Visa Merchant Data Standards Manual

Visa Supplemental Requirements

APRIL 2024

© 2024 Visa. All Rights Reserved.

Note: This document is a supplement of the Visa Core Rules and Visa Product and Service Rules. In

the event of any conflict between any content in this document, any document referenced

herein, any exhibit to this document, or any communications concerning this document, and

any content in the Visa Core Rules and Visa Product and Service Rules, the Visa Core Rules and

Visa Product and Service Rules shall govern and control.

Merchant Data Standards Manual Summary of Changes

Visa Merchant Data Standards Manual –

Summary of Changes for this Edition

This is a global document and should be used by members in all Visa Regions.

In this edition, details have been added to include the following new MCCs created:

MCC 3168 – Hainan Airlines

MCC 5723 – Guns and Ammunition Shops (effective July 1, 2024)

The following amendments were also incorporated to facilitate easier merchant designation and classification:

MCC 4829 (Money Transfer) – MCC description has been updated to include “Bill Payments merchants (who are

not eligible and not registered in the CBPS Program) should be assigned with this MCC.”

MCC 5085 (Industrial Supplies (Not Elsewhere Classified) – MCC description has been updated to include

specific examples

MCC 5122 (Drugs, Drug Proprietaries, and Druggist Sundries) – MCC description and services included in this

MCC have been amended and refined per the updated Visa High Integrity Risk MCCs

MCC 5169 (Chemicals and Allied Products (Not Elsewhere Classified)) - MCC description has been updated

to include specific examples

MCC 5399 (Miscellaneous General Merchandise) – Toiletries now qualifies as a merchandise under this MCC

MCC 5912 (Drug Stores and Pharmacies) - MCC description and services included in this MCC have been

amended and refined per the updated Visa High Integrity Risk MCCs

MCC 5967 (Direct Marketing – Inbound Teleservices Merchant) – Services included with this MCC has been

updated to include “Adult content and services including, but not limited to, website subscriptions, video streaming

and audio-text”

MCC 7523 (Parking Lots, Parking Meters and Garages) – the word ‘automobiles’ has been replaced with ‘all

modes of transportation’ to read “Merchants classified with this MCC provide temporary parking services for all

modes of transportation, usually on an hourly, daily, or monthly contract or fee basis”

MCC 7399 (Business Services (Not Elsewhere Classified) – “Cosmetic Distributors” and “Perfume Distributors”

have been included in the list of businesses applicable under this MCC

Merchant Data Standards Manual Table of Contents

Table of Contents

Introduction ............................................................................................................................................. 1

Section 1: Merchant Data Requirements ................................................................................................. 2

Determining a Merchant Name ................................................................................................................. 3

Determining a Merchant Location ............................................................................................................. 9

Determining Merchant Category Codes .................................................................................................. 16

General Requirements................................................................................................................... 16

Mandatory Multiple MCCs ............................................................................................................. 18

Section 2: Merchant Category Code Listing .......................................................................................... 22

Section 3: New MCC or MCC Change Requests ................................................................................. 109

Merchant Data Standards Manual Introduction

April 2024 VISA PUBLIC

1

Introduction

The Visa Merchant Data Standards Manual contains requirements for Merchant/payment

facilitator/marketplace classification, location, and various data elements, including Merchant

location, Merchant Category Codes (MCC), and other VisaNet data formats.

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

2

Section 1: Merchant Data Requirements

This section contains requirements for assigning and formatting the following data elements:

• Merchant name

• Merchant location, Payment Facilitator location, Digital Wallet Operator location,

and Marketplace location (including city, state, and country formats)

• Supplementary Merchant information

• Merchant Category Code (MCC)

Merchant data must be the same as, or consistent with, comparable data throughout a

transaction’s life cycle and on the transaction receipt. Visa retains the right to require

corrections to non-compliant or confusing Merchant data.

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

3

Determining a Merchant Name

General

requirements

The Merchant name is the most important factor in cardholder recognition of transactions.

Correct use helps to minimize copy requests resulting from unrecognizable Merchant

names and reduces costs to Acquirers, Issuers and Merchants.

The Merchant name must be the name most prominently displayed by the Merchant and

by which cardholders recognize the Merchant (while also reflecting the Merchant’s “Doing

Business As” (DBA) name).

Merchants may sometimes use names that do not cause confusion when viewed at the

Merchant premises but may confuse the cardholder if viewed out of context on a

cardholder statement. Examples of such names would include a parking garage named

John’s Farm (that is no longer the site of a farm) or a restaurant named Ship Chandler.

When the content of the Merchant name is inconsistent with the MCC, the Merchant name

must contain extra information that identifies the type of Merchant to the cardholder. In

the example above, the Merchant descriptor for John’s Farm must be John’s Farm

Parking; the descriptor for Ship Chandler must be Ship Chandler Restaurant.

A Merchant with multiple Merchant outlets may add the city, store number, or other unique

identifier to distinguish the specific Merchant outlet.

Example One:

A fuel station is a franchisee of a large retail chain. Accordingly, the retail chain name,

brand, and colors are prominently displayed on the forecourt and inside the shop. The

name of the franchisee is in the window on an A4 notice for legal reasons. The Merchant

name must be the name of the retail chain, possibly with an added indication of the

location.

Example Two:

An individual owns a taxicab that he leases to other drivers to provide taxi services as

part of a large taxi company chain. The taxicab displays the taxi company name and is

painted in the company’s colors. The driver leasing the taxi has his own acceptance

contract. For legal reasons, that driver’s name is on a plate on the dashboard. The

Merchant name must be the name of the taxi company, possibly with the taxicab number

to differentiate it from other taxis that provide services for the same company. The

Merchant name must not be the name of the taxi driver, nor may it be the name of the

owner of the car.

Example Three:

A magazine offers annual subscriptions through postcards inserted in every issue.

Although the magazine is one of several published by the same company, the publisher

is not mentioned on the postcard. The Merchant name must be the name of the magazine,

as that is the name that was displayed to the cardholder. It may only be the name of the

publishing house if the publisher was clearly shown on the postcard as the Merchant.

Payment

Facilitators and

Marketplaces

A Merchant is an entity that represents itself to the buyer as selling services or goods.

If an entity handles payments on behalf of sellers through an online marketplace that

brings together multiple buyers and sellers it may be classified as a Marketplace.

An entity is a Payment Facilitator if it deposits transactions or receives settlement on

behalf of the Merchant but does not sell goods or services to cardholders and cannot

otherwise be categorized as a Marketplace.

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

4

In determining whether an entity is a Merchant, Payment Facilitator, or Marketplace, Visa

looks at each transaction separately. There are a number of entities that operate as the

Merchant for some transactions and operate in a different capacity for other transactions.

Such entities must process each transaction according to the rules that apply to the type

of transaction.

Franchise:

ABC Inc. owns the franchise for The Ultimate Hamburger. ABC’s name is displayed on a

printed sheet of paper in the office window, per government requirements. Everything

else—including the large sign in corporate colors outside the shop, the menu boards, and

the staff uniform—displays the Ultimate name. ABC’s location is indistinguishable from

locations owned and run by Ultimate and locations owned by other franchisees. Any

disputes are resolved with cardholders by Ultimate’s head office. To cardholders, Ultimate

is representing itself as selling the goods. Ultimate qualifies as the Merchant.

Department Store:

DJS is a department store and leases some areas on its ground floor to perfume

companies that own the perfume they sell. The signage outside the shop is DJS, and the

entire store is in their corporate design and color. A customer can take goods from any

counter and pay for them at any cash register in the store. The customer sees the perfume

brand being sold at a unique counter in the store, but they also see unique counters for

different brands of jeans, which are owned and sold by DJS. Any disputes are resolved

with cardholders by DJS customer service division. For the purpose of the test, DJS is

representing itself to the cardholder as selling all the goods in the store, and DJS qualifies

as the Merchant.

Online Marketplace (1):

Corriedale’s runs an online marketplace specializing in sales to sheep farmers. There are

several hundred sellers represented on the website, some are major Retailers and some

are individual sellers. Corriedale does not purchase or supply the goods. Customers using

the website can search for a specific item or a specific seller. In each case, the names of

the Retailers are clearly displayed along with the price of the goods (which can vary by

Retailer), and ratings assigned by customers. The look and feel of each web page

remains that of Corriedale. It is possible to combine and pay for goods from multiple

Retailers in the same transaction. Corriedale handles the payments for sales and

chargebacks and sets the returns policy, but customer disputes are handled by individual

Retailers.

