COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

1

MARKETER EMAIL TRACKER 2019

Contents

Contents ................................................................................................................................................................................ 1

Introduction .......................................................................................................................................................................... 2

Foreword - dotdigital ............................................................................................................................................................ 3

Foreword – DMA Email council ............................................................................................................................................ 4

Executive summary .............................................................................................................................................................. 5

Marketing landscape .......................................................................................................................................................... 6

Marketing preferences ......................................................................................................................................................... 6

The GDPR eect .................................................................................................................................................................... 7

Practices & understanding .................................................................................................................................................. 9

Automation and segmentation ........................................................................................................................................... 9

Email Testing ......................................................................................................................................................................... 10

Measurement & value .......................................................................................................................................................... 12

Relevance and eectiveness ................................................................................................................................................ 12

ROI and lifetime value .......................................................................................................................................................... 12

Receiving & content ............................................................................................................................................................. 14

Frequency .............................................................................................................................................................................. 14

Relevance .............................................................................................................................................................................. 15

Sign-ups & unsubscribes ...................................................................................................................................................... 17

Sign-ups ................................................................................................................................................................................. 17

Unsubscribes ......................................................................................................................................................................... 17

Future expectations .............................................................................................................................................................. 19

Methodology ........................................................................................................................................................................ 20

About the DMA ..................................................................................................................................................................... 21

About dotdigital ................................................................................................................................................................... 22

Copyright and disclaimer ..................................................................................................................................................... 23

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

2

MARKETER EMAIL TRACKER 2019

Welcome to the DMA Marketer Email Tracker 2019. It’s the rst time we’ve recorded the thoughts of marketing

professionals about their use of email – and the effectiveness of the channel – since the implementation of the

new GDPR regulations in May 2018.

This report offers a positive view of the email marketing landscape since that date. For marketers, email

remains the core of effective multichannel campaigns. It’s also a favoured channel of consumers, too, as

reected in our recent ‘Consumer email tracker 2019’ report.

The good news for proponents of email marketing is that ROI is increasing; marketers are predicting an

increase in investment in the channel; they’re also bullish about their ability to measure its effectiveness and

their overall competence in the discipline of email marketing.

Importantly, they tell us they are also testing more campaigns – a crucial strategy in the quest to boost

effectiveness. Almost all of the measures outlined above have shown an upward trend in performance since

the 2017 tracker. Marketers can also point to a downturn in opt-out rates and spam complaints, a testament to

their efforts to improve data and comply with the GDPR. Their hard work is already bearing fruit.

There’s always room for improvement. There seems to be a gap in features of email marketing that marketers

believe are cutting-edge, but to which consumers are indifferent. Content, for instance, is not getting the cut-

through it seeks. Meanwhile, limited resource and budget, and a lack of condence at mid and junior levels

are causing consternation.

Overall, however, the results are very encouraging and this current success begs the question: are we now

entering the golden age of email marketing?

Rachel Aldighieri

MD at the DMA

Introduction

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

3

MARKETER EMAIL TRACKER 2019

dotdigital is delighted to be sponsoring the DMA Marketer tracker again – and for the rst time following our rebrand

from ‘dotmailer’ to ‘dotdigital’. The opinion of every marketer who contributed to this study will provide food for

thought, particularly in assessing the impact of the GDPR.

The DMA’s meticulous research continues to empower the digital marketing community as a whole. On a personal

note, it pleases me to see that marketers credit email as the cornerstone of their marketing strategy – powerful on its

own, but even more potent when used in conjunction with other channels like social media and mobile.

What struck me most in this report is that email ROI has shot up from £32 to £42 – email’s return on investment is

undeniable. As such, marketers are measuring ROI more than ever before; many are able to access the tools they need

to quantify the impact of email. Moreover, marketers may have beneted from better quality email addresses in their

arsenal, post GDPR.

While limited budget and resources continue to worry, it’s nice to see that marketers are growing condent in

their ability to dominate on email. Adopting more advanced tactics, they are unlocking sales, generating customer

engagement, and maximising brand loyalty.

While condence has boosted overall, it’s disappointing to see that marketers who feel they have basic or no

knowledge at all has increased by 15%. Common business challenges could be to blame, such as no access to proper

training, limited resources, and disparate or insucient data. The only way to mitigate the eects will be to invest

more in upskilling marketers with additional email tactics.

Consumers, like marketers, also favour email. They use it more than any other channel to engage with brands.

But this doesn’t mean that companies are scaling down other channels. In 2018, businesses integrated email with

the activities of seven other channels. We view this as a big step forward towards better omnichannel marketing

experiences.

