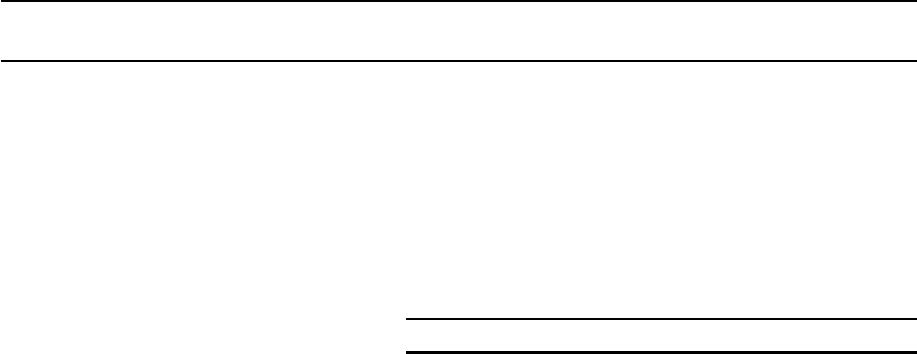

1999 2000 2001 2002 2003

Net Margin

12%

10%

8%

6%

4%

2%

10.0%

11.1%

9.2%

4.4%

7.4%

6.8%

15.8%

0.5

pts.

83.4%

3.0

pts.

80.6%

80.0%

14.2%

3.6

pts.

12.5%

4.2%

5.6%

4.2%

0.9

pts.

1.7%

3.1%

2.6%

3.5%

Operating expenses

Operating income

Operating margin

Net income

Net margin

Net income per share – basic

Net income per share – diluted

Stockholders’ equity

Revenue passengers carried

Revenue passenger miles {RPMs} (000s)

Available seat miles {ASMs} (000s)

Passenger load factor

Passenger revenue yield per RPM

Operating revenue yield per ASM

Operating expenses per ASM

Size of fleet at yearend

(2.5)%

Number of Employees at yearend

Stockholders’ equity per common share outstanding

Return on average stockholders’ equity

CONSOLIDATED HIGHLIGHTS

Operating revenues

7.5%

CHANGE

(DOLLARS IN MILLIONS, EXCEPT PER SHARE AMOUNTS)

$5,454

$483

8.1%

$442

7.4%

$.56

$.54

$5,052

9.3%

$6.40

65,673,945

47,943,066

71,790,425

66.8%

11.97¢

8.27¢

7.60¢

388

32,847

$5,937

2003

$5,105

$417

7.6%

$241

4.4%

$.31

$.30

$4,422

5.7%

$5.69

63,045,988

45,391,903

68,886,546

65.9%

11.77¢

8.0 2 ¢

7.41¢

375

33,705

$5,522

2002

Southwest Airlines Co. is the nation’s low-fare, high Customer Satisfaction airline. We primarily serve short- and medium-haul

city pairs, providing single-class air transportation which targets business and leisure travelers. The Company, incorporated

in Texas, commenced Customer Service on June 18, 1971, with three Boeing 737 aircraft serving three Texas cities – Dallas,

Houston, and San Antonio. At yearend 2003, Southwest operated 388 Boeing 737 aircraft and provided service to 59 airports in

30 states throughout the United States. Southwest has one of the lowest operating cost structures in the domestic airline

industry and consistently offers the lowest and simplest fares. Southwest also has one of the best overall Customer Service

records. LUV is our stock exchange symbol, selected to represent our home at Dallas Love Field, as well as the theme of our

Employee and Customer relationships.

1999

2000

2001

2002

$.80

$.70

$.60

$.50

$.40

$.30

$.59

$.79*

$.63

$.30

2003

$.54

Net Income Per Share, Diluted

Excludes cumulative effect of change

in accounting principle of $.03.

*

1999

2000 2001

2002

Return On Stockholders’ Equity

20%

15%

10%

5%

18.1%

19.9%

13.7%

5.7%

2003

9.3%

FREEDOM

Americans didn’t just invent the airplane, we invented the airline as well. Back in 1914, a

few bold travelers flew on the Airboat Line between Tampa and St. Petersburg. Today,

Southwest Airlines gives Americans the freedom to fly from coast to coast, including

Tampa/St. Petersburg. In February 2003, Southwest was named the Most Admired

Airline for the second straight year in

FORTUNE magazine. In June, we announced

that our current and future f leet of Boeing 737-700s will be outfitted with fuel-saving,

performance-enhancing Blended Winglets. In August, the Bureau of Transportation

Statistics announced that Southwest carried more domestic originating passengers

in May than any other airline, marking the first time a low-fare airline has topped those

monthly rankings. In October 2003, we announced service, beginning in May 2004, to

Philadelphia, the city that freedom built. As we look back on our 31st consecutive profitable

year, we are once again proud to say, “You are now free to move about the country.™”

2

Southwest Airlines Co. 2003 Annual Report

To Our Shareholders:

Just as promised in our 2002 Annual Report, in the year 2003

Southwest Airlines kept “MOVING AHEAD.”

While the airline industry, as a whole, reported more than

$5 billion (excluding special items) in 2003 losses:

1. Southwest produced its 31st consecutive year of profitability, an

airline industry record that has also generated unprecedented

airline industry job security and exceptional Profitsharing for our

marvelous Employees, as well as exceptional investment returns

for our Shareholders, including Employee-Shareholders.

2. Southwest’s annual profits increased from $198 million in 2002,

excluding special items ($241 million, including special items), to

$298 million, excluding special items ($442 million including special

items, such as industrywide government war relief grants).

3. Southwest expanded its fleet by a net of 13 new 737-700s and

increased our Available Seat Miles by 4.2 percent.

4. Southwest continued to equip our new aircraft deliveries, and to

refurbish our existing fleet, with our fresh and most attractive

Canyon Blue aircraft livery; all leather interiors in Canyon Blue

and Saddle Tan; new design seats affording superb personal

comfort; and aesthetic Blended Winglets, which improve aircraft

performance by extending range, saving fuel, and reducing

engine maintenance costs and takeoff noise.

5. Southwest retained its leadership in Customer Satisfaction, again

receiving the fewest Customer complaints per 100,000 Customers

carried, as reflected in DOT statistics compiled from reports

furnished to DOT by the largest domestic air carriers.

6. Southwest was selected: In

FORTUNE magazine, as one of

our nation’s Most Admired Companies • In Business Ethics

magazine’s listing of the “100 Best Corporate Citizens” in America

•InHISPANIC magazine’s listing of the “2003 Hispanic

Corporate 100” • The “Best Low Cost Airline” at the 2003

Official Airline Guide Airline of the Year awards • By AirTransport

World magazine as its “Airline of the Year” • By Inside Flyer

magazine as having the Best Customer Service, Best Bonus

Promotion, and Best Award Redemption of any frequent flyer

program (Southwest’s Rapid Rewards) • As featured airline in

the A&E Network series

AIRLINE •ForGlobal Finance

magazine’s “Experts’ List of the World’s Most Socially

Responsible Companies.”

We intend to keep “MOVING FUR

THER AHEAD” in

2004, expanding our fleet by a net of 29 new 737-700s and our

Available Seat Miles by almost eight percent, while utilizing

our proportionally unsurpassed financial strength ($1.87 billion

in cash and an unsecured revolving credit line of $575 million at

yearend 2003), continued low costs per Available Seat Mile, leading

Customer Satisfaction record, and superb Employee esprit de

corps to prevail over the 2004 uncertainties with respect to: fuel

price levels (we are over 80 percent hedged for the year with prices

capped at approximately $24 per barrel of crude oil); the rate of

U.S. economic recovery and attendant expansion of Customer

demand; a potential substantial expansion in capacity by competitive

air carriers; and any exogenous events adversely affecting the

domestic airline industry.

In May of 2004, we will commence air service to Philadelphia,

the largest metropolitan area in the U.S. not now served, directly or

indirectly, by Southwest. We have also announced that in light of

Southwest’s strong cash position, investment-grade balance sheet,

and desire to maximize Employee-Shareholder and non-Employee-

Shareholder value that Southwest intends to use the very significant

present and anticipated proceeds from the exercise of our

outstanding stock options for the repurchase, from time to time,

of up to $300 million of our common stock in the open market.