Corriedale has in place a process for resolving disputes between

cardholders and retailers.

Corriedale is not a Merchant—the Retailers on the site

represent themselves as the sellers of the goods, and not Corriedale. Corriedale must

register with Visa as a Marketplace.

Online Marketplace (2)

Specialist Parts of Munich (SPoM) is an online marketplace that brings together buyers

and sellers of vintage car and truck parts in a single location. Sellers must arrange their

own payments, and often choose to use a Payment Facilitator with which the marketplace

has a referral agreement. Sellers may choose their own Acquirer or a different Payment

Facilitator.

SPoM does not qualify as a Marketplace, as it does not handle payments on behalf of its

sellers. The Payment Facilitator with which it has a referral agreement is also not a

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

5

Marketplace, as its primary function is to facilitate payments; it does not bring together

buyers and sellers nor fill many of the other marketplace criteria.

Formatting the

Merchant Name

Visa authorization and clearing systems provide 25 spaces in which to describe the

Merchant name and acquirers are required to be able to use all 25 spaces.

Merchant names longer than 25 characters (this includes letters, blank spaces, and all

symbols) will not fit into the Merchant name field and must be abbreviated (but not just

truncated after the 25

th

character). Information in the Merchant name field must enable

the cardholder to accurately identify the specific Merchant, and the part of the name that

uniquely identifies the Merchant to the cardholder must not be abbreviated. This is shown

in the example below:

Name: NEW YORK HOME HARDWARE DISTRIBUTORS (35 characters)

Possible abbreviations:

N

Y

H

O

M

E

H

A

R

D

W

A

R

E

D

I

S

T

R

.

N

E

W

Y

O

R

K

H

O

M

E

H

D

W

D

I

S

T

R

.

Supplementary

Merchant Name

Information for

Specific

Transactions

In general, the Merchant name field must only contain the Merchant name, as set out

above. However, there are a number of specific exceptions to this rule in the table below.

Note: even for the categories set out below, supplementary data is not permitted if it

makes the content of the Merchant name field confusing or counter to other requirements

(such as abbreviation requirements). In some cases, the Merchant name may not be

truncated at all.

The supplemental data must be static and must appear in all transactions. For example,

if a Merchant outlet chooses to include a location descriptor in the Merchant name field,

it must be the same in every transaction. Two exceptions to this rule are airline/US railway

ticket numbers and the words “No Show”, which need only appear in no show

transactions.

If a Merchant with multiple Merchant outlets chooses to include a location descriptor in

the Merchant name field. It must use the same type of information (for example, city

name) for all its outlets. It must not add the city name for some outlets, the store number

for some outlets and no information for others.

Transaction

Supplementary Data

Required/Optional

For the first

recurring

transaction at

the end of a

trial period,

discounted

introductory

offer, or

promotional

period

After the Merchant name, may contain language to indicate that the recurring

transaction is as a result of a subscription that began with a trial period,

discounted introductory offer, promotional period, etc.

For example: in English, this may be any of the following:

• “End Trial”

• “End Offer”

• “End Free Trial”

• “End Trial Period”

• “End Discount”

• Other similar language

Merchants may use other language or transaction-specific details (for example,

universal resource locator (URL) or order number) to help the cardholder identify

that their trial period, discounted introductory offer or promotional period has

ended, and that the regular price now applies for the subscription.

Optional

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

6

For example:

M

E

R

C

H

A

N

T

N

A

M

E

E

N

D

T

R

I

A

L

Purchase of

goods or

services at an

airline or US

passenger

railway

(“ancillary

purchase”)

A general description of the type of purchase (beverage, meals, seat upgrade,

lounge access, duty free etc.

Information in the Merchant name field must use the following format:

• Merchant name in the first 11 or 12 positions

• A blank in position 12, if applicable

• A general description of the goods or services beginning position 13

For example:

Optional

A

I

R

L

I

N

E

N

A

M

E

D

U

T

Y

-

F

R

E

E

Purchase of an

airline ticket

or US

passenger

railway ticket

Must contain all of the following:

• An abbreviated airline (or US railway) name in the first 11 or 12 positions

• A blank in position 12 if applicable

• Airline (or US railway) ticket identifier beginning position 13

For example:

Required

A

I

R

L

I

N

E

N

A

M

E

1

2

3

4

5

6

7

8

9

0

1

2

3

Purchase at an

AFD

Most fuel is sold under large retail brands, and that brand must be the Merchant

name. Since the brand often has multiple locations in a city, the Merchant is likely

to include a place descriptor such as a city name or a location number. The

required Merchant name must not be abbreviated or truncated in order to place

supplemental information into the Merchant name field.

For example:

B

I

G

B

R

A

N

D

P

E

T

R

O

L

#

3

2

2

Required

Purchase of

Goods or

Services

Additional information may be included after the Merchant name and an asterisk

(*) to indicate an order number, reference number, or other information to identify

the transaction.

If the transaction is an installment transaction, installment information (1 of 2, 2 of

2, etc.) must appear after the asterisk.

For vehicle rental and hotel Merchants, the Merchant name must not be truncated

in order to place supplemental information into the Merchant name field.

Optional

Cash

For a manual cash disbursement at a member location, the disbursing member’s

name must appear first, followed by the disbursing location’s branch, office

number, or other unique identifier.

G

R

E

A

T

B

A

N

K

W

E

S

T

E

N

D

For an automated cash disbursement at a member location, a transaction

descriptor such as “cash” must be used, and at least one of the following:

• Disbursing member name

• Name of the disbursing member’s affiliated domestic, regional, or national

network

• The 3-digit servicing carrier code and a 10-digit transmission control network,

excluding the check digit

• A 3-digit carrier number, 3-digit form number, and 7-digit serial number,

excluding the check digit

B

A

N

C

O

L

O

M

B

I

A

C

A

S

H

B

A

N

C

O

L

C

A

S

H

1

2

3

1

2

3

4

5

6

7

8

9

0

Required

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

7

Original Credit

Transactions

As required by the Visa Direct Original Credit Transaction (OCT) Global

Implementation Guide

Required

No-Show

Transactions

May also include the words “NO SHOW” after the Merchant name.

Optional

Payment

Facilitator

A payment facilitator transaction that contains the Payment Facilitator and

sponsored Merchant identifiers may populate the Merchant name field with

either the sponsored Merchant name (alone), or a combination of both the

sponsored Merchant and Payment Facilitator name, using (i) the name of the

Payment Facilitator (or an abbreviation), (ii) followed by an asterisk (*), and

(iii) the sponsored Merchant name (e.g., Payment facilitator name*Sponsored

Merchant name). It should choose the name that is the more recognizable to

the cardholder.

If a Cardholder accesses the website and/or application of a high integrity risk

Merchant or a high integrity risk sponsored Merchant and is then linked or

forwarded to the website and/or application of a high-risk internet Payment

Facilitator for payment, the name of the high-risk internet Payment Facilitator

must appear in the Merchant name field in conjunction with the name of the

high integrity risk sponsored Merchant.

Acquirers must prohibit agents from utilizing dynamic Merchant descriptors for

Gambling Merchants.

Required

Staged Digital

Wallet

For funding transactions, the Merchant name field must contain the name of

the digital wallet Operator.

For back-to-back funding transactions, the Merchant name field must contain

(i) the name of the digital wallet Operator, (ii) followed by an asterisk (*), and

(iii) the Retailer name.

Required

Marketplace

The Marketplace may use the Marketplace name alone. It may choose to

insert the name of the seller into the Merchant name field, using (i) the name

of the Marketplace (or an abbreviation), (ii) followed by an asterisk (*), and (iii)

the Retailer name.

Required

Business

Payment

Solution

Provider

(BPSP)

The BPSP name must appear with the Supplier name. The BPSP name must be

the Merchant name it registered with Visa. The complete name should appear. An

abbreviation may be used for long names, but it must be easily recognizable.

The field must contain (i) the name of the BPSP (ii) followed by an asterisk (*) and

(iii) the Supplier name, or an abbreviation, (e.g. BPSP name*Supplier name). An

Acquirer must ensure that the BPSP or Supplier name remains consistent for all

transactions.