It is interesting to see that the lifetime value of an email address continues to increase – 33% year on year – in line

with a strong return on investment. Both B2B and B2C brands value email as a reliable and protable engagement

tactic, despite any concerns they may have had over the GDPR.

25 May 2018 was a date that loomed forever in marketers’ minds. However, ten months after the GDPR came into

eect, it’s fair to say that its impact hasn’t been as adverse as expected. In fact, 56% of marketers feel positive about

the eects of the legislation. Just 20% feel negative about the new regulation – skewed slightly towards B2Cs,

perhaps due to the upheaval of handling changes to their larger databases.

This study also revealed similar ndings to our very own benchmark report from last year, Hitting the Mark. We

discovered that 66% of brands are not practicing any email segmentation, while the DMA has found that only 43%

of campaigns are segmented. While this clear correlation in our research is reassuring, it’s discouraging to see that

brands are not using their data to segment eectively. Additionally, research found that a quarter of campaigns are

neither segmented nor automated. Consumers today carry the expectation of a personalized experience. So, we hope

that by 2020 there will be a higher adoption rate of these customer engagement tactics – the tools and the data are

there for the taking.

Phil Draper

Chief Marketing Ocer at dotdigital

Foreword - dotdigital

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

4

MARKETER EMAIL TRACKER 2019

Email continues to be the pre-eminent channel for marketing communications.

This stands up, regardless of the metric you choose to measure it by reach, penetration, cost, ROI, agility, etc – the list

is long and impressive.

What’s more, email’s lead over rival channels may well have increased with this year’s tracker, indicating both lifetime

value and return on investment have increased. While the phrase, “10 years ago they said email was dead” is in danger

of morphing from triumphant sloganeering to cliché, it is nevertheless true that email is in robust health. This is an

astonishing achievement given the digital landscape now compared to a decade ago.

As usual, there are alarm bells which demand attention. Email may be the most eective channel, but marketers

profess more ignorance than ever; coalescing around those who are knowledge heavy with those who are

knowledge light.

Email’s handmaiden is technology, and it has to function inside a bewildering landscape of CRM and CMS systems,

data silos, ESP and BI platforms, never mind integrating with all of the other channels — and that’s before we’ve even

got onto the subject of GDPR. To borrow a Rumsfeldian terminology, perhaps this is the marketer confessing their

known unknowns?

Finally, a word on GDPR. Before its implementation, something not unlike panic had set in among many. Was

legitimate interest or informed consent the best strategy – or both? Would marketing lists be decimated or would a

new era of opted-in consumers show those lists to be largely cha in the rst place?

Less than a year into the new regime, marketers appear to have transitioned from wary to hopeful. There is increased

optimism around the benets of better targeting and relevancy while the accompanying reduction in spam

and unsubscribe rates is both noted and welcomed. Perhaps this will change when the ICO make their rst big

prosecution under the new legislation, but the disaster it was sometimes pitched as a precursor to looks to have been

wildly exaggerated.

This time next year of course, the overwhelming subject on marketer’s minds should be Brexit. Given the chaos and

indecision around its implementation however, the only thing one can say with any condence — Brexit or no Brexit

– is that email will still be the marketing channel of choice.

Probably…

Marcus Gearey

Chair of the DMA Email council’s research hub &

Analytics manager, Zeta Global

Foreword – DMA Email council

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

5

MARKETER EMAIL TRACKER 2019

Email remains the key strategic channel according to marketers (91% rated important), followed by social media

(83%).

Main challenges include budget and internal resource (42%) and data related-challenges (38%).

The majority of marketers (56%) feel positive about the impact the GDPR is having on their operations, with just a

fth feeling negative about the new regulations.

The primary objectives of email campaigns are sales (62%), engagement (50%), brand awareness (47%) and building

loyalty (45%).

Marketers are more condent in their abilities than in the 2018 email tracker: those professing good or advanced

ability has risen from 30% to 40% since the previous survey.

However, the proportion feeling they have basic or no knowledge has climbed from 9% to 24% since 2015.

Almost two thirds (62%) say they are measuring ROI — the highest-ever result for this question. B2C marketers are

particularly condent, with almost three quarters (71%) able to make the calculation.

ROI from email marketing now stands at just over £42 for every pound spent; a rise of almost £10 since

the previous study.

Lifetime value (LTV) of each individual email address has also risen sharply by 33% year-on-year. Moreover, LTV is

perceived higher in B2C (£41) than B2B (£35).

Only 55% of marketers think more than half of all the emails leaving their organisation are relevant to the individual

recipient.

59% of marketers immediately action unsubscribes and no further emails are sent to the individual. However, 23% of

consumers claim opting out makes no dierence as they still get messages.