For more than three decades, the wisdom, farsightedness,

goodwill, and camaraderie of our People have produced a remarkable

airline providing remarkable psychic and financial rewards for all of our

Employees. We thank them for their understanding and their goodness,

which have produced greatness for Southwest and for them.

January 20, 2004

Most sincerely,

3

Southwest Airlines Co. 2003 Annual Report

Herbert D. Kelleher,

Chairman of the Board

Herb was named to Secretary of

Homeland Security Tom Ridge’s

advisory panel in 2003.

James F. Parker,

Vice Chairman & CEO

Jim was named one of two “Business

People of the Year” by

Dallas Business

Journal

; the other was Colleen Barrett.

Colleen C. Barrett,

President & COO

Colleen was named one of the

“50 Most Powerful Women in Business” by

FORTUNE magazine two years running.

4

Southwest Airlines Co. 2003 Annual Report

SPREADING

OUR WINGS

In June 2003, Southwest Airlines announced that our current and future fleet of Boeing 737-700s

will be outfitted with fuel-saving, performance-enhancing Blended Winglets. We unveiled

the fleet’s first jet with winglets in ceremonies in Austin, Dallas, and Houston — representing

our original “Texas Triangle” destinations in 1971. These sleek, colorful appendages on

the wings of our handsome Canyon Blue jets give the fleet a distinctive, technologically

advanced look and feel.

5

Southwest Airlines Co. 2003 Annual Report

2003 proved to be another perilous year for the airline industry.

With the Iraq war, severe acute respiratory syndrome (SARS), a

weak economy, high energy costs, and terrorism-related concerns,

the major airlines continue to report billions in losses and struggle

for survival. Since September 11, 2001, major airlines have cut

capacity, slashed jobs, and scrambled to reduce their costs to

avoid bankruptcy and compete in an industry that is forever

changed. Two major airlines have already filed bankruptcy, and

other smaller carriers have ceased operations entirely.

As a result of the dire financial condition of our major

airline competitors, exacerbated by the war in Iraq, the government

provided substantial cash payments to the airline industry

under the Emergency Wartime Supplemental Appropriations

Act. The government also waived the requirement that security

fees be collected on airline tickets issued from June 1 to

September 30, 2003.

Despite these difficult challenges, we reported our 31st

consecutive annual profit in 2003 because of our low operating

costs and superb People. Southwest’s long profitability record is

unmatched in the airline industry, and we are also the only major

airline to post a profit in every quarter following the September 11

terrorist attacks. While the airline industry, as a whole, reported

losses for the third straight year in 2003, our profits were up

significantly from 2002, even excluding the favorable impact from

the $271 million federal grant.

Because we were financially prepared, we were able to

persevere through these difficult times and build a stronger

Southwest. Instead of significant capacity reductions, Southwest

invested in our future. We took care of our People, providing pay

rate increases and Profitsharing rather than furloughs and wage

concessions. We added airplanes, expanded airports, and invested

in facilities, equipment, and automation to enhance our Customers’

experience and prepare us for future growth.

Although we cannot predict what external, uncontrollable

events could impact us in 2004, it seems that the worst could finally

be behind us. The downward revenue trends prior to and shortly

following the Iraq war have improved, albeit gradually. Although

the industry has planned for significant capacity increases in 2004,

we are confident in our future and believe we are uniquely

positioned for growth.

Low Costs

Historically, Southwest has enjoyed a significant cost advantage

compared to the “legacy” carriers. That advantage has been somewhat

diminished as those carriers have reduced their labor costs and

improved their work rules through either voluntary concessions or

the bankruptcy process. In addition, there are now a number of

new, rapidly growing carriers with costs roughly comparable to

those of Southwest Airlines.

The Employees of Southwest have always understood that we

are profitable, growing, and successful because of our competitive

cost advantage. Although our costs remain low, we are not satisfied

with the inflation we began to experience in our cost structure

during second half 2003 and are aggressively implementing various

measures to improve our productivity. Effective December 15, 2003,

Southwest no longer pays a commission on flights booked by

traditional travel agencies, which will reduce operating costs by

approximately $40 million annually. In February 2004, we will

consolidate our reservations operations from nine into six

Reservations Centers. We will incur restructuring charges of an

estimated $20 million in first quarter 2004 and expect ongoing cost

savings to exceed that amount each year. As a result of these and

many other measures, cost pressures should ease in second half

2004. Our Employees are motivated and innovative, and we are

confident that our People will continue to find and embrace faster

and better ways of running our business.

While a lot of factors contribute to Southwest’s historic low

cost advantage, the primary driver is the productivity and Southwest

Spirit of our People. We are devoted to the low-fare, point-to-point

market niche and have a highly efficient route structure. This

market focus allows us to operate a single aircraft type, the Boeing 737.

Commonality of fleet significantly simplifies our scheduling,

operations, and maintenance and, therefore, lowers cost. We

consistently run an ontime operation, with few mishandled bags

8.96¢

9.43¢

8.51¢

9.5¢

9.0¢

8.5¢

8.0¢

7.5¢

7.0¢

1999 2000 2001 2002

Operating Revenues Per Available Seat Mile

8.02¢

2003

8.27¢

1999 2000 2001 2002

Operating Expenses Per Available Seat Mile

7.48¢

7.73¢

7.54¢

7.41¢

2003

7.60¢

7.8¢

7.6¢

7.4¢

7.2¢

7.0¢

70

60

50

40

30

1999 2000 2001 2002

52,855

59,910

65,295

68,887

2003

71,790

Available Seat Miles

(in millions)

6

Southwest Airlines Co. 2003 Annual Report

CHICAGO

MIDWAY

BALTIMORE/

WASHINGTON

INTERNATIONAL

HOUSTON

HOBBY

Recent renovations to our Chicago Midway, Baltimore/Washington International, and

Houston Hobby airports have resulted in stunning new environments for our colorful

Southwest counters and gate areas. Not only are these downtown airports more convenient

than their big airport counterparts, they are now calm, comfortable, and traveler-friendly.

Southwest offers our Customers a welcome oasis from a workaday world, coast-to-coast and

border-to-border.

7

Southwest Airlines Co. 2003 Annual Report

and cancellations. Our fleet is young and well-maintained, which

also allows us to avoid excessive mechanical delays. Where available,

we favor alternative airports in major U.S. cities, avoiding congestion

in competitors’ hubs, which keeps our planes off the ground and in

the air where they are making money.

We have a very strong low-fare brand, which draws Customers

to us directly and results in very low distribution costs. In 2003,

approximately 54 percent of passenger revenues were derived

through the Company’s web site at southwest.com and only 16 percent

were booked through travel agents. Going forward, our distribution

costs will be even lower due to the consolidation of our reservations

operations and the elimination of traditional travel agency

commissions.

Southwest also has a successful hedging program, which saved

us $171 million in jet fuel costs during 2003. We are also well

protected in 2004 and 2005 with over 80 and 70 percent, respectively,

of our anticipated fuel requirements hedged with prices capped at

approximately $24 per barrel of crude oil.

Low Fares

Low fares has been our philosophy since day one — every seat,

every flight, every day. Since 1971, we have fought to keep our costs

low so that we could make flying affordable instead of a luxury for

a few. As we have grown and introduced Southwest fares to the

new communities we serve, more of our Customers understand

they can always rely on us for a low fare.

Although every carrier has been a “low-fare carrier” since

September 11, we are the only airline that has offered low fares

profitably and consistently for 32+ years. Our Employees remain

dedicated to spreading low fares and their Legendary Customer

Service across America. Bringing low fares to Americans is not just

our business, it’s our passion.

Legendary Customer Service

Our Employees are widely recognized for their Southwest

Spirit and caring hearts. Because we have earned a reputation as

a great place to work, we attract and hire the best applicants.

According to the April 2003 issue of

FORTUNE, Southwest

is an employer of choice among college students. Once we hire

someone, we train, develop, and provide the support they

need to succeed. We trust our Employees, and we empower

them to effectively make decisions to perform their jobs in a

challenging industry.