Required

Consumer Bill

Payment

Servicer

(CBPS)

The CBPS name must appear with the biller name. The CBPS name must be the

Merchant name it registered with Visa. The complete name should appear. An

abbreviation may be used for long names, but it must be easily recognizable.

The field must contain (i) the name of the CBPS (ii) followed by an asterisk (*) and

(iii) the biller name, or an abbreviation, (e.g. CBPS name*biller name). An acquirer

must ensure that the CBPS or biller name remains consistent for all transactions.

Required

Service Fee,

US Region

Must contain the words "Service Fee" after the Merchant name.

Required

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

8

Tipping

(Stand-alone

Transactions)

When tips are given to the person receiving the tip (service staff) as a stand-alone

Visa transaction, Cardholders are unlikely to remember the name of the person to

whom they gave the tip or gratuity. The Merchant name field therefore must

include something the Cardholder recognizes such as the establishment where

the person receiving the tip works. The Merchant name field must also contain the

word “Tip". The name of the person receiving the tip is not required.

Note: These requirements only apply to tips paid directly to the tipped employee in

a stand-alone transaction where the tip represents the entire transaction amount.

Example 1: A tip is paid by a Visa cardholder using their Visa card to Alex, who

provided valet parking service to the cardholder at a golf club named “Famous

Golf Club.” The transaction is processed by a tipping solution provider named

“NewTip” that does not act as, or work with, any payment facilitator. A compliant

merchant name field would be “Tip Famous Golf Club”.

Example 2: A tip is paid by a Visa cardholder using their Visa card to Alex, who

provided valet parking service to the cardholder at a golf club named “Famous

Golf Club.” The transaction is processed by a tipping solution provider named

“NewPF,” which acts as a payment facilitator. A compliant merchant name field

would be “NewPF* Tip Famous Golf Club”.

Example 3: A tip is paid by a Visa cardholder using their Visa card to a band

named “BestBand” that plays in several different places. The transaction is

processed by a tipping solution provider named “NewTip,” which acts as a

payment facilitator. A compliant merchant name field would be “NewTip*

BestBand”.

Note: The requirement to use the word “tip” in the merchant name field is met by

the tipping solution provider’s name.

Example 4: A tip is paid by a Visa cardholder using their staged digital wallet

named “NewWallet,” funded by a Visa card, to a band named “BestBand” that

plays in several different places. The transaction is processed by a tipping

solution provider named “NewTip,” which does not act as, or work with, any

payment facilitator. A compliant merchant name field would be “NewWallet* Tip

BestBand”.

Required

Wire Transfer

Money Order

Transactions,

US Region

Must contain:

• The name of the wire transfer operator used to identify itself to its

customers.

• An asterisk (*)

• The Merchant location at which the money order is issued in the

remaining positions

Required

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

9

Determining a Merchant Location

An Acquirer is responsible for assigning the correct location of each Merchant outlet.

The same location (country) must be disclosed to the cardholder at the time of the

transaction (via the website for electronic commerce Merchants, verbally for telephone

orders, or on the mail order form); used throughout the transaction life cycle (including

but not limited to in the authorization request(s), clearing record, credit transaction, and

chargeback record(s)); and be accurately reflected in the VisaNet record and in fulfilling

any Merchant reporting requirements.

Card-Present

Transactions

For card-present transactions at a Merchant with a fixed location, the Acquirer must

assign the location of the Merchant outlet as the location where the transaction took

place.

Some Merchants do not operate from a fixed location. For an in-transit transaction,

particularly a plane or a ship, the place where the transaction took place is not always

clear. Accordingly, the rules specify a choice of places that the Merchant may use as the

Merchant location for the purposes of a Visa transaction.

For other Merchants that do not operate from a fixed location (such as a Merchant that

travels between different locations), the location must be either the location where the

transaction takes place, or the Merchant’s principal place of business (the fixed location

where a Merchant’s executive officers direct, control, and coordinate the entity’s

activities).

Only the type of Merchant outlet, and not the acceptance device/terminal type, is relevant

in determining whether a Merchant is or is not in a fixed location. For example, an

electronics Merchant may use mPOS devices inside its store. The store is a fixed

location, so the Merchant location must be the address of that store.

Card-Absent

Transactions

The location of a card-absent transaction considers additional factors. The cardholder is

not present at the Merchant outlet when the transaction takes place, and the activities

needed to complete the transaction may occur in different locations, perhaps in different

countries.

A card-absent Merchant must disclose the location of the Merchant outlet (and,

therefore, of the transaction) to the cardholder at the time of the transaction. An e-

commerce Merchant must prominently display the Merchant outlet country to the

cardholder on the same screen as the check-out screen or on a page immediately prior

to the check-out screen. It must not be contained only via a hyperlink.

A Merchant must use its principal place of business as the Merchant outlet location for

card-absent transactions – that is the fixed location where the Merchant’s executive

officers direct, control, and coordinate the entity’s strategy, operations, and activities). A

Merchant may have only one principal place of business for it and its group subsidiaries.

In the case of a corporate group, the Merchant location is determined at the corporate

group level (i.e., as a single entity). For example, this means that a multinational

Merchant must use its principal place of business as the Merchant location and may only

use the country of a subsidiary if that country qualifies as an additional Merchant

location.

Under certain conditions a Merchant may also use other countries as Merchant outlets

in addition to the principal place of business:

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

10

• For travel/lodging Merchants, where a travel agent does not conduct the

transaction, the Merchant location may be any of the following countries:

– For airlines, passenger railways, cruise lines, and other travel Merchants, the

country from which the first leg of travel originates.

– For lodging Merchants, the country in which the stay occurs.

– For car/vehicle rental Merchants, the country in which the vehicle is rented

– For taxi/ride services, the country in which the journey originates

• For the purchase of travel where a travel agent conducts the transaction, the

location of the travel agent determines the Merchant outlet country, regardless of

whether the Merchant is the travel agent or the travel Merchant. The rules for other

card-absent transactions in the next bullet must be used to determine the location

of the travel agent.

• For other card-absent transactions, the Merchant outlet location may also be the

country where the Merchant conducts the business activity directly related to the

provision of the purchased goods or services to the cardholder. To assign an

additional country to a Merchant in this situation, the acquirer must ensure that the

Merchant meets all of the following criteria:

– The Merchant has a permanent location where the Merchant conducts

business activities and where those accountable for the sale or distribution of

the goods or services purchased in the specific transaction decide how

products are sold or distributed. The following are not, in themselves, sufficient

to satisfy these criteria:

1. A post office box, a mail-forwarding address, the address of the Merchant’s

law firm, agent, or vendor, or an email address

2. The location of a payments function, customer service function, servers or

URL, or the presence of a director or investor

– The Merchant assesses sales taxes on the transaction activity. Such taxes

must be assessed on the total amount of the sale of the goods or services.

(“Sales tax” is a generic term for a range of taxes levied on the sale, and

includes sales tax, good and service tax (GST), and value-added tax (VAT).

This condition does not apply when no sales taxes are assessable on the sale

according to local law.

– The location is the legal jurisdiction of the contract that governs the sale of the

goods or services (the transaction)

For clarity, if a card-absent Merchant (except in the case of direct sales by a

travel/lodging Merchant) qualifies for one or more additional Merchant outlet

locations, it may assign an additional location for a transaction only as the

location where the underlying business activity occurs for that specific

transaction.

• Acquirers of digital goods Merchants that qualify for MCCs 5815, 5816, 5817, or

5818 may be granted additional locations after submitting proof of additional

relevant business activity to Visa (including, but not limited to, the location of

servers).

• Within the European Economic Area (EEA), a Merchant may satisfy the criteria for

establishing a card-absent Merchant outlet location if all the relevant business

activity occurs within the EEA. That is, the activity must all occur within EEA

countries, but does not need to occur in a single EEA country. When the qualifying

business activity is spread across multiple EEA countries, the acquirer may assign

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

11

any of those countries as the additional Merchant outlet location. On the other hand,

an EEA country may not be used as a card-absent Merchant outlet location if no

business activity occurs there, or if there is business activity that is not sufficient to

satisfy any of the Visa criteria. For example, an EEA country may be the Merchant

location if there are permanent premises at which employees make decisions on

what goods are sold and the Merchant pays sales taxes on those goods, even

though the jurisdiction for the contract of sale is another EEA country. On the other

hand, if a country just has a post box, or it is the location of only payment

processing, it may not be used, as these are insufficient to fulfil any criterion.