76% report an increase in open rates in the past 12 months; 75% say click-throughs are higher; 51% say ROI has risen.

Opt-out rates have decreased according to 41%, and 55% say spam complaints are also down — further evidence of

the GDPR eect.

Respondents expect the proportion of marketing budgets spent on email to climb to almost 17%, compared to 11%

the last time they were asked. But 57% also say email marketing costs will increase.

Executive summary

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

6

MARKETER EMAIL TRACKER 2019

Marketing preferences

When asked about the strategic importance of a number of marketing channels, email remains the key channel (91%

rated important), followed by social media (83%). Phone was named as the third-most important channel (79%),

perhaps surprisingly, with face-to-face (77%) and online (72%) also faring well. The results mirror other recent DMA

surveys, such as the ‘Customer Engagement 2019: Marketers’ view’.

Only half of marketers suggest direct mail/post is strategically important. This is also surprising, as the DMA’s research

into Customer Engagement has shown that post is a trusted medium among both consumers and marketers — but

its use doesn’t strongly reect that sentiment.

Strategically speaking, how important are the following marketing channels for your organisation?

In terms of consumers’ views, from the ‘Consumer email tracker 2019’, they also prefer email as a marketing channel

ahead of any other (59%). More than one in 10 are willing to engage via the traditional methods of face-to-face (12%),

phone (11%) and post/direct mail (11%).

Strikingly, several channels appear to be overvalued by marketers. In particular, phone (11%) and social media

(8%) are eschewed by most consumers. There is a smaller gap, however, for SMS/text messaging (20%), suggesting

consumers are more willing to receive communications this way – presumably service messages and reminders.

The research also shows that, on average, in 2018 businesses integrated email with the activities of 7 other channels

— a slightly higher trend for B2C businesses and large enterprises.

Website and organic social media (both 57%) are named as the main choices by marketers integrating email into

other channels, followed by paid social and CRM technology (both 54%).

There is still a relative lack of integration with other technologies such as segmentation platforms (14%), messenger

apps (16%) and online chat (21%). Most email marketers use in-house solutions to manage their programmes (61%),

though more than a third (39%) outsource.

Marketing landscape

50%

53%

36%

18%

15%

15%

6%

3%

12%

6%

9%

10%

7%

7%

10%

5%

38%

41%

54%

72%

77%

79%

83%

91%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Messenger app

Text/SMS

Post/direct mail

Online

Face-to-face

Phone

Social media

Email

Unimportant Neutral

Important

MARKETER EMAIL TRACKER 2019

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

7

Objectives & challenges

Broadly in line with previous years, the primary objectives of email campaigns are sales (62%), engagement (50%),

brand awareness (47%) and building loyalty (45%). Customer service was named by just a quarter.

There were some clear dierences by organisation type, with 60% of B2C organisations using email to engage

customers, compared to 38% in B2B. The reverse was true for building brand awareness, which scored 56% in B2B but

29% in B2C.

Looking at the challenges to successfully executing email marketing programmes, marketers remain consistent

with previous surveys. Aspects of budget and resource were the main issue (42%), alongside several data-related

challenges such as lack of data, data silos and data degradation — which added up to 38%. A lack of strategy or

leadership at their organisation was a problem for a quarter, with a similar level of response for technology (24%).

What are the most signicant challenges to successfully executing your email marketing programmes? (Select all)

Overall, the data prove how strong the position of email is as the core channel around which other marketing activity

can be built.

The GDPR eect

The majority of marketers (56%) feel positive about the impact the GDPR is having on their operations, with just a

fth negative about the new regulations. There is a touch more negativity in B2C organisations (27%) than B2B rms

(21%);this may be due to the former handling changes to bigger databases.

2%

4%

7%

9%

16%

16%

17%

20%

21%

22%

25%

30%

40%

42%

0% 10% 20% 30% 40% 50%

None of the above

Outdated ESP technology

Choosing latest channels

rather than eective channels

Data degradation

Poor interdepartmental

communication

Data siloes

Lack of senior support

Lack of content

Outdated in-house technology

Inecient internal processes

Lack of strategy

Lack of data

Limited internal resource

Limited budget

MARKETER EMAIL TRACKER 2019

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

8

The GDPR came into force in May 2018. What impact have these new laws had on your current email marketing

programme?

Similarly, larger organisations of all types display less positive sentiment than their smaller counterparts. Just 39% of

very large enterprises (more than 1000 employees) are positive about the GDPR compared to 59% of SMEs (101-250

employees) and 56% of rms with a smaller workforce (less than 100 people) A possible explanation for this variation

of sentiments towards the new privacy laws might be due to dierences in the amount of data to manage. Indeed,

smaller organisations may have found it easier to be agile to the changes and have already started to see the benets.