Our Employees genuinely care about our Company, our

Customers, and the communities we serve. They have had to

endure constant change and stress since September 11, 2001, while

adapting to complicated security measures and procedures. We have

deployed new technologies at our airports and dramatically changed

the way we operate our business. Despite these difficult operating

conditions, our People never lost their compassion, caring hearts, or

desire to deliver the best Customer Service in the industry. Southwest

had the best annual Customer complaint record of all carriers for

the 13th straight year based on Customer complaints reported in the

U.S. Department of Transportation’s (D.O.T.) Air Travel Consumer

Report. Southwest also had the best systemwide ontime performance

record of any Major U.S. airline for the full year 2003 as reported

in the D.O.T.’s Air Travel Consumer Report. (A Major airline is

defined as having annual operating revenue of $1 billion or more.)

During 2003,

The Wall Street Journal reported Southwest ranked

first among airlines for the highest Customer Service Satisfaction,

according to a survey by the American Customer Satisfaction Index.

In 2003, Southwest was named “Best Domestic Airline of the Year”

by

Travel Weekly and “Airline of the Year” by Air Transport World

magazine. Southwest is also consistently recognized by FORTUNE as

one of America’s Most Admired Companies and America’s most

admired airline.

Our Employees are also wonderful stewards in the communities

we serve. Southwest is committed to “doing the right thing,” which

is why giving back to the communities we serve and positively

contributing to the environment is simply the way we do business. As

a result of our caring and altruistic Employees, Southwest was included

in

Global Finance magazine’s January 2004 “Experts’ List of the

World’s Most Socially Responsible Companies.” Southwest was also

listed again in

Business Ethics magazine’s “100 Best Corporate

Citizens” and again recognized for having the best reputation among

U.S. airlines in a 2003 study conducted by Harris Interactive Inc. and

the Reputation Institute. In addition, Southwest was the first U.S.

airline to be awarded the “Corporate Conscience Award for

Community Positive Impact” in October 2003.

Frequent Flights

Southwest offers lots of flights to the cities we serve and

continued to increase flights in 2003. We have approximately

2,800 daily frequencies to 59 airports. Our high frequencies and

expansive route system offer our Customers convenience and

reliability with lots of options to get where they want to go, when

they want to get there.

As a result of the combination of low fares, high frequencies, and

our friendly Customer Service, we dominate the majority of the markets

we serve. We consistently rank first in market share in approximately

90 percent of our top 100 city-pair markets and, in the aggregate, hold

around 65 percent of the total market share in those markets.

Although our revenues have been soft since September 11,

2001, our market share has increased in many of our markets as

most of our major competitors have been forced to shrink

8

Southwest Airlines Co. 2003 Annual Report

9

Southwest Airlines Co. 2003 Annual Report

their operations. For example, as of second quarter 2003 (the

latest information available), we have a 48 percent market share

in Chicago Midway; 44 percent in Baltimore; 36 percent in LasVegas;

and 36 percent in Phoenix. We also have a 74 percent intra-Texas

market share; 71 percent intra-California; and 42 percent intra-Florida.

Rapid Rewards

In addition to our low fares and convenient flight schedule, our

frequent flyers are generously rewarded with free trips through our

Rapid Rewards program. Rapid Rewards allows Customers to

receive a roundtrip award valid for travel anywhere Southwest flies

by simply flying eight roundtrips or earning 16 credits (a one-way

ticket equals one credit) within 12 consecutive months. There are

no seat restrictions and very few blackout dates for awards travel;

therefore, Members can use their award to fly virtually anytime to

any Southwest destination. Rapid Rewards awards are also fully

transferable.

Inside Flyer magazine recognized the generosity and

simplicity of our Rapid Rewards program with its Freddie Awards

for Best Customer Service, Best Award Redemption, and Best

Bonus Promotion among all frequent flyer programs. Rapid

Rewards Members can also receive Rapid Rewards credits when

doing business with our Preferred Partners (Alamo, American

Express, Budget, Diners Club, Dollar, Hertz, Earthlink, Nextel,

Hilton, Hyatt, Marriott, La Quinta, and Choice brand hotels) as

well as through the use of the Southwest Airlines Rapid Rewards

Bank One

®

Visa credit card.

Strong Financials

Our Chairman and Co-founder, Herb Kelleher, has always

taught us to manage our Company in good times so that we are

ready for bad times. As a result of this philosophy, we have the

strongest financial position in the industry, and we were prepared

for the devastating aftermath of September 11, 2001. We operate

in an industry that is cyclical, energy intensive, labor intensive,

and capital intensive. Our operating costs are largely fixed,

and our operations are subject to federal oversight, weather

conditions, and natural disasters. Our industry is also highly

competitive. Consequently, we must always be financially prepared

for the worst.

Since September 11, 2001, we have taken the necessary steps

to protect and even strengthen our balance sheet and liquidity. At

the end of 2003, we had $1.87 billion in cash on hand, a fully

available bank revolving credit facility of $575 million, unmortgaged

assets of over $5 billion, and debt to total capital of less than

40 percent, including leases as debt. We are the only airline with an

investment-grade credit rating. We have adequate access

to the capital markets and have strengthened our financial

position during the post-September 11 period; therefore, we

are well poised to take advantage of growth opportunities or

face further adversities.

In consideration of our strong financial and cash flow

position and our desire to maximize Employee-Shareholder and

non-Employee-Shareholder value, we recently announced that

we intend to use a portion of the very significant present and

anticipated proceeds from the exercise of Employee stock options

toward the repurchase of up to $300 million of our common

stock from time to time in the open market.

Growth Opportunities

Steady, conservative growth during the recessionary environment

since the terrorist attacks has enabled Southwest to restore our

operations, strengthen our balance sheet, and maintain our

profitability. We grew our annual capacity by just over four percent

in 2003 and over five percent in 2002. Since September 11, 2001, we

have added 30 net aircraft. The airline industry, on the other hand,

has reduced domestic capacity by 15 to 20 percent. As a result of our

decision to cautiously grow rather than reduce capacity, Southwest

topped the monthly domestic originating passenger rankings for the

first time in May 2003. Also Southwest is the largest carrier based

on scheduled domestic departures.

With the exception of Norfolk, which was planned prior to the

terrorist attacks, there have been no new cities since September 11,

2001. Instead, we added new city-pair routings and increased existing

PHILADELPHIA

FREEDOM

Net Income (in millions)

Excludes cumulative effect of change

in accounting principle of $22 million

1999 2000 2001 2002

$600

$500

$400

$300

$200

$100

$474

$625*

*

$511

$241

2003

$442

Average Daily Departures

1999 2000 2001 2002

2,800

2,600

2,400

2,200

2,000

2,550

2,700

2,800

2,800

2003

2,800

1.0

.75

.50

.25

Customer Service

(Complaints per 100,000 Customers boarded)

For the year ending December 31, 2003

Excludes American Eagle Airlines

LUV

.14

ALK

.52

U

.90

NWAC

.95

DAL

.78

CAL

.95

AMR

.88

UAL

.83

AWA

.84

*

*

In October 2003, Southwest announced service to Philadelphia, the city that freedom built,

beginning in May 2004. Philadelphia was once the home of local legend and Southwest

Chairman Herb Kelleher (center left), whose triumphant return to his boyhood home gives all

Philadelphians the Freedom to Fly. Philadelphia is also the home of the original Ronald

McDonald House (lower left), the primary charity of Southwest Airlines.

9

Southwest Airlines Co. 2003 Annual Report

their operations. For example, as of second quarter 2003 (the

latest information available), we have a 48 percent market share

in Chicago Midway; 44 percent in Baltimore; 36 percent in LasVegas;

and 36 percent in Phoenix. We also have a 74 percent intra-Texas

market share; 71 percent intra-California; and 42 percent intra-Florida.

Rapid Rewards

In addition to our low fares and convenient flight schedule, our

frequent flyers are generously rewarded with free trips through our

Rapid Rewards program. Rapid Rewards allows Customers to

receive a roundtrip award valid for travel anywhere Southwest flies

by simply flying eight roundtrips or earning 16 credits (a one-way

ticket equals one credit) within 12 consecutive months. There are

no seat restrictions and very few blackout dates for awards travel;

therefore, Members can use their award to fly virtually anytime to

any Southwest destination. Rapid Rewards awards are also fully

transferable.