Payment

Facilitators

A payment facilitator location must be the country of its principal place of business and

may be an additional country or countries if all activities specified in the Visa rules occur

in each country.

However, within the Europe Region, the relevant business activity required to establish

a payment facilitator location does not need to occur in a single country. If the required

activity is spread across multiple Europe Region countries, the Acquirer may assign any

of those countries as an additional payment facilitator location. For clarity, all the

activities listed in the Visa rules must occur within the Europe Region, and the Acquirer

may assign as the payment facilitator location any (or any combination) of the countries

in which the required activity occurs. A Europe Region country does not qualify as a

payment facilitator location if no relevant business activity occurs there or if the payment

facilitator does not have a business license there.

Staged Digital

Wallet Operators

(SDWO)

A staged digital wallet operator location must be the country of its principal place of

business and may be an additional country or countries if all activities specified in the

Visa rules occur in each country.

However, within the Europe Region, the relevant business activity required to establish

an SDWO location does not need to occur in a single country. If the required activity is

spread across multiple Europe Region countries, the acquirer may assign any of those

countries as an additional SDWO location. For clarity, all the activities listed in the Visa

rules must occur within the Europe Region, and the acquirer may assign as the SDWO

location any (or any combination) of the countries in which the required activity occurs.

A Europe Region country does not qualify as an SDWO location if no relevant business

activity occurs there or if the SDWO does not have a business license there.

Marketplaces

The location of a marketplace (as defined in the Visa rules) must be the country of its

principal place of business and may be an additional country or countries if all activities

specified in the Visa rules occur in each country.

Retailers that sell goods or services through a qualifying marketplace may be located in

a different country to the marketplace. When that happens, the location of the

marketplace must be used to process the transaction.

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

12

Other Location-

Related

Requirements

Acquirers are responsible for ensuring their Marketplaces or Merchants / Sponsored

Merchants undergo an adequate due-diligence review to establish the correct Merchant

outlet location.

Visa reserves the right to dispute Marketplace or Merchant locations and make a final

determination based on the criteria specified in the Visa Rules or any other information

available to Visa.

Acquirers must ensure that the Marketplaces or Merchants they sign are legitimately

located in their jurisdiction. Acquirers of card-absent Merchants should look at additional

factors (for which a Marketplace or Merchant would already have needed to demonstrate

to carry out the business activity that enabled the sale) to validate that the Merchant

location is genuine, including:

• Any other country of domicile claimed by the Marketplace or Merchant / sponsored

Merchant

• The country of domicile of the Marketplace or Merchant’s sponsored Merchant’s

Agent or Payment Facilitator

• The country

1

most connected to the Marketplace’s or Merchant / Sponsored

Merchant’s website, marketing material, and transaction activity with reference to:

– The currency selected to settle transactions

– The language used to explain the terms and conditions.

– The percentage of international transactions

• The country

2

of the tax authority in which the Marketplace or Merchant assesses

sales taxes.

• The legal jurisdiction of any laws to which the Marketplace or Merchant is subject.

• The fixed address where the Marketplace’s or Merchant’s executive officers direct,

control, and coordinate the entity’s strategy, operations, and activities, or of

operational facilities where the Marketplace’s or Merchant’s core business

processes are managed (for example: product development and management,

research and development, accounting, finance, human resources, information

technology)

• The location of customer support facilities where orders are taken/processed and

inquiries/complaints are processed

Examples

Example 1:

A cardholder makes a purchase on board a ferry traveling between Singapore and

Malaysia. There is no need to determine in which country’s territory the vessel is

travelling at the time of the transaction. Under the Visa requirements, the Merchant

outlet is an in-transit Merchant outlet, and the Merchant may choose the country where

the trip commenced (Singapore), the destination (Malaysia), or the Merchant’s principal

place of business.

Example 2:

A cardholder purchases an air ticket online from the airline website for travel from the

U.S.A. to Japan. The airline is a U.S. airline. In this case, the Merchant outlet location

must be the U.S.A., as it is both the principal place of business for the airline and the

place the journey begins.

1

Within the European Economic Area, acquirers should ensure that these activities occur within an EEA country

2

Within the European Economic Area, acquirers should ensure that these activities occur within an EEA country

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

13

Example 3:

A cardholder purchases an air ticket online from the airline website for travel from

Japan to the USA. The airline is a Singaporean airline. In this case, the Merchant may

choose the Merchant’s principal place of business (Singapore) or the place the journey

begins (Japan).

Example 4:

A cardholder purchases an air ticket from a Canadian travel agent for a flight between

Australia and South Africa. The airline is an Australian airline, and the Merchant name

in the transaction record is that of the airline. The Merchant location is Canada, as that

is the country of the travel agent.

Example 5:

A Merchant headquartered in the U.S.A. hires drivers in Uzbekistan to carry Visa

cardholders, competing against taxis. Cards are lodged with the Merchant’s app and

payment is made as a card-absent payment. The Merchant outlet location must be the

USA, which is the Merchant’s principal place of business, or Uzbekistan, which is the

location where the ride began.

Example 6:

A Merchant using MCC 5817 or 5818 sells software, downloaded through its website.

The Merchant’s principals work and reside in Manila. Unless Visa approves an

exception, the Merchant must use the Philippines as its Merchant outlet location,

because that is the Merchant’s principal place of business. The same company has a

regional hub in Singapore and a call center in Brazil. Both the Singapore and Brazil

offices assess sales taxes on software sold. The Singapore office also has people who

control the pricing and the product design for sales in Asia, and the jurisdiction for the

customer contract is Singapore. The Merchant may use Singapore as an additional

Merchant location to sell the goods priced and designed there. Unless Visa approves

an exception, Brazil does not qualify as a Merchant location, because the employees

there do not manage the development, pricing, and sale of the goods sold in the

specific transaction.

Example 7:

A Merchant sells shoes online to consumers all over the world. The Merchant’s

executive officers work and reside in the UK. The Merchant must use the UK as the

Merchant location, because it is the Merchant’s principal place of business. The same

Merchant has a regional hub in Brazil for all of its Latin America operations and has a

local management team and call center staff, determines pricing, determines marketing

strategy and conducts marketing campaigns, ships merchandise from a warehouse to

all of Latin America, and assesses sales taxes based on Brazilian law. The Merchant

may claim Brazil as an additional Merchant location because business activity is

occurring in Brazil. Furthermore, because the business activity is occurring in Brazil for

all of its Latin America activity, the Merchant may use Brazil as an additional Merchant

location for all countries in Latin America.

Example 8:

An ecommerce maple syrup Merchant has its principal place of business in Canada. It

has permanent locations in Germany, France, Spain, and the Netherlands. Its France

office manages pricing and decisions on which goods are to be sold in Europe. The

Spain office manages distribution. German law is the law of the contract, and the

company pays VAT in Germany on its European sales. The Netherlands office

processes payments. As the business activity may be spread across multiple EEA

countries, and all the required business activity occurs in the EEA, the Merchant may

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

14

choose to assign its Merchant outlet location to one of the EEA countries in which

relevant business activity occurs. In this case, it may choose France, Spain, or

Germany. Payment processing activity alone is not sufficient as business activity, so

the Merchant may not use the Netherlands. It may not use any other country in the

EEA, as there is no relevant business activity.

Example 9:

An online travel agent has its principal place of business in Australia. Its UK office

makes decisions on pricing for UK transactions. Its office in Germany manages other

aspects of the company’s European sales – deciding strategy and marketing,

managing customer relations, and handling disputes. It pays VAT in Germany.

Australian law governs the contract of sale for transactions in all countries. The only

country that may be used as a Merchant outlet location for card-absent transactions is

Australia, as that is the principal place of business. The EEA may not be assigned as a

Merchant outlet location, because not all of the required activities occur in EEA

countries.

Merchant

City

The Merchant city field reflects the city in which the transaction occurred and, for most

transactions, must reflect the city in which the Merchant outlet is located.

Visa authorization and clearing systems provide 13 characters in which to place the

Merchant city information. Whenever possible, the Merchant city should be completely

spelled out and not abbreviated. A clear and discernible city name is required.