Bigger businesses, on the other hand, have more wide-ranging factors, such as bigger teams, more databases and

sheer scale to consider. In many cases, they are still on their journey to full compliance, as we found in the ‘Data

privacy – An industry perspective’ report.

Marketers also said that email deliverability has generally improved in light of the new regulations. Over half (55%)

feel positive about the GDPR’s eect in this area, compared to 19% negative sentiment.

In terms of legal bases being used for email marketing, the largest proportion of organisations (46%) are using both

consent and legitimate interests (LI). A third use only consent and 21% use LI. B2C rms admit a greater reliance on

consent as a single legal ground: 36%, compared to 29% of B2B organisations. It’s a similar situation with LI, with 27%

in B2C relying solely on this defence compared to 15% in B2B. Very large organisations tend to opt for consent (46%)

whereas the group of smallest organisations are the most likely to choose a blend of consent and LI (61%).

Delving deeper into marketers’ attitudes, they feel they can now make their email campaigns more targeted and

relevant thanks to the need for better data under the GDPR — leading to improved open rates. From the negative

point of view, however, some have seen drastic reductions in the size of their email database.

Despite the generally positive attitude revealed by the research, organisations must remain aware that compliance is a

continual process. Despite initial changes made, it will be important to keep an eye on adjudications under the GDPR,

from the ICO and other EU regulators, which will make aspects of the new regulation clearer. In all cases, organisations

need to be sure that use of LI is a legal basis, which can be determined by a Legitimate Interest Assessment (see the

DMA’s ‘GDPR for marketers: The essentials’ guidance).

Unimportant Neutral Important

20% 24% 56%

0% 20% 40% 60% 80% 100%

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

9

MARKETER EMAIL TRACKER 2019

How do marketers rate their own email expertise? This year, there was an improvement in the level of condence

respondents displayed. Those professing good or advanced ability have risen from 30% to 40% since the previous

survey, while levels of intermediate and basic knowledge have fallen.

How would you rate your organisation’s overall level of competence in email marketing?

Nevertheless, the proportion feeling they have basic or no knowledge has climbed from 9% to nearly 24% since

2015, suggesting plenty aren’t prepared to rest on their laurels. Perceived complexity of the email environment may

be leading some people to rate themselves less adept with aspects of marketing technology, such as automation

through AI and machine learning. It’s quite hard to maintain a feeling of advanced competence amid constant

evolution.

Meanwhile, senior respondents are more condent in their competence, with 52% rating their businesses’ ability

advanced or good. This compares to 42% of juniors and 35% of mid-level respondents. Possibly, those at a senior level

feel condent because of their involvement in, and awareness of, the latest strategic trends and technologies. Mid-

level respondents are the most likely to have a wide range of implementation responsibilities, and this relative lack of

day-to-day focus on email marketing is reected in their condence levels.

Automation and segmentation

A new question this year about automation and segmentation reveals that almost a quarter of campaigns are not

segmented or automated. Small companies (less than 100 employees) are the least likely to automate campaigns

(26%) and most likely to do neither (31%).

In an era when consumers are expecting better targeting, and even personalisation, these gures highlight a gap in

the armoury of marketing teams, where adopting new systems could easily make email marketing more eective.

Organisations are more likely to segment (43%) than automate (33%).

Practices & understanding

2%

3%

1%

5%

7%

24%

25%

19%

47%

43%

44%

37%

27%

21%

20%

22%

17%

9%

10%

18%

0%

20%

40%

60%

80%

100%

2015 2016 2017 2018

None Basic Intermediate Good Advanced

MARKETER EMAIL TRACKER 2019

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

10

What percentage of your email campaigns are automated/segmented/neither?

Email Testing

When it comes to email testing, there is a pronounced increase in marketers’ belief in their own abilities. In our

previous study, 34% rated themselves advanced or intermediate; the latest research sees that combined gure

increase to almost half (48%). In fact, condence has grown steadily from 2015 when the same combined level of

response was 31%.

How would you rate your organisation’s overall level of competence in email testing?

33%

43%

24%

0%

10%

20%

30%

40%

50%

Automated Segmented Neither

17%

8%

15%

11%

5%

14%

19%

12%

47%

44%

33%

29%

25%

27%

25%

33%

6%

7%

9%

15%

0%

20%

40%

60%

80%

100%

2015 2016 2017 2018

Don't conduct testing No competence Basic

Intermediate Advanced

MARKETER EMAIL TRACKER 2019

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

11

Furthermore, senior respondents feel most condent about testing, with 51% answering advanced or intermediate

compared to 45% of mid-level and 38% of junior respondents. The latter were also most likely to rate their testing

ability as basic. Additionally, 26% of this junior group say they have no competence or their organisation doesn’t carry

out email testing.