Inside Flyer magazine recognized the generosity and

simplicity of our Rapid Rewards program with its Freddie Awards

for Best Customer Service, Best Award Redemption, and Best

Bonus Promotion among all frequent flyer programs. Rapid

Rewards Members can also receive Rapid Rewards credits when

doing business with our Preferred Partners (Alamo, American

Express, Budget, Diners Club, Dollar, Hertz, Earthlink, Nextel,

Hilton, Hyatt, Marriott, La Quinta, and Choice brand hotels) as

well as through the use of the Southwest Airlines Rapid Rewards

Bank One

®

Visa credit card.

Strong Financials

Our Chairman and Co-founder, Herb Kelleher, has always

taught us to manage our Company in good times so that we are

ready for bad times. As a result of this philosophy, we have the

strongest financial position in the industry, and we were prepared

for the devastating aftermath of September 11, 2001. We operate

in an industry that is cyclical, energy intensive, labor intensive,

and capital intensive. Our operating costs are largely fixed,

and our operations are subject to federal oversight, weather

conditions, and natural disasters. Our industry is also highly

competitive. Consequently, we must always be financially prepared

for the worst.

Since September 11, 2001, we have taken the necessary steps

to protect and even strengthen our balance sheet and liquidity. At

the end of 2003, we had $1.87 billion in cash on hand, a fully

available bank revolving credit facility of $575 million, unmortgaged

assets of over $5 billion, and debt to total capital of less than

40 percent, including leases as debt. We are the only airline with an

investment-grade credit rating. We have adequate access

to the capital markets and have strengthened our financial

position during the post-September 11 period; therefore, we

are well poised to take advantage of growth opportunities or

face further adversities.

In consideration of our strong financial and cash flow

position and our desire to maximize Employee-Shareholder and

non-Employee-Shareholder value, we recently announced that

we intend to use a portion of the very significant present and

anticipated proceeds from the exercise of Employee stock options

toward the repurchase of up to $300 million of our common

stock from time to time in the open market.

Growth Opportunities

Steady, conservative growth during the recessionary environment

since the terrorist attacks has enabled Southwest to restore our

operations, strengthen our balance sheet, and maintain our

profitability. We grew our annual capacity by just over four percent

in 2003 and over five percent in 2002. Since September 11, 2001, we

have added 30 net aircraft. The airline industry, on the other hand,

has reduced domestic capacity by 15 to 20 percent. As a result of our

decision to cautiously grow rather than reduce capacity, Southwest

topped the monthly domestic originating passenger rankings for the

first time in May 2003. Also Southwest is the largest carrier based

on scheduled domestic departures.

With the exception of Norfolk, which was planned prior to the

terrorist attacks, there have been no new cities since September 11,

2001. Instead, we added new city-pair routings and increased existing

Net Income (in millions)

Excludes cumulative effect of change

in accounting principle of $22 million

1999 2000 2001 2002

$600

$500

$400

$300

$200

$100

$474

$625*

*

$511

$241

2003

$442

Average Daily Departures

1999 2000 2001 2002

2,800

2,600

2,400

2,200

2,000

2,550

2,700

2,800

2,800

2003

2,800

1.0

.75

.50

.25

Customer Service

(Complaints per 100,000 Customers boarded)

For the year ending December 31, 2003

Excludes American Eagle Airlines

LUV

.14

ALK

.52

U

.90

NWAC

.95

DAL

.78

CAL

.95

AMR

.88

UAL

.83

AWA

.84

*

*

FREEDOM

10

Southwest Airlines Co. 2003 Annual Report

FIGHTERS

The People of Southwest Airlines are our most valuable asset. It is their friendliness, Customer

caring, and relentless resourcefulness that have helped make Southwest one of the world’s most

successful airlines. We are not a Company of planes; we are a Company of People — People

willing to fight for your right to fly.

11

Southwest Airlines Co. 2003 Annual Report

service in many markets, particularly in Baltimore/Washington

and Chicago Midway. We celebrated our tenth anniversary in

Baltimore/Washington in 2003, now our third largest market in

terms of daily departures. We have 161 daily nonstop flights from

Baltimore/Washington, including coast-to-coast service to Los

Angeles, San Jose, and San Diego. Chicago Midway is now our fifth

largest city in terms of daily departures with 134.

In addition to recently expanding airport facilities at

Baltimore/Washington and Chicago Midway, we have major expansion

projects at Fort Lauderdale, Houston Hobby, Las Vegas, Long Island/Islip,

Oakland, Orange County, Orlando, Phoenix, and Tampa Bay.

With the worst of times hopefully behind us, we are prepared

for accelerated growth. As a result of significant penetration by

Southwest and other low-fare carriers and the ability for Customers

to easily shop for low fares on the Internet, more Americans than

ever realize that they do not have to pay high fares. Given the weak

financial condition of the industry, we are uniquely positioned to

meet the increased demand for low fares. After all, profitably offering

low fares is what we do best!

As a result of our improved longterm outlook and numerous

opportunities to grow, we have stepped up our growth rate and

currently expect to increase capacity almost eight percent in 2004

and over ten percent in 2005. In total, we have just under 400 Boeing

737 aircraft on either firm order, option, or purchase rights with The

Boeing Company from 2004 through 2012, which results in an

annualized growth rate during this period of roughly eight percent.

We are well positioned to grow our traditional low-fare,

point-to-point market niche and are excited to bring the Freedom

to Fly to Philadelphia in May 2004. From Philadelphia, we will

initially begin service to Chicago Midway, Las Vegas, Orlando,

Phoenix, Providence, and Tampa Bay.

Airport Automation

Our People have done a wonderful job of responding to the

multitude of complex security changes since the September 11,

2001, terrorist attacks. In fact, our Chairman was recently appointed

to the Private Sector Senior Advisory Committee, a subcommittee

of the Homeland Security Advisory Council. Although these new

requirements initially presented challenges and longer checkin

times and lines for our Customers, the checkin times are back to

normal for our Customers and, in many ways, the airport experience

has been improved.

To facilitate the many new security requirements, we have

streamlined our airport operations with automation. We implemented

computer-generated baggage tags to electronically capture bags

checked by Customers. We then introduced computer-generated

Automated Boarding Passes from multiple points at the airport. This

allows us to identify the Customer by name for boarding purposes and

allows the Customer a more convenient checkin at airports through

standing in fewer lines. We also implemented self-service boarding

pass kiosks, or RAPID CHECK-IN, to allow our Customers plenty of

options to acquire boarding passes and alleviate checkin lines at ticket

and gate counters. As a result of this technology, we recently installed

gate reconciliation devices at our airports to speed the boarding

process. In 2004, Customers will be able to check bags using our

RAPID CHECK-IN kiosks and will be able to obtain their

transfer boarding passes at the time of checkin. We will also

offer Customer checkin and boarding passes on southwest.com.

All-Jet Fleet

At the end of 2003, Southwest operated an all-coach,

all-Boeing 737 fleet. All of our future orders, options, and purchase

rights with The Boeing Company for 2004 through 2012 are for

B737-700s. The average age of our young fleet is less than ten years.

As the -700 model is our future, we are in the process of retiring our

-200 fleet over the next two years with 18 and five retirements

scheduled in 2004 and 2005, respectively.

Since 2001, we have been renewing the interior and exterior of

our fleet, including leather-covered seats. Beginning in October

2004, all of our -700s are expected to be delivered with Blended

Winglets, and we are in the process of retrofitting our existing -700s

with winglets through early 2005. The addition of these wing

enhancements will extend the range of the aircraft, save fuel, lower

engine maintenance costs, and reduce takeoff noise.