For example, use:

S

T

P

E

T

E

R

S

B

U

R

G

Do not use:

S

A

I

N

T

P

E

T

E

R

S

B

Exceptions

For some transaction types, information other than the city name must or may be

included in the Merchant city field:

• Transactions at a Military Base, Embassy, or Consulate

Must contain the name of the country in which the military base, embassy, or

consulate is located.

• Card-Absent Transactions

Must contain the Merchant’s customer service telephone number, the Merchant’s

universal resource locator (URL) or internet/e-mail address

• For the first recurring transaction at the end of a trial period, discounted

introductory offer, or promotional period, may contain language or transaction-

specific details to help the cardholder identify that their trial period, discounted

introductory offer or promotional period has ended, and that the regular price now

applies for the subscription

• Transit Merchant Transactions (MCCs 4111, 4112 and 4131)

In addition to the Merchant city, may include a telephone number or URL through

which the cardholder may obtain transaction information

• Traveling Merchant Transactions

May contain an appropriate descriptive phrase, such as:

– SEMINAR

– ONBOARD TRAIN (PLANE) (SHIP)

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

15

– HOME SALE

– SERVICE CALL

• Travel Agency Transactions – The Merchant city field may contain the name of the

travel agency.

Merchant State

(US Region)

The Merchant state field must include the US state in which the transaction occurred (and,

for most transactions, the state in which the Merchant outlet is located).

Traveling Merchants:

When the Merchant outlet is in the 50 United States or the District of Columbia but not a

fixed location, include “XX” (for BASE II transactions) or “99” (for Single Message System

transactions) in this field.

Military Bases, Embassies, or Consulates:

When the transaction takes place at a US military base, embassy, or consulate located

outside the 50 United States and the District of Columbia, include “XX” (for BASE II

transactions) or “99” (for Single Message System transactions) in this field.

Merchant Country

The Merchant country field must reflect the country in which the Merchant outlet is located.

The correct Merchant country code must be used.

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

16

Determining Merchant Category Codes

The Merchant Category Code (MCC) is a four-digit number assigned to describe a

Merchant’s primary business based on annual sales volume measured in local currency.

In addition, some MCCs identify a specific Merchant or type of transaction.

Visa and its members use MCC data for a range of purposes, including activity tracking,

reporting, and risk management.

It is an important requirement that Acquirers (and their Agents) assign the correct MCC

to each of their Merchants. Visa retains the right to require corrections to MCC

assignments and use.

Any transactions representing the purchase of Non-Fungible Tokens (NFTs) should use

the MCC appropriate for the type of item purchases or the Merchant’s primary business

as per Visa’s regular MCC assignment rules when permitted.

General

Requirements

The following rules apply to the assignment of MCCs:

1. Select the MCC that most accurately describes the Merchant’s business. The MCC,

in most cases, should reflect the primary type of business in which the Merchant is

engaged. If the Merchant has more than one line of business and may qualify for

more than one MCC, the Merchant must either:

• Use the MCC that describes the business with the highest sales volume

(measured in local currency) to process all Visa sales

• Use different MCCs for each line of business.

2. Use “miscellaneous” MCCs (usually ending in “99”) only if there is no MCC specific

to the Merchant’s business. MCC descriptions are very accurate, and Merchants

must only be assigned a “miscellaneous” MCC when no other MCC applies to its

business.

3. Merchants with multiple Merchant outlets must choose the appropriate MCC for each

individual outlet. Electronic commerce websites are Merchant locations in

themselves. A Merchant generally has only one e-commerce Merchant location per

country, however, acquirers may have multiple websites in the same country if there

are different Merchant names or a check-out processes.

4 If there are different businesses operating on the same Merchant premises, each

business must be assigned its own MCC if any of the following apply:

• It operates under a different Merchant name

• It operates in a distinct area

• It has separate points of sale.

For example, lodging Merchants often operate other types of businesses on the

premises (restaurant, flower shop, gift shop, etc.) with separate business names and

payment acceptance devices. These other businesses must use the MCC that

describes the specific business operation. For example, a flower shop in a hotel

should be classified under MCC 5992 (Florists), whether or not it is affiliated with the

hotel property.

5. When applicable, use the unique Merchant-specific MCCs that have been

designated for major travel and entertainment (T&E) Merchants. If an airline, car

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

17

rental, or lodging Merchant has a Merchant-specific MCC, it must be used for all

transactions related to the Merchant’s core business. For example, an airline with its

own MCC should use that MCC for ticket purchase, baggage fees, upgrade fees,

and purchases made on the aircraft. Airline, car rental, and lodging. Merchants that

do not have their own MCCs must use the “generic” MCC for that Merchant type:

4511 – Airlines, Air Carriers (Not Elsewhere Classified), 7512 – Car Rental Agencies

(Not Elsewhere Classified), and 7011 – Lodging – Hotels, Motels, Resorts, Central

Reservation Services (Not Elsewhere Classified).

6. Direct marketing and wholesale club MCCs describe how the Merchant conducts its

business rather than what the Merchant sells or provides. For example, a direct

marketing Merchant sells through catalogs, brochures, telemarketing, direct

mailings, etc. and conducts card-absent transactions. A direct marketing Merchant

can sell any type of product or service physical or digital to consumers but must use

a direct marketing MCC.

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

18

Mandatory

Multiple MCCs

There are a number of cases where a Merchant must be assigned multiple MCCs.

• Automated Fuel Dispensers

A Merchant that deploys Automated Fuel Dispensers (AFD) must use MCC 5542

(Automated Fuel Dispensers) for AFD transactions. If the Merchant also sells other

goods or services, the Merchant must use the appropriate MCC for those

transactions.

• Cash Disbursements at ATMs

A member that deploys ATMs must use MCC 6011(Financial Institutions,

Automated Cash Disbursements) for ATM cash disbursements. All other

transactions (for example, the sale of stamps) at an ATM must use the appropriate

MCC.

• Manual Cash Disbursements

A member that provides manual (face-to-face) cash disbursements must use MCC

6010 (Financial Institutions, Manual Cash Disbursements) for those transactions.

All other transactions at the same Merchant location must use the appropriate

MCC for those transactions (such as MCC 6012 (Financial Institutions –

Merchandise, Services, and Debt Repayment)).

• Quasi-Cash transactions including Crypto Currency Sellers

A Merchant that sells quasi-cash must use MCC 6051 (Non-Financial Institutions –

Foreign Currency, Liquid and Cryptocurrency Assets (for example: Cryptocurrency),

Money Orders (Not Money Transfer), Account Funding (not Stored Value Load),

Travelers Cheques, and Debt Repayment) or MCC 6012 – Financial Institutions –

Merchandise, Services, and Debt Repayment for those transactions even if selling

quasi-cash is not the Merchant’s primary business. Purchases of cryptocurrency

must use MCC 6012 or 6051, as applicable. They must also contain special

condition indicator 7 and the quasi-cash transaction indicator in the authorization

request and special condition indicator 7 in the clearing record. All other transactions

at the same Merchant location must use the appropriate MCC for those transactions.

Merchant Purchases of NFTs can and often do occur in fiat currency, and as such

do not require the use of the cryptocurrency Special Condition Indicator of 7 unless

the Visa transaction actually represents the purchase of the cryptocurrency that is

immediately used to purchase the NFT.

• Money Transfer

Merchants classified with this MCC allow customers to transfer funds via an

electronic funds transfer / wire transfer / remittance (both card-present and card-

absent locations including on the premises of the Merchant and third-party agents

such as casinos, truck stops, or check-cashing storefronts) or via an original credit

transaction (e.g., via Visa Direct or Person to Person [P2P] payments).

• Different businesses in one location

A Merchant must assign different MCCs to different businesses on the same

premises if all of the following apply:

– There are distinct areas in the location for each business.

– Each has its business name / type clearly shown to customers.

– Each business has its own points of sale.

Examples would include a nightclub and restaurant owned by the same company

in separate, but adjacent areas; a coffee shop inside a supermarket, with its own

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

19

branding and payment system; a restaurant inside a hotel that is in its own

separate area and has its own name, branding, and payment system.

• An electronic commerce site with a link to a different website

A Merchant that links from its own ecommerce website to another website must

use the appropriate MCC for each website.

• Payment Facilitator: A payment facilitator is a third party. Accordingly, it must

evaluate the business of every sponsored Merchant, and assign the MCC most

appropriate to the sponsored Merchant’s business.