Finally, large and medium-sized businesses show a greater amount of condence, with respondents claiming

advanced and intermediate ability outweighing those with basic or no competence. This could be the GDPR eect at

play, as organisations must pay more attention to their communications and make sure campaigns are optimised so

they are compliant, relevant and useful for the recipient.

In terms of frequency, there is a trend towards fewer marketers not testing at all, or testing less than a quarter of their

campaigns, than in previous years. However, the proportion testing more than three quarters has dropped from 19%

to 11% during the last 12 months, meaning the most likely outcome is that organisations test somewhere between a

quarter and three-quarters of campaigns. B2C organisations are testing more regularly than B2B.

Testing is a vital part of email marketing. It can inform simple tweaks such as subject line and call to action amends

to generate better open rates and response. In that sense, it’s encouraging to know marketers generally feel more

condent about their testing abilities, as is the trend towards more frequent testing.

How often does your organisation conduct email testing? (Select one)

40%

47%

38%

30%

24%

35%

14%

10%

17%

16%

19%

11%

0%

20%

40%

60%

80%

100%

2016 2017 2018

Under a quarter A quarter to half Half to three-quarters Over three-quarters

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

12

MARKETER EMAIL TRACKER 2019

Relevance and eectiveness

For marketers measuring the relevance and eectiveness of their email campaigns, click-throughs, open rates, and

conversion rates are the top three metrics of choice. Just over a quarter (76%) use click-through to gauge relevance,

while around two thirds (67%) use them to track eectiveness.

Unsubscribes (52%) and engagement (43%) are also scrutinised by marketers measuring relevance, while delivery

volumes are used to gauge eectiveness (35%).

However, it is also important for marketers to consider the indirect eects of email. As we learned from our consumer

research into email, 27% of respondents said that an email would prompt them to go to the company’s website and

12% would visit its physical store. A further 9% would check out the brand on social media and 5% would call the

organisation. These are all indirect actions that may need to be considered when deciphering attribution for a multi-

channel marketing programme.

ROI and lifetime value

This year’s research saw a marked increase in marketers’ belief in their organisations’ ability to calculate ROI. Whereas

condence in calculating value had steadily declined between 2012 and 2015 to a 50/50 split, almost two thirds

(62%) now think they are measuring — the highest-ever result for this question.

B2C marketers are particularly condent, with almost three quarters (71%) able to make the calculation, though of

course B2B organisations (48%) generally need longer lead times and may not have a clear line of sight between

initial email and ROI.

ROI from email marketing now stands at just over £42 for every pound spent; a rise of almost £10 since the previous

study. B2B organisations collectively report just under £36 ROI, but a lower proportion are measuring, compared to

B2C organisations we surveyed — which score an average return of nearly £48.

How much is the approximate return you get back for every pound spent on email marketing?

Measurement & value

£29.64

£31.01

£32.28

£42.24

£-

£10.00

£20.00

£30.00

£40.00

£50.00

2015 2016 2017 2018

MARKETER EMAIL TRACKER 2019

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

13

Further good news comes in the shape of the ability to calculate lifetime value. This also increased markedly, almost

doubling year-on-year to 41%. Again, this is likely down to preparation for the GDPR when subscriber lists were

scrutinised.

Lifetime value of each individual email address has also risen sharply by 33% year-on-year. An address is now believed

to be worth £37, on average, an encouraging sign that companies understand the value of email records and they are

starting to feel the benets of better data quality. Again, lifetime value was higher in B2C (£41) than B2B (£35).

How much is the approximate value for an average individual email address to your organisation?

Alongside the results of the previous section, marketers appear to be bullish about their ability. They are testing more,

have better condence about framing ROI, and also understanding the lifetime value of each customer in their email

database. This can only be good news for email as a marketing channel.

£28.56

£37.32

£-

£10.00

£20.00

£30.00

£40.00

2017 2018

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

14

MARKETER EMAIL TRACKER 2019

Frequency

A majority of marketers believe a rule for frequency of contact should be implemented at their organisations. Some

87% agree they would like to see this implemented, against 77% in the previous survey.

Do you think there should be a frequency of contact rule within your organisation?

Interestingly, however, rms are now sending more emails than prior to the new law’s implementation: a weekly

average of 24 emails is sent to people on their mailing list, compared to the 21 they declared in 2018. B2B companies

send 18 emails weekly, while B2C organisations distribute 24.