1999 2000 2001 2002

11:20

11:15

11:10

11:05

11:00

Aircraft Utilization (hours and minutes per day)

11:10

11:18

11:10

11:12

2003

11:09

Fleet Size (at yearend)

1999 2000 2001 2002

400

300

200

100

312

344

355

375

2003

388

Boeing 737-700 Firm Orders and Options

Firm Orders

47 28

34

22 25 6

–

–––

–

–

6 12 9 25

2020 177

177

217

397

128

52

47 34 54 51

Options

Purchase Rights

Type

Total

Total

2009-

2012

2004 2005 2006 2007 2008

12

Southwest Airlines Co. 2003 Annual Report

Southwest System Map

•

Service to Philadelphia starts May 9, 2004

Southwest’s Market Share

(Southwest’s top 100 city-pair markets based on passengers carried)

Southwest’s Capacity By Region

Southwest

65%

Other Carriers

35%

California

18%

Remaining West

26%

Midwest

15%

East

29%

Southwest’s Top Ten Airports — Daily Departures

Heartland

12%

(Santa Fe Area)

(Miami Area)

Oakland

Los Angeles (LAX)

San Diego

Phoenix

Tucson

Albuquerque

Amarillo

Lubbock

Midland/

Odessa

El Paso

Dallas

(Love Field)

Austin

Houston

(Hobby & Intercontinental)

Corpus

Christi

Harlingen/South Padre Island

New Orleans

Birmingham

Nashville

Oklahoma City

Tulsa

Omaha

Little Rock

St. Louis

Chicago

(Midway)

San Antonio

Sacramento

Burbank

Reno/Tahoe

Salt Lake City

Cleveland

Providence

Long Island/Islip

Norfolk

Manchester

Detroit

Columbus

Kansas City

Louisville

San Jose

Baltimore/

(BWI)

Washington

Portland

Boise

Seattle/

Tacoma

Spokane

Orange County

Jacksonville

Ft. Lauderdale

Jackson

Ontario

Raleigh-Durham

Hartford/Springfield

Albany

Philadelphia

West Palm Beach

Orlando

Tampa Bay

Buffalo/

Niagara Falls

Indianapolis

Las Vegas

(D.C. Area)

(Southern Virginia)

(Boston Area)

(Boston Area)

(Palm Springs Area)

(San Francisco Area)

(San Francisco Area)

200

175

150

125

100

75

50

83

San Diego

86

Nashville

114

Los Angeles

122

Oakland

143

Houston

Hobby

183

Las Vegas

185

Phoenix

161

Baltimore/

Washington

134

Chicago

Midway

130

Dallas Love

13

Southwest Airlines Co. 2003 Annual Report

COMMON STOCK PRICE RANGES AND DIVIDENDS

Southwest’s common stock is listed on the New York Stock Exchange and is traded under the symbol LUV. The high and low sales prices of the common

stock on the Composite Tape and the quarterly dividends per share were:

PERIOD DIVIDENDS HIGH LOW

2003

1st Quarter $.0045 $15.33 $11.72

2nd Quarter .0045 17.70 14.09

3rd Quarter .0045 18.99 15.86

4th Quarter .0045 19.69 15.30

2002

1st Quarter $.0045 $22.00 $17.17

2nd Quarter .0045 19.35 14.85

3rd Quarter .0045 16.08 10.90

4th Quarter .0045 16.70 11.23

QUARTERLY FINANCIAL DATA (UNAUDITED)

THREE MONTHS ENDED

(In millions, except per share amounts) MARCH 31 JUNE 30 SEPTEMBER 30 DECEMBER 31

2003

Operating revenues $1,351 $1,515 $1,553 $1,517

Operating income 46 140 185 111

Income before income taxes 39 397 171 101

Net income 24 246 106 66

Net income per share, basic .03 .32 .14 .08

Net income per share, diluted .03 .30 .13 .08

2002

Operating revenues $1,257 $1,473 $1,391 $1,401

Operating income 49 189 91 88

Income before income taxes 35 169 124 64

Net income 21 102 75 42

Net income per share, basic .03 .13 .10 .05

Net income per share, diluted .03 .13 .09 .05

1999 2000 2001 2002

Operating Revenue

(in millions)

$4,736

$5,650

$5,555

$5,522

2003

$5,937

$6,000

$5,000

$4,000

$3,000

$2,000

$1,000

1999

2000

2001

2002

Passenger Load Factor

69.0%

70.5%

68.1%

65.9%

2003

66.8%

75%

70%

65%

60%

55%

50%

50

40

30

20

10

1999 2000 2001 2002

36,479

42,215

44,494

45,392

2003

47,943

Revenue Passenger Miles

(in millions)

14

Southwest Airlines Co. 2003 Annual Report

SELECTED CONSOLIDATED FINANCIAL DATA

(Dollars in millions, except per share amounts)

2003

(4)

2002

(3)

2001

(3)

2000

Operating revenues:

Passenger

(2)

$ 5,741 $ 5,341 $ 5,379 $ 5,468

Freight 94 85 91 111

Other

(2)

102 96 85 71

Total operating revenues 5,937 5,522 5,555 5,650

Operating expenses 5,454 5,105 4,924 4,628

Operating income 483 417 631 1,022

Other expenses (income), net (225) 24 (197) 4

Income before income taxes 708 393 828 1,018

Provision for income taxes 266 152 317 392

Net income

(1)

$442 $241 $511 $626

Net income per share, basic

(1)

$.56 $.31 $.67 $.84

Net income per share, diluted

(1)

$.54 $.30 $.63 $.79

Cash dividends per common share $.0180 $.0180 $.0180 $.0148

Total assets $ 9,878 $ 8,954 $ 8,997 $ 6,670

Long-term debt less current maturities $ 1,332 $ 1,553 $ 1,327 $ 761

Stockholders’ equity $ 5,052 $ 4,422 $ 4,014 $ 3,451

CONSOLIDATED FINANCIAL RATIOS

Return on average total assets 4.7% 2.7% 6.5% 10.1%

Return on average stockholders’ equity 9.3% 5.7% 13.7% 19.9%

CONSOLIDATED OPERATING STATISTICS

Revenue passengers carried 65,673,945 63,045,988 64,446,773 63,678,261

RPMs (000s) 47,943,066 45,391,903 44,493,916 42,215,162

ASMs (000s) 71,790,425 68,886,546 65,295,290 59,909,965

Passenger load factor 66.8% 65.9% 68.1% 70.5%

Average length of passenger haul 730 720 690 663

Trips flown 949,882 947,331 940,426 903,754

Average passenger fare

(2)

$87.42 $84.72 $83.46 $85.87

Passenger revenue yield per RPM

(2)

11.97¢ 11.77¢ 12.09¢ 12.95¢

Operating revenue yield per ASM 8.27¢ 8.02¢ 8.51¢ 9.43¢

Operating expenses per ASM 7.60¢ 7.41¢ 7.54¢ 7.73¢

Operating expenses per ASM, excluding fuel 6.44¢ 6.30¢ 6.36¢ 6.38¢

Fuel cost per gallon (average) 72.3¢ 68.0¢ 70.9¢ 78.7¢

Number of Employees at yearend 32,847 33,705 31,580 29,274

Size of fleet at yearend

(5)

388 375 355 344

(1)

Before cumulative effect of change in accounting principle

(2)

Includes effect of reclassification of revenue reported in 1999 through 1995 related to sale of flight segment

credits from Other to Passenger due to the accounting change implemented in 2000

(3)

Certain figures in 2001 and 2002 include special items related to the September 11, 2001, terrorist attacks and Stabilization Act grant

(4) Certain figures in 2003 include special items related to the Wartime Act grant

(5) Includes leased aircraft

(6)

Includes certain estimates for Morris Air Corporation, acquired by the Company in 1994

TEN-YEAR SUMMARY

15

Southwest Airlines Co. 2003 Annual Report

1999 1998 1997 1996 1995 1994

$ 4,563 $ 4,010 $ 3,670 $ 3,285 $ 2,768 $ 2,498

103 99 95 80 66 54

70 55 52 41 39 40

4,736 4,164 3,817 3,406 2,873 2,592

3,954 3,480 3,293 3,055 2,559 2,275

782 684 524 351 314 317

8 (21) 7 10 8 18

774 705 517 341 306 299

299 272 199 134 123 120

$ 475 $ 433 $ 218 $ 207 $ 183 $ 179

$.63 $.58 $.43 $.28 $.25 $.25

$.59 $.55 $.41 $.27 $.24 $.24

$.0143 $.0126 $.0098 $.0087 $.0079 $.0079

$ 5,654 $ 4,716 $ 4,246 $ 3,723 $ 3,256 $ 2,823

$ 872 $ 623 $ 628 $ 650 $ 661 $ 583

$ 2,836 $ 2,398 $ 2,009 $ 1,648 $ 1,427 $ 1,239

9.2% 9.7% 8.0% 5.9% 6.0% 6.6%

18.1% 19.7% 17.4% 13.5% 13.7% 15.6%

57,500, 213 52,586,400 50,399 ,960 49,621,504 44,785,573 42,742,602

(6)