• Gambling

In a card-present environment, a Merchant that conducts gambling transactions

must use MCC 7995 (Betting, including Lottery Tickets, Casino Gaming Chips, Off-

Track Betting, Wagers at Race Tracks and games of chance to win prizes of

monetary value) for those transactions. If the Merchant also sells other goods or

services, it must use the appropriate MCC for the other services.

• Card-absent environment: If the Merchant conducts online gambling transactions,

however, it must use MCC 7995 for all transactions, even if gambling is not the

Merchant’s primary business.

• US Merchants: Lottery and gambling transactions that qualify for MCC 7800, 7801

and/or 7802 must use the applicable MCC for all transactions even if gambling is

not the Merchant’s primary business. If the Merchant also sells other goods or

services, it must use the appropriate MCC for the other services.

• Multiple lines of business, one or more of which is considered “high integrity

risk”

A Merchant that has multiple lines of business in the same location must assign a high

integrity risk MCC to the line of business that is considered high integrity risk and another

MCC to other businesses that are not considered high integrity risk. Current high integrity

risk MCCs are:

For all Card-Absent transactions using the following MCCs:

– 5122 (Drugs, Drug Proprietaries, Druggist Sundries)

– 5912 (Drug Stores, Pharmacies)

1

– 5966 (Direct Marketing – Outbound Telemarketing Merchants

– 5967 (Direct Marketing – Inbound Telemarketing Merchants)

– 5993 (Cigar Stores and Stands)

1

– 7273 (Dating and Escort Services)

– 7995 (Betting, including Lottery Tickets, Casino Gaming Chips, Off-Track Betting,

Wagers at Race Tracks and games of chance to win prizes of monetary value)

For certain Card-Absent Transactions using the following MCCs:

– 4816 (Computer Network/Information Services), for the sale of access to cyber lockers

or remote digital file-sharing services

- 6211 High Integrity Risk Financial Trading Platforms (card absent)

- 5968 Subscription “Negative Option” Merchants (card absent)

– 5816 (Digital Goods – Games), for Transactions involving skilled game wagering (for

example: daily fantasy sports)

– 6051 and 6012 Crypto Merchants: exchanges, wallet providers or on-ramp providers

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

20

(card absent) with transactions required to use Special Condition Code 7

1 In the AP Region, Canada Region, CEMEA Region, Europe Region, LAC Region: Applies only if the Merchant conducts

transactions other than domestic transactions

Optional Multiple

MCCs

If a Merchant or marketplace sells more than one type of merchandise or has more than

one line of business, it must use the MCC that best describes the business with the

highest sales volume (measured in local currency) to process all Visa sales. The acquirer

and the Merchant may determine that an additional MCC and Merchant or marketplace

identifier is appropriate for each different line of business. A Marketplace that sells

multiple lines of goods may use MCC 5262 (Marketplaces). Visa strongly recommends

that the MCCs assigned to Merchants are reviewed periodically to ensure accuracy in

order to limit potential compliance complaints

Examples of

Multiple MCCs

Example One:

A Merchant sells books, stationery, and newspapers, and also has a music CD

department. Book sales make up the majority of the Merchant’s business, so the correct

MCC is 5942 (Book Stores).

Example Two:

A Merchant operates a restaurant and nightclub. In the restaurant, which is upstairs,

customers are served dinner; the nightclub, which is downstairs, charges a cover and

serves drinks. Each floor has its own business name on the door, and they have separate

places to pay and separate acceptance device. The Merchant must use two different

MCCs: 5812 (Eating Places, Restaurants), and 5813 – (Drinking Places (Alcoholic

Beverages), Bars, Taverns, Cocktail Lounges, Nightclubs, and Discotheques).

Example Three:

A Merchant operates a beauty salon that sells hair products in the front of its store, and

a day spa in the rear of the building. Both businesses use the same DBA name, and

both operate using the same acceptance device near the front door of the shop. Initially,

the salon did the majority of the business, using MCC 7230 (Beauty and Barber Shops).

Recently, the spa has generated more in sales, and the potential for growth is apparent.

For this business, the Merchant now has two choices:

• Change MCC to reflect the change in business and use 7298 (Health and Beauty

Spas) as the only MCC

• Continue to use 7230 (Beauty and Barber Shops) for the salon, and use a

separate acceptance device for the spa, using 7298 (Health and Beauty Spas).

If the spa uses its own name and starts using its own acceptance device, the

Merchant must use both MCCs.

Example Four:

A local county government office allows community members to pay for property taxes

with a Visa card, using MCC 9311 (Tax Payments). The county also owns and operates

a ballpark and accepts registrations from the youth athletic leagues. The government

office would like to use the same MCC for both situations. Based on the specificity of

MCC 9311 for tax payments, it is inappropriate for the county to accept the ballpark

registrations using this MCC. In this example, the office must use 9399 (Government

Services, not elsewhere classified) because it is a payment to the county government

that does not fall under any other government related MCC.

Example Five:

John’s Walk and Carry sells shoes and luggage on the internet. The majority of goods

sold through the website are shoes, so the Merchant must use MCC 5661 (Shoe Stores).

The Merchant may also use 5948 (Luggage and Leather Goods Stores) even though it

is only required to use the one MCC for this Merchant outlet. If the Merchant decides to

split the different businesses into different websites with separate check-out processes

Merchant Data Standards Manual Section 1: Merchant Data Requirements

April 2024 VISA PUBLIC

21

but with links between the sites, they are now considered two different Merchant outlets

and must now use different MCCs to reflect the different businesses.

Example Six:

A service station uses AFDs to sell fuel on the forecourt and permits patrons to pay for

petrol inside as well. The service station also sells a small amount of oil, drinks and

snacks. The Merchant must use 5542 (Automated Fuel Dispensers) for the AFD sales,

and 5541 (Service Stations with or without Ancillary Services) for their non-AFD sales.

Merchant Data Standards Manual Section 2: Merchant Category Code Listing

April 2024

VISA PUBLIC

22

Section 2: Merchant Category Code Listing

MCCs are listed in numeric order with a full definition for each MCC.

The MCCs and descriptions have been derived from Standard Industrial Classification

(SIC) Codes and the International Organization for Standardization (ISO) Codes. Please

note that Visa MCCs and SIC codes do not always correspond. In many cases, Visa has

consolidated several SIC codes into one MCC to manage the number of MCCs. In other

cases, such as for T&E and direct marketing Merchants, Visa established MCCs that do

not have corresponding SIC codes.