For their part, consumers have reported receiving almost half the number of emails (25 per week) compared to 2017,

when they estimated 45 per week hitting their inbox. Marketers, meanwhile, think the weekly total has risen slightly

from 21 to 24 emails, in very close alignment with consumers’ calculations. These gures demonstrate that marketers

might be overestimating the number of messages sent, and consumers are feeling less ‘spammed’. If an accurate

reection of the market, this means GDPR has again had a positive impact when it comes to email marketing.

Receiving & content

23%

13%

77%

87%

0%

20%

40%

60%

80%

100%

2017 2018

No Yes

MARKETER EMAIL TRACKER 2019

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

15

How many emails do you send on average each week to those on your mailing lists, including those sent

automatically? (Compared to the number consumers believe they receive from brands)

Relevance

However, relevance remains a concern. Only 55% of marketers think more than half of all the emails leaving their

organisation are relevant to the individual recipient. Our consumer insight also revealed that only around one in

seven people (14%) believe more than half the emails they get are of use to them. This means that, despite volume

reduction, relevance is still an issue for brands.

How many of the emails that your organisation sends do you believe to be relevant to individual customers?

(Compared the percentage consumers believe are ‘useful’)

21

45

24

25

0

10

20

30

40

50

Marketers Consumers

2017 2018

46%

86%

55%

14%

0%

20%

40%

60%

80%

100%

Marketers Consumers

Under half Over half

MARKETER EMAIL TRACKER 2019

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

16

Advance notice of sales (78%), non-promotional content (73%) and discounts/oers (70%) are deemed the most

eective email features to help marketers achieve their goals. For consumers, the most useful types of email content

are discounts/oers (75%), e-receipts (61%) and advance notice of new products/sales (58%).

Consumers are also far less interested in non-promotional content than marketers believe, with just 22% liking it

compared to the 73% of marketers who think it’s eective. The same is true of videos, pictures and GIFs (27% for

consumers vs. 66% for marketers). This may be down to consumers expecting this content as part and parcel of the

emails they receive from brands, but there is clearly a disconnection here that brands should consider. The key to

success remains oering tangible value and using content to oer relevance — whether it’s the format or quality of

the message.

What types of email message/content helps you to achieve your email campaign objectives? (Compared to

content consumers like to receive from brands)

78%

73%

70%

66%

65%

57%

47%

34%

58%

22%

75%

27%

41%

47%

40%

61%

0%

20%

40%

60%

80%

100%

Advance notice of

products/sales

Non-promotional

content

Discounts & oers Videos, picture

and GIFs

Post-purchase

communications

Competitions Access to other brand

benets

E- receipts

Consumers likeMarketers value

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

17

MARKETER EMAIL TRACKER 2019

Sign-ups

Customer loyalty, trust and advance notice of new products and sales are deemed the top three most eective

ways of prompting email subscription, according to marketers. E-receipts, though popular with consumers, are not

considered eective, along with features such as the opportunity to join a loyalty scheme, video/image content and

competitions.

Considering your email marketing programmes, which are most eective in encouraging consumers to sign-up

for your emails? (Compared to what consumers say normally persuades them to give their email address to a

brand)

Unsubscribes

Moving towards the closure of the relationship between the brand and its customer, almost half of the marketing

respondents (47%) immediately action unsubscribes and no further emails are sent to the individual, with 39% saying

only service emails are then sent. Meanwhile, unsubscribe actions are linked to a preference centre by 18% and a

survey by 11%. It is really promising to see that none of the businesses surveyed keep sending emails to customers

that had unsubscribed – a further conrmation that GDPR has improved marketing practices.

Some 40% of consumers agree that they shouldn’t receive non-service emails after unsubscribing — though 21%

claim opting out makes no dierence as they still get messages. It’s possible this could decrease as brands build in

further compliance in the wake of the GDPR, reassuring consumers about the emails they will receive.

Sign-ups & unsubscribes

84%

76%

74%

71%

70%

65%

61%

58%

55%

54%

48%

35%

46%

31%

17%

5%

51%

27%

9%

22%

3%

40%

12%

30%

0%

20%

40%

60%

80%

100%

Regular

customer

Trust in

the brand

Advance

notice of

products/sales

Non-

promotional

content

Discounts

& oers

Like the

brand

Post-

purchase

communications

Competitions

Videos,

picture and

GIFs

Join loyalty

programme

Access to other

brand benets

E- receipts

Consumers likeMarketers value

MARKETER EMAIL TRACKER 2019

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

18

When a customer unsubscribes from your organisation’s emails, what happens next? (Compared to what

consumers typically expect to happen)

59%

48%

25%

40%

23%

17%

21%

0%

20%

40%

60%

80%

No more contact Still receive service emails Taken to preference centre/survey Emails will continue later

/makes no dierence

Consumers Marketers

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

19

MARKETER EMAIL TRACKER 2019

Marketers are generally positive about the changes in key performance metrics for email over the past 12 months.