36,479,322 31,419,110 28,355,169 27,083,483 23,327,804 21,611,266

52,855,467 47,543,515 44,487,496 40,727,495 36,180,001 32,123,974

69.0% 66.1% 63.7% 66.5% 64.5% 67.3%

634 597 563 546 521 506

846,823 806,822 786,288 748,634 685,524 624,476

$79.35 $76.26 $72.81 $66.20 $61.80 $58.44

12.51¢ 12.76¢ 12.94¢ 12.13¢ 11.86¢ 11.56¢

8.96¢ 8.76¢ 8.58¢ 8.36¢ 7.94¢ 8.07¢

7.48¢ 7.32¢ 7.40¢ 7.50¢ 7.07¢ 7.08¢

6.55¢ 6.50¢ 6.29¢ 6.31¢ 6.06¢ 6.09¢

52.7¢ 45.7¢ 62.5¢ 65.5¢ 55.2¢ 53.9¢

27,653 25,844 23,974 22,944 19,933 16,818

312 280 261 243 224 199

16

Southwest Airlines Co. 2003 Annual Report

TRANSFER AGENT AND REGISTRAR

Registered shareholder inquiries regarding

stock transfers, address changes, lost stock

certificates, dividend payments, or account

consolidation should be directed to:

Continental Stock Transfer & Trust Company

17 Battery Place

New York, New York 10004

(212) 509-4000

STOCK EXCHANGE LISTING

New York Stock Exchange

Ticker Symbol: LUV

INDEPENDENT AUDITORS

Ernst & Young LLP

Dallas, Texas

GENERAL OFFICES

P.O. Box 36611

Dallas, Texas 75235-1611

ANNUAL MEETING

The Annual Meeting of Shareholders of

Southwest Airlines Co. will be held at 10:00 a.m.

on May 19, 2004, at the Southwest Airlines

Corporate Headquarters, 2702 Love Field Drive,

Dallas, Texas.

FINANCIAL INFORMATION

A copy of the Company’s Annual Report

on Form 10-K as filed with the U.S. Securities

and Exchange Commission (SEC) and other

financial information can be found on Southwest’s

web site (southwest.com) or may be obtained

without charge by writing or calling:

Southwest Airlines Co.

Investor Relations

P.O. Box 36611

Dallas, Texas 75235-1611

Telephone (214) 792-4908

DIRECTORS

COLLEEN C. BARRETT

President and Chief Operating Officer

Southwest Airlines Co., Dallas, Texas

LOUIS CALDERA

President of The University of New Mexico

Albuquerque, New Mexico; Audit and

Nominating and Corporate Governance

Committees

C. WEBB CROCKETT

Attorney, Fennemore Craig,

Attorneys at Law, Phoenix, Arizona;

Compensation and Nominating and Corporate

Governance Committees

WILLIAM H. CUNNINGHAM, Ph.D.

James L. Bayless Professor of Marketing

University of Texas School of Business

Former Chancellor of The University of Texas

System, Austin, Texas; Audit (Chairman) and

Nominating and Corporate Governance

Committees

WILLIAM P. HOBBY

Chairman of the Board, Hobby

Communications, L.L.C.; Former Lieutenant

Governor of Texas; Houston, Texas; Audit,

Compensation (Chairman), and Nominating and

Corporate Governance Committees

TRAVIS C. JOHNSON

Attorney at Law, El Paso, Texas; Audit,

Executive, and Nominating and Corporate

Governance Committees

HERBERT D. KELLEHER

Chairman of the Board, Southwest Airlines Co.,

Dallas, Texas; Executive Committee

ROLLIN W. KING

Retired, Dallas, Texas; Audit, Executive, and

Nominating and Corporate Governance

Committees

NANCY LOEFFLER

Longtime advocate of volunteerism

San Antonio, Texas

JOHN T. MONTFORD

President, External Affairs, SBC Southwest,

a division of SBC Communications, Inc.,

San Antonio, Texas; Audit and Nominating and

Corporate Governance Committees

JUNE M. MORRIS

Founder and former Chief Executive Officer

of Morris Air Corporation, Salt Lake City, Utah;

Audit, Compensation, and Nominating and

Corporate Governance Committees

JAMES F. PARKER

Vice Chairman and Chief Executive Officer of

Southwest Airlines Co., Dallas, Texas

OFFICERS

JAMES F. PARKER*

Vice Chairman and Chief Executive Officer

COLLEEN C. BARRETT*

President and Chief Operating Officer

Corporate Secretary

DONNA D. CONOVER*

Executive Vice President — Customer Service

GARY C. KELLY*

Executive Vice President and

Chief Financial Officer

JAMES C. WIMBERLY*

Executive Vice President and

Chief of Operations

JOYCE C. ROGGE*

Senior Vice President — Marketing

DEBORAH ACKERMAN

Vice President — General Counsel

BEVERLY CARMICHAEL

Vice President — People Department

GREGORY N. CRUM

Vice President — Flight Operations

GINGER C. HARDAGE

Vice President — Corporate Communications

ROBERT E. JORDAN

Vice President — Technology

CAMILLE T. KEITH

Vice President — Special Marketing

DARYL KRAUSE

Vice President — Provisioning

KEVIN M. KRONE

Vice President — Interactive Marketing

PETE MCGLADE

Vice President — Schedule Planning

BOB MONTGOMERY

Vice President — Properties and Facilities

ROB MYRBEN

Vice President — Fuel

RON RICKS*

Vice President — Governmental Affairs

DAVE RIDLEY*

Vice President — Ground Operations

JAMES A. RUPPEL

Vice President — Customer Relations

and Rapid Rewards

RAY SEARS

Vice President — Purchasing

JIM SOKOL

Vice President — Maintenance and Engineering

KEITH L. TAYLOR

Vice President — Revenue Management

ELLEN TORBERT

Vice President — Reservations

MICHAEL G. VAN DE VEN

Vice President — Financial Planning

and Analysis

TAMMYE WALKER-JONES

Vice President — Inflight

GREG WELLS

Vice President — Safety, Security,

and Flight Dispatch

STEVEN P. WHALEY

Controller

LAURA H. WRIGHT

Vice President — Finance and Treasurer

*Member of Executive Planning Committee

CORPORATE DATA

“One of the interesting results of this financial crisis is that some airlines have found ways to operate far more efficiently – and cheaply.

The ideas aren’t really new – many are things Southwest has been doing for years.”

– USA Today, January 9, 2003

“The top ten won the business world’s regard…by refocusing attention where it counts the most: on customers and employees.”

— FORTUNE magazine, in its annual listing of “America’s Most Admired Companies,” in which Southwest finished second, February 19, 2003

Rather than starting their own, “If Delta and United really want to invest in a discount airline, there’s a better way: Buy some Southwest

stock.”

– Washington Post columnist Steven Pearlstein, in an article titled “Airline Recovery Plans Fly in the Face of Reason,” March 25, 2003

“Unlike other carriers, Southwest has lured plenty of Customers without partnering with travel Web sites Expedia, Travelocity, and Orbitz.

‘Their Customers seek them out, which is tremendous,’ said Paul Berliner, an industry consultant. ‘I mean, my goodness, that’s what you

dream about.’”

– San Jose Mercury News, May 8, 2003

“Many carriers, new and old, are trying to emulate Southwest’s low-cost, no-frills formula. And there has been a nearly perfect inverse

correlation between declining traffic for old-line carriers and increasing traffic at the low-cost carriers of which Southwest is the progenitor.”

– The Wall Street Journal, July 24, 2003

“Let’s see…Southwest pays Employees well and makes it clear through actions rather than ‘managementspeak’ that it appreciates and trusts

its workers. And the company succeeds where others fail. What a shock.”

– The San Francisco Chronicle, August 13, 2003

“It’s becoming as predictable as death and taxes: Southwest Airlines reported its 50th-consecutive quarterly profit.” – “Today in the Sky,”

USA Today, October 22, 2003

“Southwest Airlines may only be the nation’s sixth largest airline, but it doesn’t act like No. 6. In many ways, it may be No. 1. The grandfather

of the low-cost airline has set the pace and provided the model for the latest crop of low-fare carriers. …Southwest’s financial superlatives

in these days of airline bankruptcies are of chest-pounding stuff.”

