrawal of exposures and the hoarding

of cash led to a general breakdown of intermediation—the “matching” of the funding

market to investors by an agent or third party, such as a bank. For creditors, it was much

easier and safer to withdraw their positions than to check the safety of their investments.

During the weeks after Lehman’s bankruptcy, the general perceived riskiness of private

lending to banks was reflected in a spike in interbank lending rates.

49

The day after the Lehman bankruptcy, another highly interconnected institution—

the American Insurance Group (AIG)—also encountered an acute liquidity shortage.

Like the investment banks, AIG was heavily involved in the credit derivatives business,

particularly in selling CDS. AIG had issued tens of billions of dollars of CDS to insure

against declines in asset values. It had also written CDS to protect against default on

more than $440 billion of bonds. After Lehman declared bankruptcy, nervous investors

demanded additional collateral on AIG’s insurance and derivatives contracts. AIG did

not have the cash. The Federal Reserve quickly organized a rescue, providing an $85

billion loan in exchange for an 80 percent equity stake in the company.

After the Lehman bankruptcy, short-term funding markets, already stressed as

described above, nearly collapsed. MMFs were one market that experienced panic and a

run.

50

Investor redemption requests on MMFs surged, causing a severe liquidity crisis. The

Reserve Primary Fund—an MMF that held debt securities issued by Lehman Brothers—

fell to 97 cents per share, becoming the first money market fund in 14 years to “break

48

Gary Gorton, “Questions and Answers about the Financial Crisis,” NBER Working Paper 15787 (February

2010), 2, http://www.nber.org/papers/w15787.pdf.

49

FCIC, Final Report, 355.

50

MMFs were historically perceived to be safe, liquid investment vehicles that were slightly higher-yielding

substitutes for bank deposits. However, unlike bank deposits, MMFs were not federally insured. MMFs

invested in short-term debt that typically included government securities, certificates of deposit, commercial

paper, repurchase agreements, or tax-exempt securities issued by state or local governments.

28 CRISIS AND RESPONSE: AN FDIC HISTORY, 20082013

the buck” by falling below $1 per share. This event spread panic throughout the MMF

industry, prompting MMF investors to redeem their investments. For example, Putnam

Investments closed its $15 billion Prime Money Market Fund because of “significant

redemption pressure.”

51

During the week when Lehman Brothers declared bankruptcy,

MMF net outflows totaled $169 billion. These outflows caused MMF funding for short-

term debt to drop, affecting sectors that relied on the funding.

In some cases, the investment banks that sponsored MMFs stepped in to support

MMFs facing significant redemptions. The Reserve Primary Fund, however, did not

have a parent company that could provide support. Ultimately, the U.S. government

provided liquidity and guarantees to the entire MMF industry. The Federal Reserve

made liquidity available to money markets through two facilities, the Asset-Backed

Commercial Paper Money Market Mutual Fund Liquidity Facility and the Money Market

Investor Funding Facility, to support the commercial paper market, to help MMFs meet

redemption requests, and to enhance money market investors’ willingness to invest in

money market instruments. In addition, the Treasury provided a temporary guarantee

for MMF shareholders. The guarantee lasted for one year and protected the shares of all

MMF investors for amounts that they held in participating MMFs. The Treasury did not

incur any losses under the program, and its actions helped stabilize the run on MMFs.

52