Just over three quarters (76%) report an increase in open rates; 75% say click-throughs are higher; 67% indicate

delivery rates have increased and 66% say the same about conversion. Slightly more than half (51%) say ROI has risen.

All of these performance areas have increased signicantly compared to the previous survey.

Conversely, opt-out rates have decreased according to 41%, and 55% say spam complaints are also down — further

evidence of the GDPR eect.

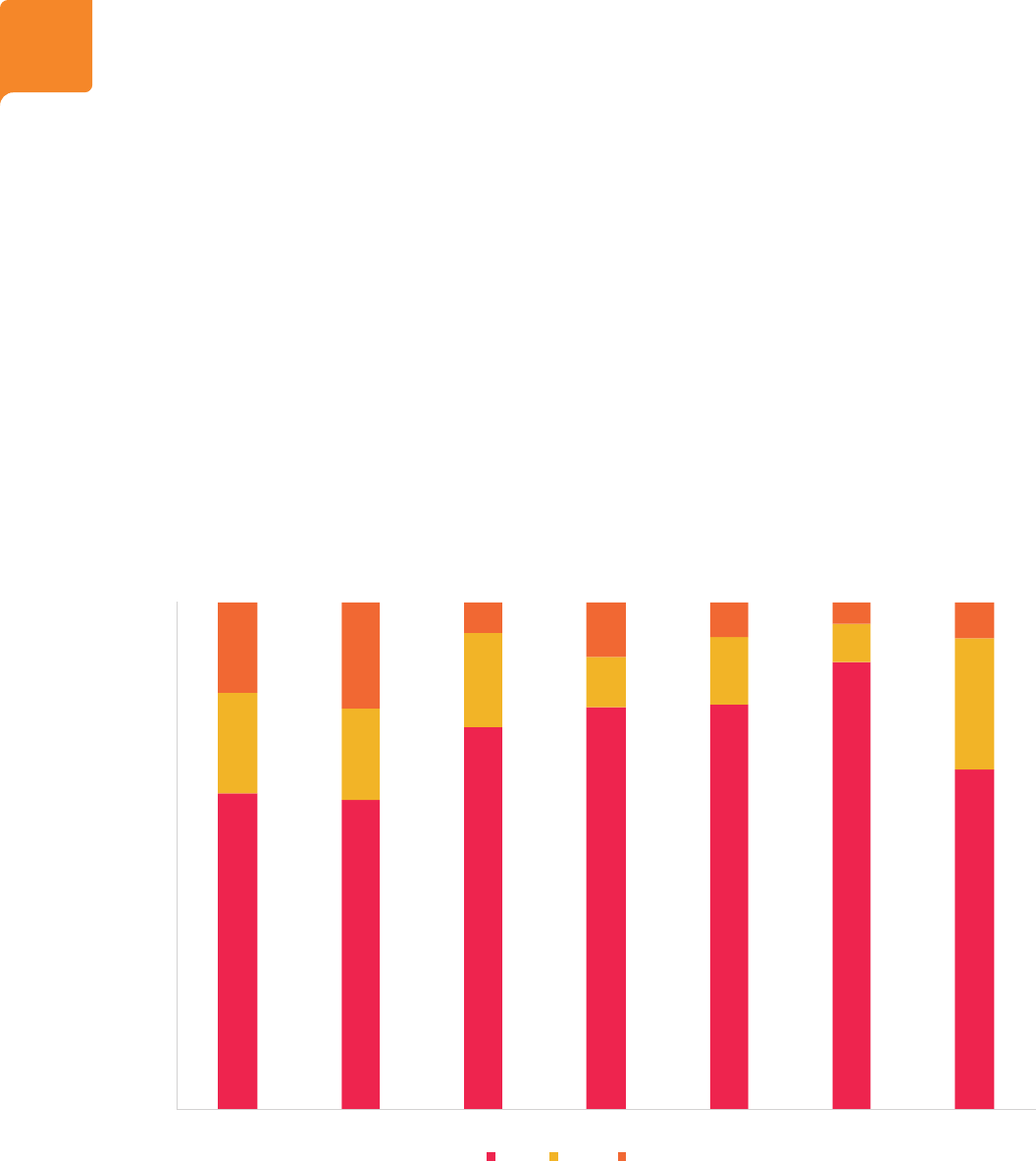

Furthermore, marketers expect performance to improve in most areas over the next year. Some 82% expect a rise

in open rates, 77% click-throughs and 74% delivery. ROI will continue to increase according to 59%, while opt-outs

should drop, say 46%, along with spam complaints (54%).