– Airline Financial News, December 4, 2003

SOUTHWEST AIRLINES CO.

P.O. Box 36611

Dallas, Texas 75235-1611

214.792.4000

1.800.I.FLY.SWA

southwest.com

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

For the Fiscal Year Ended December 31, 2003 or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission File No. 1-7259

SOUTHWEST AIRLINES CO.

(Exact name of registrant as specified in its charter)

TEXAS 74-1563240

(State or other jurisdiction of (I.R.S. employer

incorporation or organization) identification no.)

P.O. Box 36611

Dallas, Texas 75235-1611

(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code: (214) 792-4000

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

Name of Each Exchange

Title of Each Class on Which Registered

Common Stock ($1.00 par value) New York Stock Exchange, Inc.

Common Share Purchase Rights New York Stock Exchange, Inc.

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was

required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein,

and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of the Securities

Exchange Act of 1934). Yes [X] No [ ]

The aggregate market value of the Common Stock held by non-affiliates of the registrant was approximately

$13,309,000,000, computed by reference to the closing sale price of the stock on the New York Stock Exchange on June

30, 2003, the last trading day of the registrant’s most recently completed second fiscal quarter.

Number of shares of Common Stock outstanding as of the close of business on December 31, 2003: 789,390,678 shares

DOCUMENTS INCORPORATED BY REFERENCE

Proxy Statement for Annual Meeting of

Shareholders, May 19, 2004: PART III

PART I

Item 1. Business

Description of Business

Southwest Airlines Co. (“Southwest”) is a major domestic airline that provides predominantly shorthaul,

high-frequency, point-to-point, low-fare service. Southwest was incorporated in Texas in 1967 and

commenced Customer Service on June 18, 1971 with three Boeing 737 aircraft serving three Texas cities -

Dallas, Houston, and San Antonio.

At year-end 2003, Southwest operated 388 Boeing 737 aircraft and provided service to 59 airports in

58 cities in 30 states throughout the United States. Southwest Airlines topped the monthly domestic

passenger traffic rankings for the first time in May 2003. Based on monthly data from May through August

2003 (the latest available data), Southwest Airlines is the largest carrier in the United States based on

originating domestic passengers boarded and scheduled domestic departures. The Company recently

announced that it intends to begin service to Philadelphia in May 2004.

One of Southwest’s competitive strengths is its low operating costs. Southwest has the lowest costs,

adjusted for stage length, on a per mile basis, of all of the major airlines. Among the factors that contribute

to its low cost structure are a single aircraft type, an efficient, high-utilization, point-to-point route structure,

and hardworking, innovative, and highly productive Employees.

The business of the Company is somewhat seasonal. Quarterly operating income and, to a lesser

extent, revenues tend to be lower in the first quarter (January 1 - March 31) and fourth quarter (October 1 -

December 31) of most years.

Southwest’s filings with the Securities and Exchange Commission (“SEC”), including its annual

report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those

reports are accessible free of charge at www.southwest.com.

Fuel

The cost of fuel is an item having significant impact on the Company's operating results. The

Company's average cost of jet fuel, net of hedging gains, over the past five years was as follows:

Year

Cost

(Millions)

Average Cost

per Gallon

Percent of

Operating Expenses

1999 $492 $.53 12.5%

2000 $804 $.79 17.4%

2001 $771 $.71 15.6%

2002 $762 $.68 14.9%

2003 $830 $.72 15.2%

From October 1, 2003 through December 31, 2003, the average cost per gallon was $.74. See

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” for a discussion

of Southwest’s fuel hedging activities.

Regulation

Economic. The Dallas Love Field section of the International Air Transportation Competition Act of

1979, as amended in 1997 (commonly known as the “Wright Amendment”), as it affects Southwest's

scheduled service, provides that no common carrier may provide scheduled passenger air transportation for

compensation between Love Field and one or more points outside Texas, except that an air carrier may

transport individuals by air on a flight between Love Field and one or more points within the states of

Alabama, Arkansas, Kansas, Louisiana, Mississippi, New Mexico, Oklahoma, and Texas if (a) "such air

carrier does not offer or provide any through service or ticketing with another air carrier" and (b) "such air

carrier does not offer for sale transportation to or from, and the flight or aircraft does not serve, any point

which is outside any such states." The Wright Amendment does not restrict flights operated with aircraft

having 56 or fewer passenger seats. The Wright Amendment does not restrict Southwest's intrastate Texas

flights or its air service from points other than Love Field.

The Department of Transportation (“DOT”) has significant regulatory jurisdiction over passenger

airlines. Unless exempted, no air carrier may furnish air transportation over any route without a DOT

certificate of public convenience and necessity, which does not confer either exclusive or proprietary rights.

The Company's certificates are unlimited in duration and permit the Company to operate among any points

within the United States, its territories and possessions, except as limited by the Wright Amendment, as do

the certificates of all other U.S. carriers. DOT may revoke such certificates, in whole or in part, for

intentional failure to comply with certain provisions of the U.S. Transportation Code, or any order or

regulation issued thereunder or any term of such certificate; provided that, with respect to revocation, the

certificate holder has first been advised of the alleged violation and fails to comply after being given a

reasonable time to do so.

DOT prescribes uniform disclosure standards regarding terms and conditions of carriage and

prescribes that terms incorporated into the Contract of Carriage by reference are not binding upon passengers

unless notice is given in accordance with its regulations.

Safety. The Company and its third-party maintenance providers are subject to the jurisdiction of the

Federal Aviation Administration (“FAA”) with respect to its aircraft maintenance and operations, including

equipment, ground facilities, dispatch, communications, flight training personnel, and other matters affecting

air safety. To ensure compliance with its regulations, the FAA requires airlines to obtain operating,

airworthiness, and other certificates, which are subject to suspension or revocation for cause. The Company

has obtained such certificates. The FAA, acting through its own powers or through the appropriate U. S.

Attorney, also has the power to bring proceedings for the imposition and collection of fines for violation of

the Federal Air Regulations.

The Company is subject to various other federal, state, and local laws and regulations relating to

occupational safety and health, including Occupational Safety and Health Administration (OSHA) and Food

and Drug Administration (FDA) regulations.

Security. On November 19, 2001, President Bush signed into law the Aviation and Transportation

Security Act (“Security Act”). The Security Act generally provides for enhanced aviation security measures.

The Security Act established a new Transportation Security Administration (“TSA”), which has recently

been moved to the new Department of Homeland Security. The TSA assumed the aviation security functions

previously residing in the FAA and assumed passenger screening contracts at U.S. airports on February 17,

2002. The TSA now provides for the screening of all passengers and property, which is performed by

federal employees. Beginning February 1, 2002, a $2.50 per enplanement security fee is imposed on

passengers (maximum of $5.00 per one-way trip). This fee was suspended by Congress from June 1 through

September 30, 2003. Pursuant to authority granted to the TSA to impose additional fees on air carriers if

necessary to cover additional federal aviation security costs, the TSA has imposed an annual Security

Infrastructure Fee, which approximated $23 million for Southwest in 2002 and $18 million in 2003. This fee

was also suspended by Congress from June 1 through September 30, 2003. Like the FAA, the TSA may

impose and collect fines for violations of its regulations.

Enhanced security measures have had, and will continue to have, a significant impact on the airport

experience for passengers. While these security requirements have not impacted aircraft utilization, they have

impacted our business. The Company has invested significantly in facilities, equipment, and technology to

process Customers efficiently and restore the airport experience. The Company has implemented its

Automated Boarding Passes and RAPID CHECK-IN self service kiosks in its 59 airports to reduce the

number of lines in which a Customer must wait. During 2003, the Company also installed gate readers at all

of its airports to improve the boarding reconciliation process. In 2004, Customers will be able to check

baggage using RAPID CHECK-IN kiosks. Southwest also plans to introduce internet checkin and transfer

boarding passes at the time of checkin.

Environmental. Certain airports, including San Diego and Orange County, have established airport

restrictions to limit noise, including restrictions on aircraft types to be used, and limits on the number of

hourly or daily operations or the time of such operations. In some instances, these restrictions have caused

curtailments in service or increases in operating costs and such restrictions could limit the ability of

Southwest to expand its operations at the affected airports. Local authorities at other airports may consider

adopting similar noise regulations, but such regulations are subject to the provisions of the Airport Noise and

Capacity Act of 1990 and regulations promulgated thereunder.