Merchant Data Standards Manual Section 2: Merchant Category Code Listing

April 2024

VISA PUBLIC

23

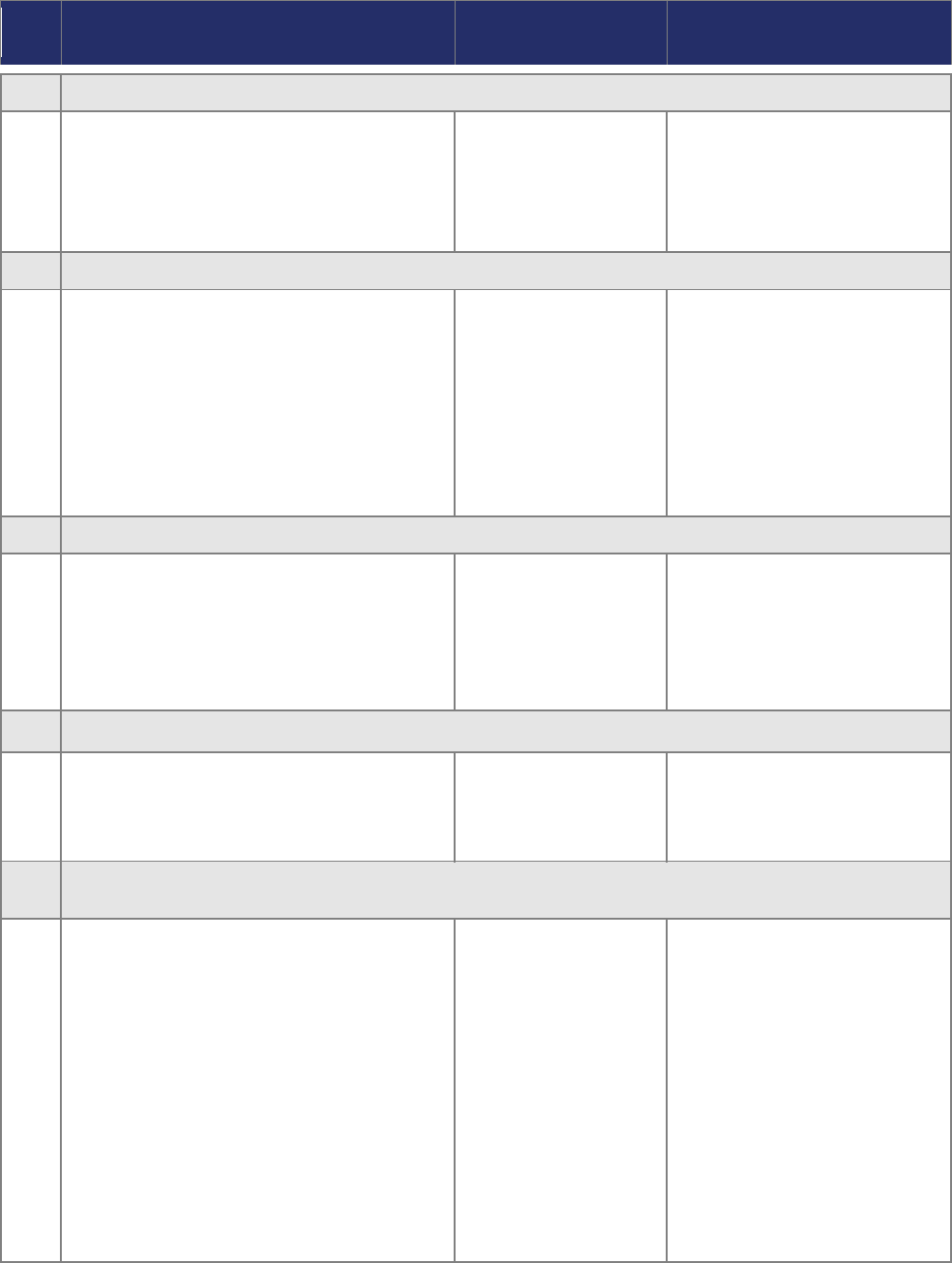

MCC

MCC Title/

MCC Description

Included in this MCC

Similar Merchants

0742

Veterinary Services

Merchants classified with this MCC are licensed

practitioners of veterinary medicine, dentistry, or

surgery. This MCC includes medical practitioners of

pets (e.g., dogs, cats), livestock (e.g., cattle, horses,

sheep, hogs, goats, poultry), and large or exotic

animals.

Animal Doctors, Hospitals

Clinics – Pet

Hospitals – Pet

Pet Clinics

Services – Veterinary

5995 – Pet Shops, Pet Foods and

Supplies Store

0763

Agricultural Co-operatives

Merchants classified with this MCC provide farm

management services or engage in farming

operations. Also included in this MCC are

associations and cooperatives that provide assistance

and services to farmers in farm management. These

services include, but are not limited to financial

assistance, management or complete maintenance of

crops, soil preparation, planting and cultivating, aerial

dusting and spraying, disease and insect control,

weed control, and harvesting crops.

Farm Management

Services

Orchards

Vineyards

0780 – Landscaping and Horticultural

Services

4225 – Public Warehousing and

Storage – Farm Products, Refrigerated

Goods, Household Goods, and Storage

0780

Landscaping and Horticultural Services

Merchants classified with this MCC provide landscape

planning and design services. This MCC also

includes Merchants that offer a variety of lawn and

garden services (e.g., planting, fertilizing, mowing,

mulching, seeding, spraying, sod laying).

Gardening Services

Horticulture Services

Services – Gardening

Services – Horticulture

Services – Landscaping

5193 – Florist Supplies, Nursery

Stock and Flowers

5261 – Nurseries and Lawn and

Garden Supply Stores

1520

General Contractors – Residential and Commercial

Merchants classified with this MCC are general

contractors primarily engaged in construction of

residential and/or commercial buildings. This MCC

includes contractors that perform new construction as

well as remodeling, repair, additions, or alterations.

Building Contractors –

Residential, Commercial

Construction Companies

Contractors – General

Contractors – Residential,

Commercial

1711 – Heating, Plumbing, and Air

Conditioning Contractors

1731 – Electrical Contractors

1740 – Masonry, Stonework, Tile

Setting, Plastering and Insulation

Contractors

1750 – Carpentry Contractors ........

1761 – Roofing, Siding, and Sheet

Metal Work Contractors

1771 –Concrete Work Contractors

1799 – Special Trade Contractors

(Not Elsewhere Classified)

1711

Heating, Plumbing, and Air Conditioning Contractors

Merchants classified with this MCC are contractors

that provide heating, plumbing and air conditioning

services. This MCC includes contractors that perform

air system balancing and testing, drainage system

installation, furnace repair, irrigation system

installation, refrigeration and freezer work, sewer

Air Conditioning

Contractors

Contractors – Air

Conditioning

Contractors – Heating

1520 – General Contractors –

Residential and Commercial

5074 – Plumbing and Heating

Equipment and Supplies

1799 – Special Trade Contractors

(Not Elsewhere Classified)

Merchant Data Standards Manual Section 2: Merchant Category Code Listing

April 2024

VISA PUBLIC

24

MCC

MCC Title/

MCC Description

Included in this MCC

Similar Merchants

hookups and connections, solar heating, sprinkler

system installation and water pump installation and

servicing.

Contractors – Plumbing

Heating Contractors

Plumbing Contractors

1731

Electrical Contractors

Merchants classified with this MCC are contractors

that provide electrical work such as fire alarm

installation, sound equipment installation,

telecommunications equipment installation,

cable/internet installation, and telephone and

telephone equipment installation.

Contractors – Electrical

1520 – General Contractors –

Residential and Commercial

1799 – Special Trade Contractors

(Not Elsewhere Classified)

1740

Masonry, Stonework, Tile Setting, Plastering and Insulation Contractors

Merchants classified with this MCC are contractors

that perform masonry work, stone setting and other

stone work, tile setting, plain and ornamental

plastering, and insulation. This MCC also includes

contractors that perform bricklaying, ceramic and

marble work, mosaic work, acoustical improvements,

and drywall construction.

Contractors – Insulation

Contractors – Masonry

Contractors – Plastering

Contractors – Stonework

Contractors – Tile Setting

Insulation Contractors

Plastering Contractors

Stonework Contractors

Tile Setting Contractors

1520 – General Contractors –

Residential and Commercial

1799 – Special Trade Contractors

(Not Elsewhere Classified)

1750

Carpentry Contractors

Merchants classified with this MCC are contractors

that perform carpentry work. This MCC includes

contractors that do cabinet work at the construction

site, framing, trim and finish work and window and

door installation.

Contractors – Carpentry

1520 – General Contractors –

Residential and Commercial

1799 – Special Trade Contractors

(Not Elsewhere Classified)

1761

Roofing, Siding, and Sheet Metal Work Contractors

Merchants classified with this MCC are contractors

that install roofing and/or siding and do sheet metal

work. This MCC includes contractors that perform

architectural sheet metal work, ceilings and skylight

installation, duct and gutter installation, and roof

spraying, painting or coating.

Contractors – Roofing

Contractors – Sheet

Metal Work

Contractors – Siding

Sheet Metal Work

Contractors

Siding Contractors

1520 – General Contractors –

Residential and Commercial

1799 – Special Trade Contractors

(Not Elsewhere Classified)

1771

Concrete Work Contractors

Merchants classified with this MCC are contractors

that perform concrete, cement or asphalt work. This

MCC includes contractors that construct private

driveways and walks of all materials. Also included in

this category are contractors that pour concrete for

foundations and perform grouting work and concrete

patio and sidewalk construction.