Respondents expect the proportion of marketing budgets for email to climb to almost 17%, compared to 11% the

last time they were asked. A total of 33% expect their organisation to commit more than 21% of the overall marketing

budget to email in the next 12 months. Moreover, almost two thirds (63%) expect email marketing budgets to

increase, a year-on-year rise from 46%.

What percentage of your marketing budget is spent on email? (Not including sta costs)

It will be interesting to see if this budgetary boost results in a rise in ROI — or if costs are simply increasing; 57% say

email marketing costs are due to increase, up from 48% last year.

Future expectations

63%

61%

74%

81%

82%

88%

67%

20%

18%

18%

10%

14%

8%

26%

18%

21%

6%

11%

7%

4%

7%

0%

20%

40%

60%

80%

100%

2012 2013 2014 2015 2016 2017 2018

21-40%0-20% More than 40%

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

20

MARKETER EMAIL TRACKER 2019

The ‘Marketer email tracker 2019’ is part of an annual study undertaken by the DMA in partnership with dotdigital and

the Research hub of the DMA’s Email council.

The research was conducted in January 2019 via an online survey of 197 respondents ¬¬— nationally representative

of UK marketers.

The data was collected and collated by Qualtrics, then analysed by the DMA Insight department. The report was

written and designed by the DMA Insight department and in-house design team.

The survey consisted of a maximum of 30 questions. These questions were reviewed by the DMA, dotdigital and the

Email council’s research hub to ensure relevance to the current state of the email industry.

Respondents represented a range of department types, sectors and career levels. Of those answering the relevant

question, 29% were B2B, 29% in B2C, and 42% were involved in both B2B and B2C marketing. The reported career

levels were 21% senior, 52% mid and 27% junior.

Where averages are presented, these were calculated by multiplying the number of respondents by the

corresponding value (or the middle value where this is a range), summing these, and then dividing by the total

number of respondents.

If you have any questions about the methodology used in the report, you can contact the DMA’s research team via

email: [email protected]g.uk.

Methodology

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

21

MARKETER EMAIL TRACKER 2019

The DMA represents the UK’s data and marketing industry, and a DMA membership is a recognised badge of

accreditation.

Membership will help you grow your business alongside our network of more than 1,000 UK companies. You will

access a suite of services, including complimentary legal advice and lobbying, industry leading research and insight,

and IDM training courses.

Our members connect at regular events that inspire creativity, innovation, and responsible marketing, while

upholding a code that puts the customer at the heart of all we do.

We are proud to lead the data and marketing industry towards new standards for customer centric business practice,

creativity, and innovation.

Published by The Direct Marketing Association (UK) Ltd Copyright © Direct Marketing Association.

All rights reserved.

www.dma.org.uk

About the DMA

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

22

MARKETER EMAIL TRACKER 2019

Formerly dotmailer, dotdigital is a leader in customer engagement technology.

dotdigital’s Engagement Cloud is the platform of choice for businesses seeking to engage customers across all

touchpoints. The platform’s features empower 4,000+ brands across 150 countries to acquire, convert, and retain

customers.

Users can connect customer data, surface powerful insights, and automate intelligent messages across email, SMS,

social, and more. dotdigital is a global company with over 350 employees, serving companies of all sizes and in all

verticals for over 20 years.

About dotdigital

COPYRIGHT: THE DIRECT MARKETING ASSOCIATION (UK) LTD 2019

23

MARKETER EMAIL TRACKER 2019

The Marketer Email Tracker 2019 is published by The Direct Marketing Association (UK) Ltd Copyright © Direct

Marketing Association. All rights reserved. No part of this publication may be reproduced, copied or transmitted in

any form or by any means, or stored in a retrieval system of any nature, without the prior permission of the DMA (UK)

Ltd except as permitted by the provisions of the Copyright, Designs and Patents Act 1988 and related legislation.

Application for permission to reproduce all or part of the Copyright material shall be made to the DMA (UK) Ltd, DMA

House, 70 Margaret Street, London, W1W 8SS.

Although the greatest care has been taken in the preparation and compilation of the Marketer email tracker 2019, no

liability or responsibility of any kind (to extent permitted by law), including responsibility for negligence is accepted

by the DMA, its servants or agents. All information gathered is believed correct at February 2019. All corrections

should be sent to the DMA for future editions.

Copyright and disclaimer