Operations at John Wayne Airport, Orange County, California, are governed by the Airport's Phase 2

Commercial Airline Access Plan and Regulation (the "Plan"). Pursuant to the Plan, each airline is allocated

total annual seat capacity to be operated at the airport, subject to renewal/reallocation on an annual basis.

Service at this airport may be adjusted annually to meet these requirements.

The Company is subject to various other federal, state, and local laws and regulations relating to the

protection of the environment, including the discharge or disposal of materials such as chemicals, hazardous

waste, and aircraft deicing fluid. Regulatory developments pertaining to such things as control of engine

exhaust emissions from ground support equipment and prevention of leaks from underground aircraft fueling

systems could increase operating costs in the airline industry. The Company does not believe, however, that

such environmental regulatory developments will have a material impact on the Company’s capital

expenditures or otherwise adversely effect its operations, operating costs, or competitive position.

Additionally, in conjunction with airport authorities, other airlines, and state and local environmental

regulatory agencies, the Company is undertaking voluntary investigation or remediation of soil or

groundwater contamination at several airport sites. The Company does not believe that any environmental

liability associated with such sites will have a material adverse effect on the Company’s operations, costs, or

profitability.

Customer Service Commitment. From time to time, the airline transportation industry has been faced

with possible legislation dealing with certain Customer service practices. As a compromise with Congress,

the industry, working with the Air Transport Association, has responded by adopting and filing with the

DOT written plans disclosing how it would commit to improving performance. Southwest Airlines

formalized its dedication to Customer Satisfaction by adopting its Customer Service Commitment, a

comprehensive plan which embodies the Mission Statement of Southwest Airlines: dedication to the highest

quality of Customer Service delivered with a sense of warmth, friendliness, individual pride, and Company

Spirit. The Customer Service Commitment can be reviewed by clicking on “About SWA” at

www.southwest.com. Congress is expected to monitor the effects of the industry’s plans, and there can be no

assurance that legislation will not be proposed in the future to regulate airline Customer service practices.

Marketing and Competition

Southwest focuses principally on point-to-point, rather than hub-and-spoke, service in markets with

frequent, conveniently timed flights and low fares. At year-end, Southwest served 337 nonstop city pairs.

Southwest’s average aircraft trip stage length in 2003 was 558 miles with an average duration of

approximately 1.5 hours. Examples of markets offering frequent daily flights are: Dallas to Houston, 35

weekday roundtrips; Phoenix to Las Vegas, 19 weekday roundtrips; and Los Angeles International to

Oakland, 22 weekday roundtrips. Southwest complements these high-frequency shorthaul routes with

longhaul nonstop service between markets such as Baltimore and Los Angeles, Phoenix and Tampa Bay,

Seattle and Nashville, and Houston and Oakland.

Southwest's point-to-point route system, as compared to hub-and-spoke, provides for more direct

nonstop routings for Customers and, therefore, minimizes connections, delays, and total trip time. Southwest

focuses on nonstop, not connecting, traffic. As a result, approximately 79 percent of the Company's

Customers fly nonstop. In addition, Southwest serves many conveniently located satellite or downtown

airports such as Dallas Love Field, Houston Hobby, Chicago Midway, Baltimore-Washington International,

Burbank, Manchester, Oakland, San Jose, Providence, Ft. Lauderdale/Hollywood and Long Island Islip

airports, which are typically less congested than other airlines' hub airports and enhance the Company's

ability to sustain high Employee productivity and reliable ontime performance. This operating strategy also

permits the Company to achieve high asset utilization. Aircraft are scheduled to minimize the amount of

time the aircraft are at the gate, currently approximately 25 minutes, thereby reducing the number of aircraft

and gate facilities that would otherwise be required. The Company operates only one aircraft type, the

Boeing 737, which simplifies scheduling, maintenance, flight operations, and training activities. Southwest

does not interline or offer joint fares with other airlines, nor have any commuter feeder relationships.

Southwest employs a relatively simple fare structure, featuring low, unrestricted, unlimited, everyday

coach fares, as well as even lower fares available on a restricted basis. The Company’s highest oneway

unrestricted walkup fare offered is $299 for any flight. Even lower walkup fares are available on

Southwest’s short and medium haul flights.

Southwest was the first major airline to introduce a Ticketless travel option, eliminating the need to

print and then process a paper ticket altogether, and the first to offer Ticketless travel through the Company’s

home page on the Internet, www.southwest.com. For the year ended December 31, 2003, more than 85

percent of Southwest's Customers chose the Ticketless travel option and approximately 54 percent of

Southwest’s passenger revenues came through its Internet site, which has become a vital part of the

Company’s distribution strategy. As part of Southwest’s cost reduction measures and due to the success of

its website, the Company has announced it will no longer pay commissions to travel agents for sales on or

after December 15, 2003.

The airline industry is highly competitive as to fares, frequent flyer benefits, routes, and service, and

some carriers competing with the Company have larger fleets and wider name recognition. Certain major

United States airlines have established marketing or codesharing alliances with each other, including

Northwest Airlines/Continental Airlines/Delta Air Lines; American Airlines/Alaska Airlines; and United

Airlines/USAirways.

After the terrorist acts of September 11, 2001, and in the face of weak demand for air service, most

major carriers (not including Southwest) significantly reduced service, grounded aircraft, and furloughed

employees. UAL, the parent of United Airlines, and US Airways sought relief from financial obligations in

bankruptcy and other, smaller carriers have ceased operation entirely. America West Airlines, USAirways,

and others received federal loan guarantees authorized by federal law and additional airlines may do so in the

future. Many carriers renegotiated collective bargaining agreements and vendor agreements, resulting in a

reduction in their costs. More recently, many major carriers have announced plans for capacity increases in

2004; likewise, smaller low cost carriers have accelerated their growth plans. While Southwest’s share of the

domestic market has continued to increase, it is not currently possible to assess the ultimate impact of all of

these events on airline competition.

The Company is also subject to varying degrees of competition from surface transportation in its

shorthaul markets, particularly the private automobile. In shorthaul air services that compete with surface

transportation, price is a competitive factor, but frequency and convenience of scheduling, facilities,

transportation safety and security procedures, and Customer Service are also of great importance to many

passengers.

Insurance

The Company carries insurance of types customary in the airline industry and at amounts deemed

adequate to protect the Company and its property and to comply both with federal regulations and certain of

the Company’s credit and lease agreements. The policies principally provide coverage for public and

passenger liability, property damage, cargo and baggage liability, loss or damage to aircraft, engines, and

spare parts, and workers’ compensation.

Following the terrorist attacks, commercial aviation insurers significantly increased the premiums

and reduced the amount of war-risk coverage available to commercial carriers. The federal government

stepped in to provide supplemental third-party war-risk insurance coverage to commercial carriers for

renewable 60-day periods, at substantially lower premiums than prevailing commercial rates and for levels of

coverage not available in the commercial market. In November 2002, Congress passed the Homeland

Security Act of 2002, which mandated the federal government to provide third party, passenger and hull war-

risk insurance coverage to commercial carriers through August 31, 2003, and which permitted such coverage

to be extended by the government through December 31, 2003. The Emergency Wartime Supplemental

Appropriations Act (see Note 3 to the Consolidated Financial Statements) extends the government's mandate

to provide war-risk insurance until August 31, 2004, and permits such coverage to be extended until

December 31, 2004. The Company is unable to predict whether the government will extend this insurance

coverage past August 31, 2004, whether alternative commercial insurance with comparable coverage will

become available at reasonable premiums, and what impact this will have on the Company’s ongoing

operations or future financial performance.

Frequent Flyer Awards

Southwest's frequent flyer program, Rapid Rewards, is based on trips flown rather than mileage.

Rapid Rewards Customers earn a flight segment credit for each one-way trip flown or two credits for each

round trip flown. Rapid Rewards Customers can also receive flight segment credits by using the services of

non-airline partners, which include car rental agencies, hotels, and credit card partners, including the

Southwest Airlines Bank One (formerly First USA

(R)

) Visa card. Rapid Rewards offers two types of travel

awards. The Rapid Rewards Award Ticket (“Award Ticket”) offers one free roundtrip travel award to any