Asphalt Contractors

Cement Contractors

Contractors – Concrete

Work

1520 – General Contractors –

Residential and Commercial

1799 – Special Trade Contractors

(Not Elsewhere Classified)

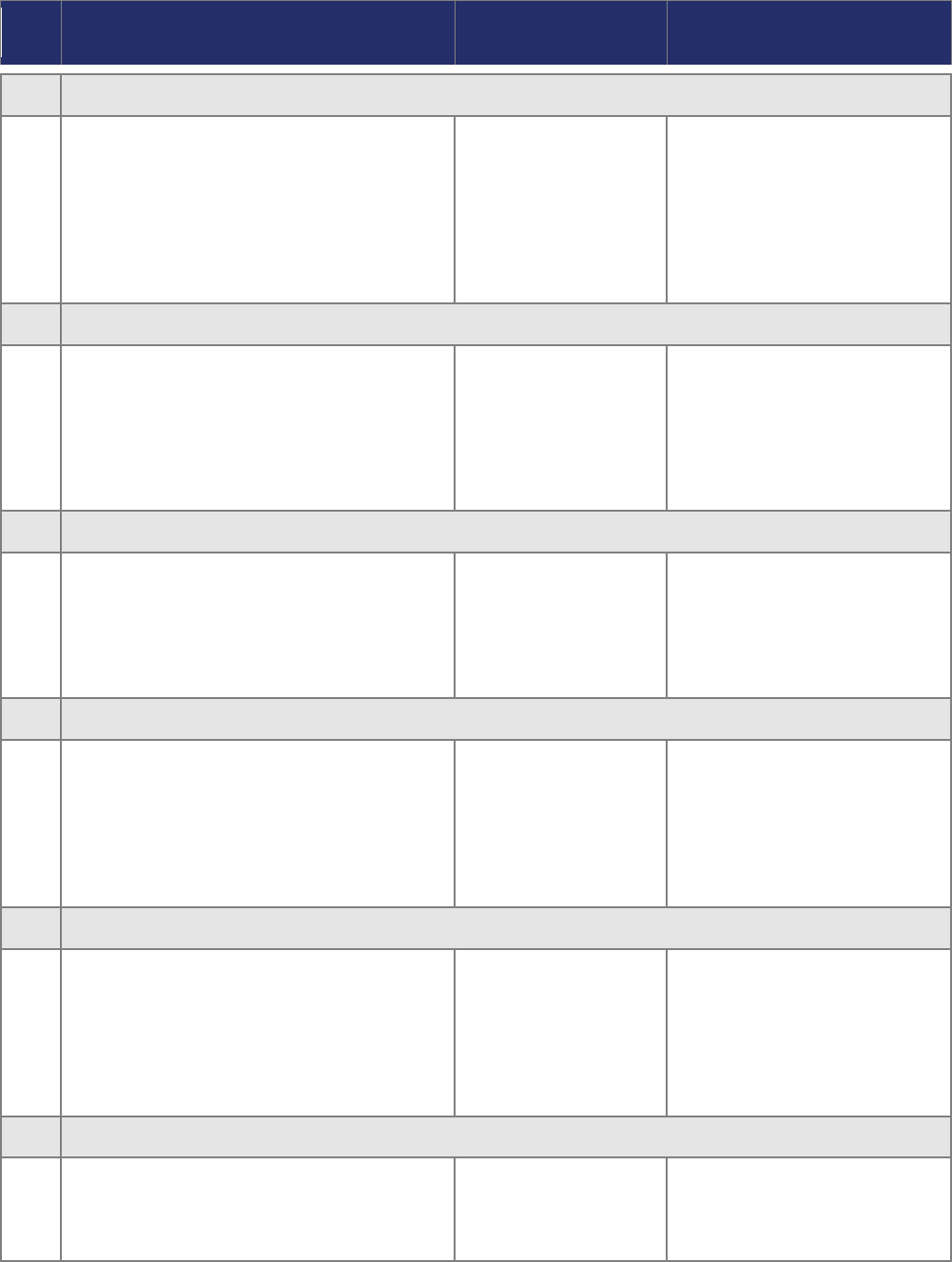

Merchant Data Standards Manual Section 2: Merchant Category Code Listing

April 2024

VISA PUBLIC

25

MCC

MCC Title/

MCC Description

Included in this MCC

Similar Merchants

1799

Special Trade Contractors (Not Elsewhere Classified)

Merchants classified with this MCC are special trade

contractors that perform construction work not

covered with a more specific MCC. This MCC

includes contractors that perform jobs such as awning

installation, bathtub refinishing, fence construction,

fire escape installation, house moving, home window

replacement, garage door installation, ornamental

metal work, swimming pool construction, glasswork,

well drilling, wallpaper services, and waterproofing.

Contractors – Decorating

Contractors – Demolition

Services

Contractors – Glasswork

Contractors – Painting,

Home and Building

Contractors – Paper

Hanging

Contractors – Special

Trade Contractors

Contractors – Welding

Contractors – Well

Drilling

Decorating Contractors

Decorators – Interior

Demolition Services

Garage Door Installation

Glasswork Contractors

Interior Decorators

Window Replacement

Miscellaneous Special

Contractors

Painting Contractors –

Home, Building

Paper Hanging

Contractors

Services – Demolition

Wallpaper Hangers

Welding Contractors

Well Drilling Contractors

1520 – General Contractors –

Residential and Commercial

2741

Miscellaneous Publishing and Printing

Merchants classified with this MCC engage in

business-to-business or wholesale printing, publishing

and/or bookbinding activity. This includes Merchants

that print or publish maps and atlases, business

newsletters, directories, sheet music, paper patterns,

technical manuals and papers, telephone directories

and yearbooks.

Bookbinding Services

Printing Services

Publishing Services

Services – Bookbinding

Services – Publishing,

Printing

5192 – Books, Periodicals and

Newspapers

5942

–

Book Stores

7338

–

Quick Copy, Reproduction,

and Blueprinting Services

2791

Typesetting, Plate Making and Related Services

Merchants classified with this MCC perform business-

to-business or wholesale typesetting for the printing

trade and those that make plates for printing

purposes. These Merchants are involved in

advertisement typesetting, phototypesetting,

computer-controlled typesetting, and color

separations. This MCC also includes Merchants that

make positives and negatives from which offset

Plate Making Services

Services – Plate Making

Services – Typesetting

2741

–

Miscellaneous Publishing

and Printing

7338

–

Quick Copy, Reproduction,

and Blueprinting Services

Merchant Data Standards Manual Section 2: Merchant Category Code Listing

April 2024

VISA PUBLIC

26

MCC

MCC Title/

MCC Description

Included in this MCC

Similar Merchants

lithographic plates are made. These establishments

do not print from the plates they make but prepare

them only for use by other Merchants. This MCC also

includes Merchants that provide engraving or

embossing services for printing purposes, such as

engraving on wood, rubber, copper, or steel, or

photoengraving.

2842

Specialty Cleaning, Polishing and Sanitation Preparations

Merchants classified with this MCC engage in the

business-to-business or wholesale manufacture of

polishes for wood, metal, and other materials as well

as cleaning solutions, industrial and household

disinfectants, and other sanitation preparations. Also

included in this MCC are Merchants that sell non-

personal deodorants, waxes and dressings for

fabricated leather and other materials, wax removers,

dry cleaning fluid and chemicals, rust and stain

removers, wallpaper cleaners, and window cleaning

solutions.

Cleaning Preparations

Materials – Cleaning,

Polishing, Sanitation

Polishing Preparations

Sanitation Preparations

5085 – Industrial Supplies

(Not Elsewhere Classified)

5169 – Chemicals and Allied Products

(Not Elsewhere Classified)

Airlines and Air Carriers

MCC

Merchant Name

Required Name in Authorization Request/Clearing Record

3000

UNITED AIRLINES

UNITED AIR

3001

AMERICAN AIRLINES

AMERICAN AIR

3002

PAN AMERICAN

PAN AM AIR

3003

EUROFLY AIRLINES

EUROFLY AIR

3004

DRAGON AIRLINES

DRAGONAIR

3005

BRITISH AIRWAYS

BRITISH AWYS

3006

JAPAN AIRLINES

JAL AIRLINE

3007

AIR FRANCE

AIR FRANCE

3008

LUFTHANSA

LUFTHANSA

3009

AIR CANADA

AIR CANADA

3010

KLM (ROYAL DUTCH AIRLINES)

KLM AIRLINE

3011

AEROFLOT

AEROFLOT

3012

QANTAS

QANTAS AIR

3013

ITA AIRWAYS (FORMERLY ALITALIA)

ITA AIRWAYS (FORMERLY ALITALIA)

3014

SAUDI ARABIAN AIRLINES

SAUDIA AIR

3015

SWISS INTERNATIONAL AIRLINES

SWISSINTAIR

3016

SAS

SAS

3017

SOUTH AFRICAN AIRWAYS

SAA AIRWAYS

3018

VARIG (BRAZIL)

VARIG

3019

EASTERN AIRLINES